2022 Forecast: Industry on Slow Path to Recovery

Money for removing lead pipes and service lines is included in the $1 trillion infrastructure act.

AP Photo/Brittany Peterson

As the world continues its widespread vaccination effort, COVID-19 restrictions ease somewhat and the now-signed $1-trillion U.S. infrastructure spending bill moves forward, forecasters are expressing cautious optimism about the year to come.

*Click the table for more detail

“The economic recovery has resumed following the setback in the third quarter, and construction should follow suit,” says Richard Branch, Dodge Construction Network chief economist. “The dollar value of nonresidential building projects in the early stages of planning is at a level not seen in nearly 13 years, and the infrastructure bill will provide meaningful support and growth to the sector in years to come.”

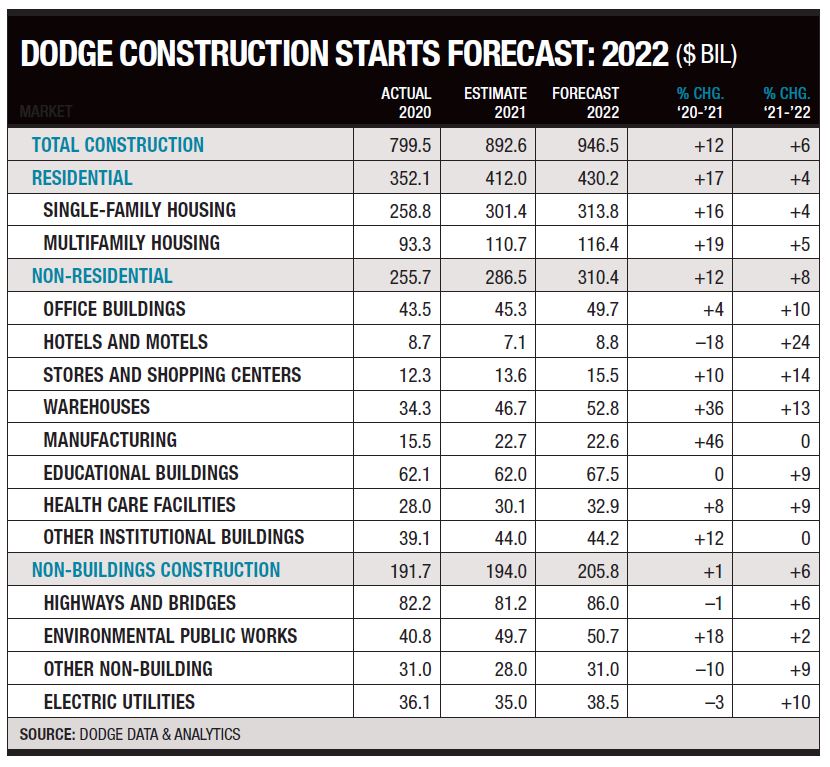

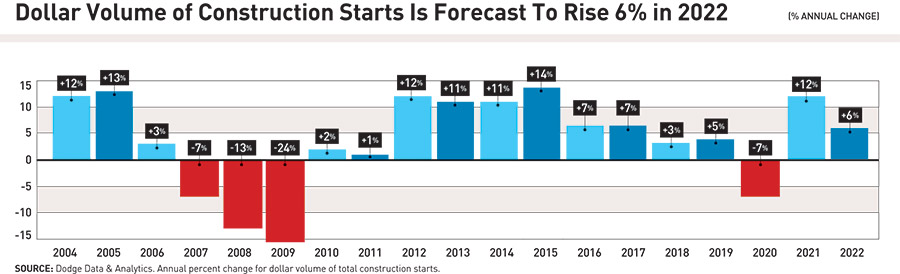

Dodge predicts a 12% increase in the dollar value of construction by the end of 2021, with a 6% overall rise to come in 2022. But the outlook has some drawbacks. Branch notes that “hope must be tempered” as the industry continues to face a number of challenges. “In a world where prices are rising, materials are hard to come by and labor is scarce, the ability to do more with less is what’s going to be a critical path forward in terms of increasing your profit margins,” he says. “While construction starts will grow in 2022, that growth is expected to be modest.”

