Ethics

A Bold Individual Surety Claims His Coal-Backed Bonds Are Rock Solid

About this time, Scarborough revamped his bond program, parting ways with Wright and Hanson ("I wasn't crazy about them," Scarborough says). To back his bonds, he started to acquire coal properties, including ones in West Virginia and Kentucky. He also continued to expand his reach and clientele, promising to provide up to $50 million in surety credit.

|

Another change involved the bank that provided the irrevocable trust receipts related to Scarborough's asset. He switched that part of his business to a trust department of Wells Fargo Bank in Utah.

For some contractors lacking surety credit, individual surety is needed but unwelcome. "If there's something better than dealing with Scarborough, put him out of business," says one of his former clients, who declined to be identified due to the sensitivity of the topic. "Yet, he helped me get work." For others, individual surety was an unqualified godsend. Omar Karim, president of Laurel, Md.-based contractor Banneker Group, was genuinely grateful for the support.

Karim says he and his joint-venture partner needed the bond to qualify for $10 million worth of building construction work at Ft. Belvoir, Va. He remembered that his bond on the project was "backed by coal."

A Contracting Officer Rejects Coal Assets

In 2007, Wanda Peffer reviewed documents she had received from a small contractor on the island of Saint John in the U.S. Virgin Islands and didn't like what she saw. A contracting officer for the Federal Highway Administration (FHWA), Peffer was reviewing the documents for an intersection reconstruction project on which Tip Top Construction submitted a low bid of $1.8 million.

What held up Peffer's approval was the surety bond Tip Top submitted. She noticed the bond was from an individual and that it was backed by coal assets. The bond documents described the assets behind the bond as an "allocated portion of $191,350,000 of previously mined, extracted, stockpiled and marketable coal, located on property of E.C. Scarborough."

Scarborough was basically claiming that the coal-related material on the property is more like a share of actively traded stock, a type of asset that federal regulations permit to be used to back a bond, rather than a speculative asset (such as antiques) that is forbidden under federal rules.

As far as Peffer was concerned, coal fell outside the guidelines for acceptable assets in her understanding of Federal Acquisition Regulations. She exchanged information about the coal assets with Tip Top and Scarborough but ultimately rejected the bond and declined to accept a substitute asset.

Tip Top filed protests and eventually sued the federal government. Scarborough also sued it. Most of the pleadings concerned Peffer's right to say no to coal.

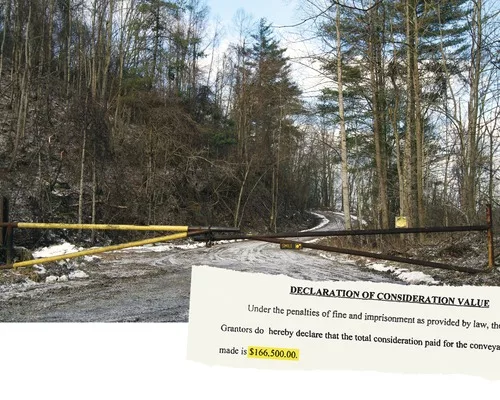

In his court submissions, Scarborough represented that the asset backing the Tip Top bond was a portion of 166,400 gross tons of previously mined surface coal on an irregularly shaped, 115.5-acre tract in rural Nicholas County, W. Va. The website of a separate Scarborough company, IBCS Mining, says that the company has another coal property in Kentucky and that it had sold coal to utilities and other buyers.

The website describes the material at the properties as waste coal piles. IBCS' team of engineers, geologists and lab technicians had determined the character of each waste pile, the website stated, and the firm planned to use "Green Technology" to reduce the troublesome piles and "America's dependence on foreign oil."

A federal judge eventually ruled in favor of FHWA, bolstering the contracting officer's authority to accept or reject a bond. During the lawsuit, much evidence found its way into the record about the coal properties.

For example, Scarborough's attorneys submitted a report from an engineering-and-mining consultant that provided a limited-scope estimate that the coal refuse on the West Virginia property could produce 3.3-million tons of recoverable coal and that, based on current coal pricing, "this may potentially equate to a gross value of approximately $261 million following processing." Qualifying their findings, the engineers said they had performed no testing or measuring of the actual, inplace material but had relied on an affidavit of the tract's former owner, a coal engineer.

Scarborough also submitted an affidavit from another coal expert attesting to the fact that coal is indeed a readily marketable asset and that, when already mined, extracted and stockpiled, coal is a very liquid asset. The expert also said it wasn't a mineral right because the material already had been mined.

Although critics claim the Federal Acquisition Regulations don't permit the use of mineral rights to back individual surety bonds, says IBCS Fidelity's Golia, "that's not what we use. Mr. Scarborough uses the actual mined minerals. This is coal you can go over and kick with your foot."

Kicking the coal may not be so easy at the Nicholas County site. Documents attached to the property deeds in West Virginia show a prior owner had been reclaiming the land under the state's direction, covering the coal waste with soil. One question is whether the property's environmental permit, No. R-707, actually allows Scarborough and IBCS Mining to remove the coal waste. The property's ownership chain and regulatory history is long and complex.