Ethics

A Bold Individual Surety Claims His Coal-Backed Bonds Are Rock Solid

At a House subcommittee hearing on H.R. 3534, a former attorney with the Naval Facilities Engineering Command, Robert E. Little Jr., took note of these discrepancies related to the Nicholas County coal assets backing the Tip Top bonds.

In his written testimony last March, Little noted that the Tip Top bond's certificate of pledged assets stated that the "previously mined, extracted, stockpiled and marketable coal" was worth $191,350,000. "Imagine now, if you will, what $191,350,000 worth of coal looks like," Little stated. He pointed out that "the surety had no mining permit to mine … or process the coal refuse" and that much of it was covered with soil by a prior owner who was the permit holder for the reclamation obligation.

"Who among you," Little asked, "envisioned grassy fields with new growth timber showing no signs of mined, extracted and stockpiled coal?"

The IBCS Mining website states that the license for the West Virginia property is "in progress." Eric Rapp, who handles environmental matters for Green Valley Coal Co., says his firm owns the mineral permit for the tract and that Scarborough "can't take anything off."

Asked about it, Scarborough says his "program has changed dramatically. We have indentured trust agreements where Wells Fargo has a security interest in the properties." He continues, "We haven't used West Virginia in years. West Virginia is ready to go—it's just not going until we get everything together in Kentucky." He sells surface and underground material from his Pike County, Ky., mine, Scarborough adds.

|

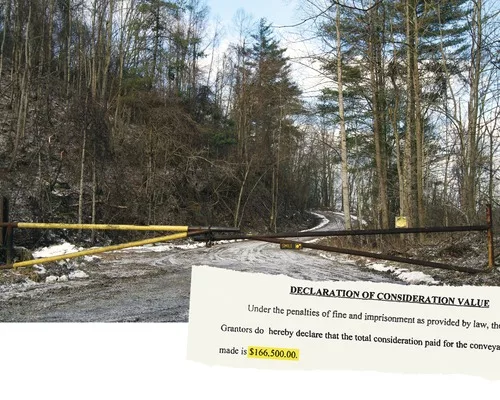

Scarborough acquired the West Virginia site in 2007 for $166,500.00, as shown in county records. Scarborough explains, "That's where false information comes in. Do you think Wells Fargo would have issued a trust receipt?" Millions more, he says, will have to be paid to the prior owner in royalties once the coal is sold. A spokeswoman for the bank said it could not comment on "our particular duties to either Scarborough or the parties" with an interest in the trust assets.

Expertise, Assets, Reform and Ethics

The fog hanging over the value of Scarborough's West Virginia coal holdings is almost as mysterious as the regulatory status of individual surety. Because federal regulations require no license or authority for individual surety, some regard it as wild and wide open for abuses. But this isn't exactly the case. State insurance departments and their investigators require certificates of authority or licenses for anyone working as a broker or insurer. If they receive valid complaints, they issue cease-and-desist orders against individuals operating without authority or a license.

When it comes to the bonds themselves, federal rules place the burden of verifying contractor responsibility on agency contracting officers. "They may not have the specific expertise required in understanding the financial analysis," concedes Michael P. Frischetti, executive director of the National Contract Management Association.

The harm from fraudulent bonds isn't immediately apparent to casual observers. NASBP CEO Mark McCallum says there's plenty of damage when public works and private contracts are backed by shaky or non-existent assets. "It cheats the taxpayers out of rightful guarantees and the subs and suppliers out of payment remedy if the bonds prove worthless," he says. If the sub cannot recover in a suit against the prime, and the prime refuses to pay or is in bankruptcy, says McCallum, "the only recourse is the payment bond. And if that's fake or worthless, it endangers the contractors' businesses."

Corporate sureties' and brokers remain determined to end what they consider fraudulent individual surety. At a time when more government and private owners are trying to save money by allowing contractors to work without payment or performance bonds, the potential for individual surety fraud creates an atmosphere of distrust.

Lynn M. Schubert, president of The Surety and Fidelity Association of America, says her members are tainted when an individual surety doesn't pay on a legitimate claim or refuses to give premium back even though the bond's rejected and not in place. "That has an impact on us," she says.

The small and minority contractors that need help are hurt the most when a fraudulent individual is rejected by the owner during bidding, or worse, when the individual surety fails to return the premium, Schubert says.

If the new proposed rules thin the ranks of individual sureties, any bonds written by individual sureties under those rules will have real assets behind them. Additionally, small contractors still can get bonds through the Small Business Administration's bond guarantee program, she says. Or they can avail themselves of several different programs created to help contractors to qualify for corporate surety bonds and assist them in finding a qualified bond professional.

Scarborough, for his part, also is wary of some individual sureties after being stung by what he learned in 2005 and 2006 about Hanson and Wright.

He testified in the NASBP deposition that he never had reason to suspect Wright. And about whether Hanson should be admitted to the individual surety association, Scarborough said, "He doesn't strike me—from what I've read and from what I heard from others—as being somebody that will step up to the plate and be accountable for whether he did something right or wrong."

The text of this story was clarified on Feb. 5, 2015.