Julian Anderson, president of Rider Levett Bucknall, also sees these as recovery stumbling blocks. “The labor shortage we have been talking about for several years became worse and ‘just-in-time’ supply chains have been tripped up by burgeoning retail demand and COVID-19 impact on manufacturing,” he says, even as more remote work and low interest rates stoke the housing market. “That cocktail is giving the construction industry a sizeable headache,” says Anderson, who expects this to continue for the majority of 2022.

*Click the table for more detail

“I don’t see a slowdown happening until the Federal Reserve’s decision to taper its bond buying program starts to be felt and interest rates start to rise,” he adds. “In the meantime, I expect to see significant upward pressure on prices as we move into the new year, with the first half of 2022 being particularly challenging” to navigate through. In the long term, however, Anderson believes the outlook is positive. “Even if we do have a cyclical slowdown, work flowing from the Infrastructure Investment and Jobs Act should provide support for the construction industry well into the future,” he says.

“While construction starts will grow in 2022, that growth is expected to be modest.”

Richard Branch, chief economist, Dodge Construction Network

Single-Family Growth Slows

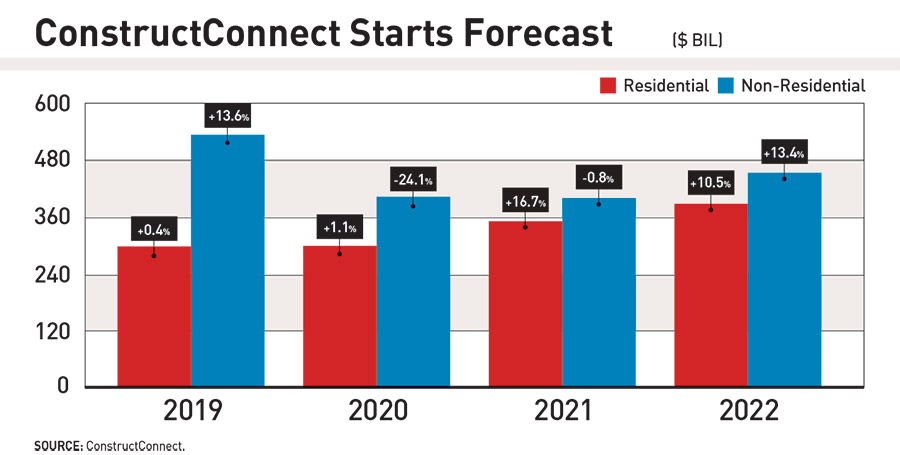

Residential starts continue to trend upward, but the pace is slowing. ConstructConnect’s Construction Starts Forecast estimates a 16.7% increase in total residential work for 2021, with an additional 10.5% boost in 2022. “To date, relative to early last year, residential activity has vastly exceeded the recovery efforts of nonresidential building and engineering work,” says Alex Carrick, ConstructConnect’s chief economist. “Residential currently accounts for half of total volume, where its share has traditionally been about 40%,” he says. “There’s been strong new homebuilding driven by ultra-low interest rates and abundant savings that have facilitated the accumulation of down payments.”

Dodge expects single-family starts to end the year up 16% from 2020, with a more modest 4% boost in 2022. Starts are up 19% in 2021 for multifamily housing, with another 5% increase forecast for 2022.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

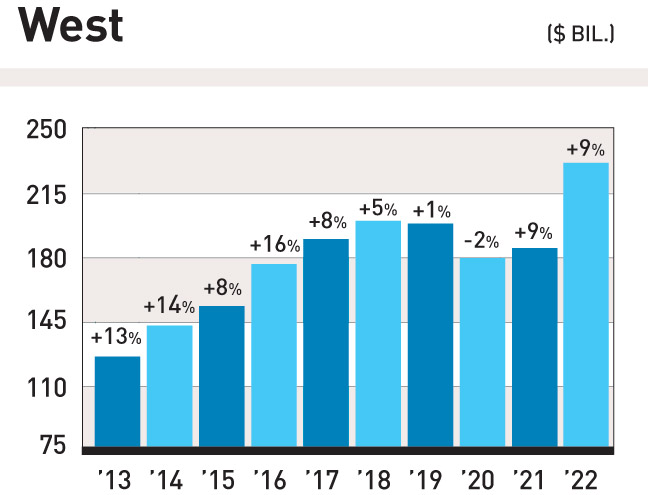

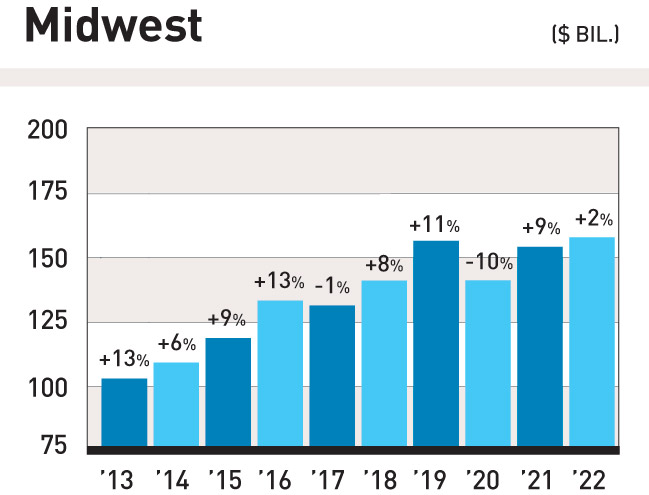

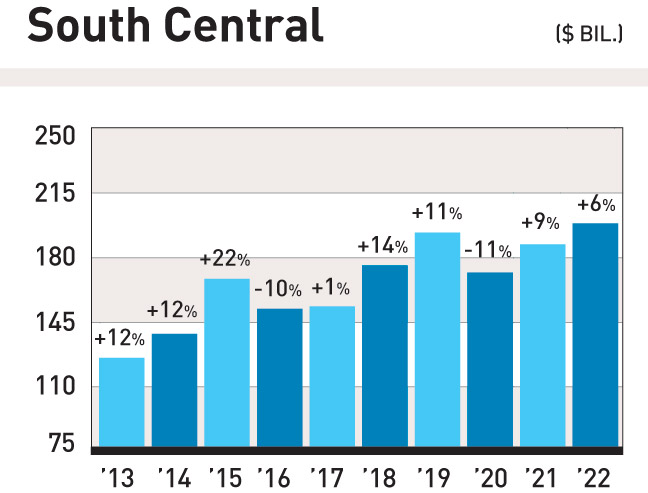

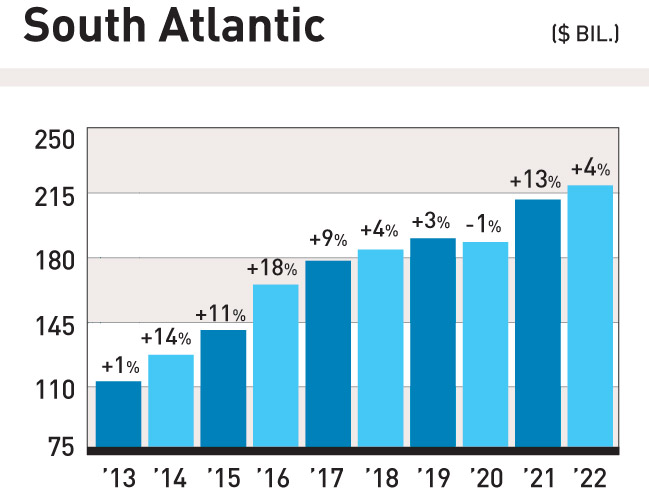

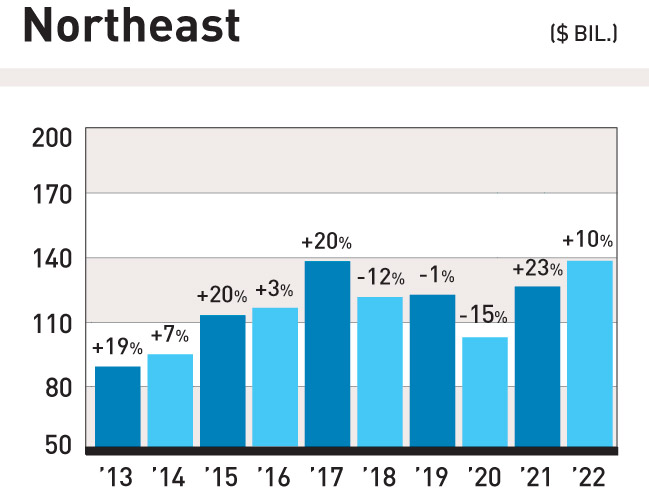

CONSTRUCTION STARTS TO INCREASE ACROSS ALL REGIONS IN 2022

Starts in the Northeast region will rise 10%, with starts in the West up 9% according to Dodge Construction Network

*Click on the graphs for more detail

*Click on the graphs for more detail

*Click on the graphs for more detail

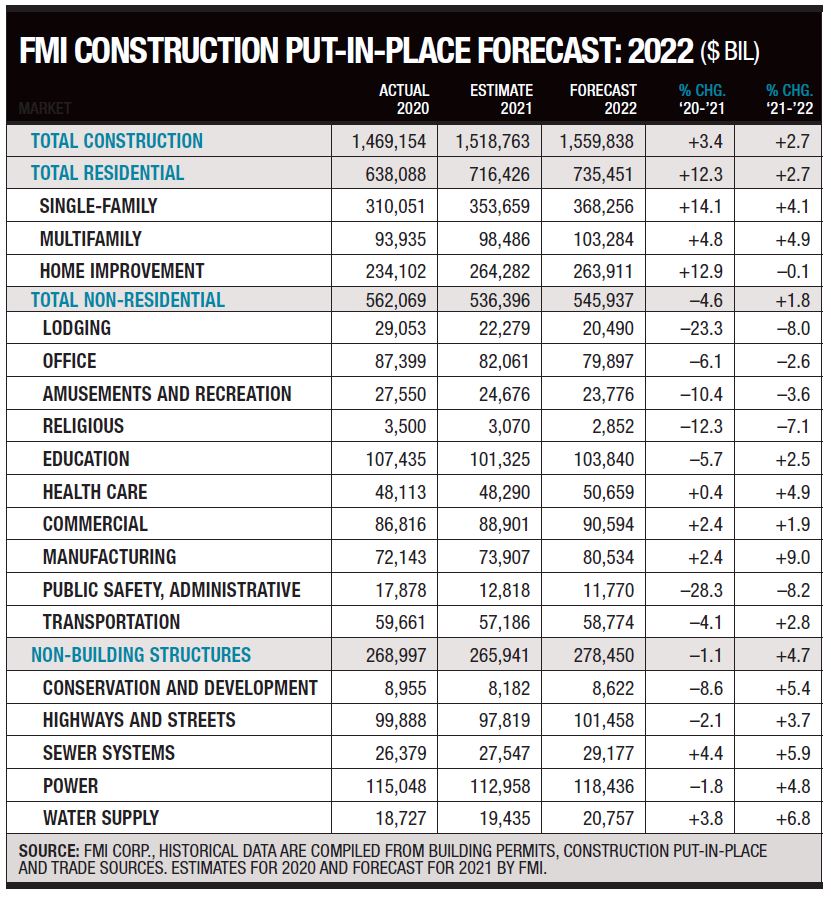

The FMI Construction Put-in-Place forecast had similar numbers for total residential, with an expected 12.3% increase in 2021. Single family is up 14.1%, while multifamily rose 4.8%. FMI predicts a smaller overall increase in 2022, at 2.7%, with single family and multifamily at 4.1% and 4.9%, respectively. “Developers will continue to add [single-family homes] through 2022, but at a slower rate and more carefully,” says FMI principal Jay Bowman. “Higher construction costs and ongoing resource constraints layer increasing risk against softened demand.”

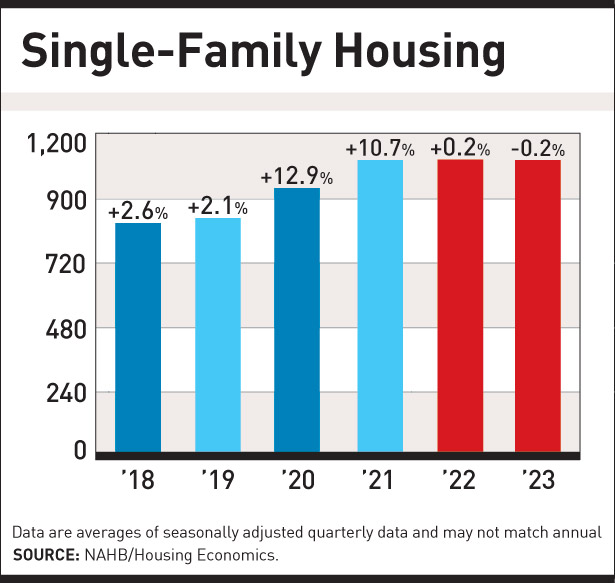

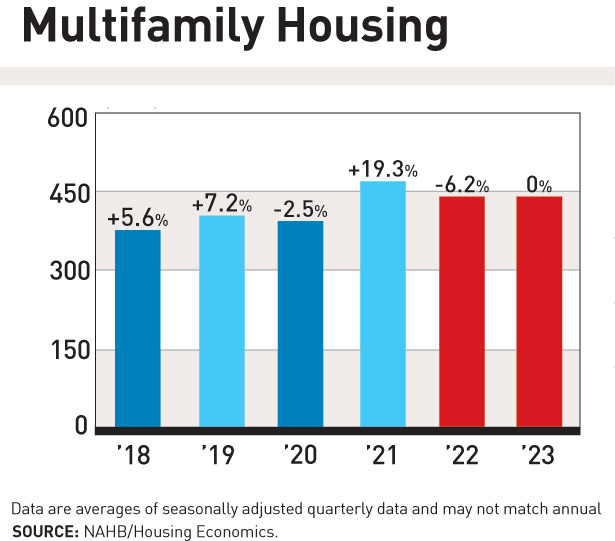

The National Association of Home Builders (NAHB) estimates total housing starts will rise 13% by year end, with single-family units up 10.7% and multifamily housing up 19.3%. For 2022, they forecast a small 1.7% drop in overall starts, spurred by a 6.2% decline in multifamily housing. Single family is expected to rise 0.2%.

“Home builder confidence has cooled somewhat over the course of 2021” after peaking in November 2020, says Robert Dietz, NAHB chief economist. “Even a flat level of single-family starts for 2022 would represent more than a 20% gain over the 2019, pre-COVID construction levels.” He said affordability will be a “key emerging constraint in 2022 for home buyers, given the substantial and unsustainable run-up in home prices during 2020 and 2021.”

NAHB FORECAST

Home Building to Remain Relatively Flat in 2022

Total housing starts are expected to rise 13% by the end of 2021, before falling 1.7% in 2022, according to the National Association of Home Builders. NAHB forecasts single-family homes will be up 10.7% by the end of this year, with an increase of 0.2% next year. Multi-family starts, up 19.3% in 2021, are expected to drop 6.2% in 2022. “Housing affordability will be the key emerging constraint,” says Robert Dietz, senior vice president and chief economist at NAHB.

*Click on the graphs for more detail

Warehouse Sector Continues to Soar

In the commercial sector, Dodge reports an overall 15% rise in 2021 and a 12% increase in 2022. Warehouse construction remains a key driver. Starts are set to increase 36% this year, with an added 13% boost in 2022. “Warehouse starts continue to stagger the imagination,” says Branch. He points to e-commerce businesses as catalysts, with online shopping continuing to grow in popularity.

In the retail sector, a 10% jump is estimated for 2021, with a 14% gain in 2022. Branch attributes this to the rise in multifamily housing in smaller cities and suburban areas. The hotel sector, especially affected by COVID-19 restrictions, dropped 51% in 2020 and another 18% in 2021. A recovery of 24% expected in 2022. “We don’t really expect business travel to return in force until probably the back half of 2022,” says Branch, which will “certainly suppress construction activity for hotels.”

*Click on the graph for more detail

Office construction took a sizeable hit in 2020 amid the surge in remote work. After a 20% drop that year, office work is expected to increase 4% this year, followed by a 10% boost in 2022, according to Dodge. The FMI forecast is less optimistic about office construction, expecting a 6.1% drop in 2021, with a further decline of 2.6% next year. The lodging and amusements and recreation sectors also will go down, says Bowman, adding that “construction typically lags overall economy by one to two years. It will take a while for people to decide what they’re going to come back to following COVID and what will be permanent changes.”

Federal Spending—Just in Time

Federal infrastructure funding will provide a significant boost in transportation investment “that will impact every state highway, bridge and transit program,” says Alison Black, American Road & Transportation Builders Association senior vice president and chief economist. “The increase in the federal-aid highway program is the largest boost in funding since the first two years of the program over 60 years ago.”

ARTBA FORECAST

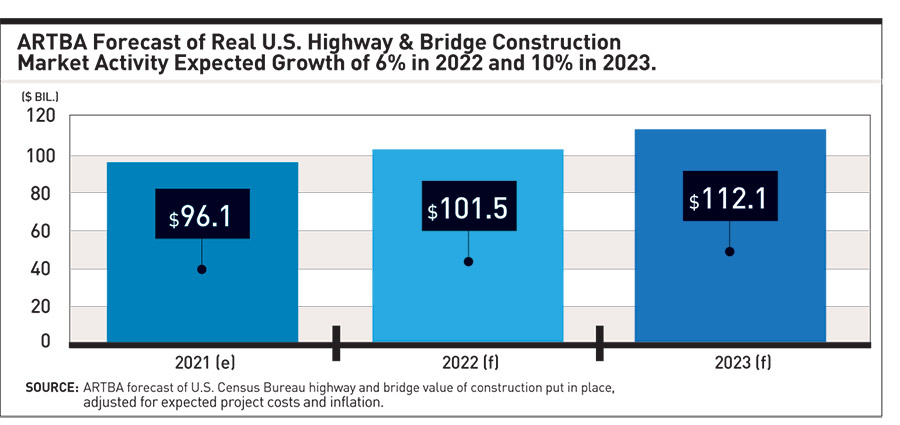

Highways and Bridges to Increase 6% in 2022

*Click on the graph for greater detail

The American Road & Transportation Builders Association estimates total spending for highway and bridge construction to decrease 4% in 2021, and 6% in 2022. But the recently signed infrastructure act will generate more activity, says Alison Black, senior vice president and chief economist. “Spending will continue to ramp up in 2023 and 2024 as work continues and new projects get started,” she says.

In the highways and bridges sector, the group expects to see a 4% drop in 2021, with a 6% increase in 2022. Black says issues with supply and inflation remain. “The increase in fuel and input prices have been a challenge this year for the entire construction industry, and some contractors have also faced significant delays for select materials,” she says. “Most economists believe the price increases are a temporary supply-side issue. So, while the price pressures will likely continue through the first part of 2022, we expect project costs to moderate as supply issues are resolved.”

Dodge estimates highways and bridges to drop just 1% by the end of this year, with road construction down 2% and bridges up 1%. In 2022, Dodge forecasts a 6% increase overall, with 3% in each sector. Branch also notes the infrastructure act ais the main catalyst. The program “will have a profound impact on construction starts in the years to come,” he says. “In 2022 alone, it will increase public works construction starts by $11 billion over and above if the bill had not passed.”

*Click on the graph for greater detail

The new infrastructure program is set to add about $35 billion to U.S. construction activity in 2023, says Moody’s Analytics.

“This is an especially economically propitious time to increase public infrastructure investment, since the return is substantially greater than the government’s cost of financing given extraordinarily low interest rates,” say Moody’s chief economist Mark Zandi, and Bernard Yaros, assistant director in a Nov. 9 report. “Thirty-year Treasury bond yields are close to 2%, while the return on almost any public infrastructure project is likely to be meaningfully greater.”

“I expect to see a signifi cant upward pressure on prices as we move into the new year.”

Julian Anderson, president, Rider Levett Bucknall

Moody’s sees boosts in Amtrak funding for Northeast Corridor rail infrastructure upgrades and route expansion, as well as in measures favoring more use of public-private partnerships.

“The inclusion of $100 million for PPP capacity-building will help new governmental entities explore the PPP procurement model for capital projects,” says Moody’s. “The legislation also raises the cap on private activity bonds to $30 billion from $15 billion, allowing private entities to benefit from tax-exempt bond treatment to finance certain public works improvements like highways.”

The infrastructure spend program also “sets the stage for further strong growth in volume and earnings for companies that produce aggregates, concrete and cement,” says Emile El Nems, Moody’s senior credit officer. “Half of aggregate demand in the U.S. typically goes to public infrastructure.”

While the research and ratings firm also notes a “benefit” from more activity for construction and engineering companies in transportation, utilities, renewable energy and telecom sectors, “the magnitude of the impacts on revenue and profitability will depend on the amount of work they win and margins they generate, and on the effects of pricing pressures on inputs and labor.”

Says Moody’s: “The most serious concern … is around execution risk.” The infrastructure and reconciliation packages “are complex, with lots of massive moving parts.”