The Top 500 Design Firms: 2010-2011 at a Glance

For the first time in over three years, the construction industry is seeing signs that the deep industry recession has bottomed out and the market is turning around. But among large design firms, no one is ready to pop any corks to celebrate. However, most firms believe the recovery will be a long, slow climb with some bumps along the way.

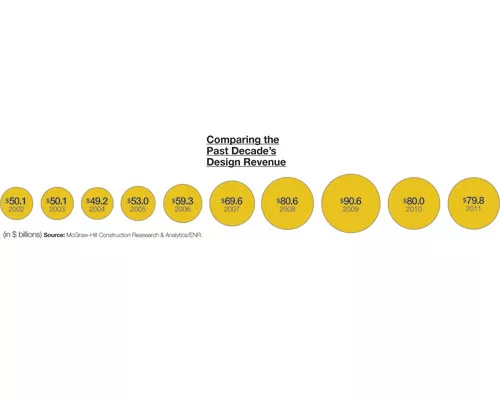

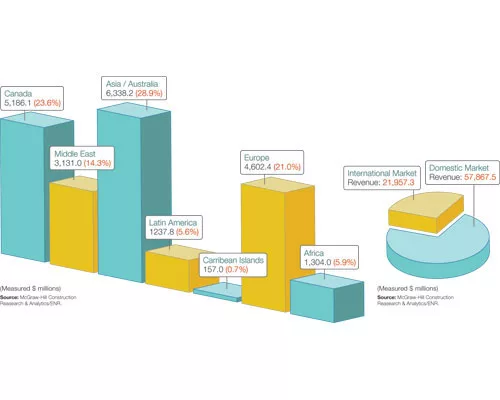

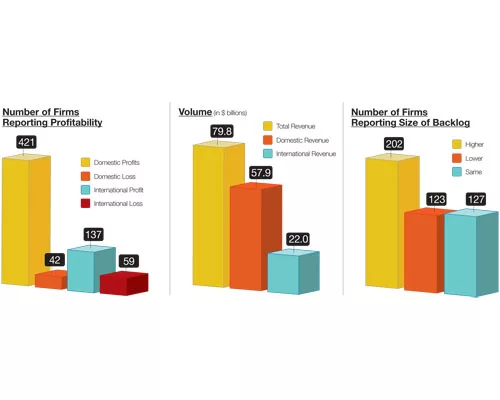

The results can be seen in ENR's Top 500 Design Firms list. The Top 500, taken as a group, had overall design revenue of $79.8 billion in 2010, down 0.2% from 2009's $80 billion and 11.9% from 2008's high-water mark of $90.6 billion. Not surprisingly, the domestic U.S. market was hit harder for the Top 500 than the international market. Design revenue for projects in the U.S. for the Top 500 fell 2.3% to $57.86 billion in 2010 from $59.22 billion in 2009. Revenue from projects outside the U.S. rose in 2010 to $21.96 billion, up 5.6% from $20.80 billion in 2009. However, domestic revenue dropped 15.1% over the two-year period from 2008 to 2010, while international design revenue fell 2.1% during the same time period for the Top 500.

There is a general feeling among the Top 500 firms that the markets will recover over the next 12 months. The ENR online survey contained a series of market-related questions, including whether survey participants believed prospects for the U.S. construction market would improve over the next 12 months. Of the 418 firms on the Top 500 that answered this question, 58.9% said the market would improve. Only 6% believed it would continue to decline, while 35.2% thought the market would stay the same.

“I don't think anyone believes that we are out of the recession yet,” says Brad Perkins, CEO of Perkins Eastman. “We are looking a ‘bathtub' curve of a recovery. We are out of the drain, but we will have a long, gradual rise before we hit a significant upward slope,” says Craig Martin, CEO of Jacobs.

Dick Fox, CEO of CDM adds, “I think it is going to take two years for the market to come all the way back. I don't think recovery will come this year, but there will be slow increases in the market.”

John Cryer, principal at PageSoutherlandPage, says he is seeing more private-sector requests for qualifications but was surprised at how quickly federal-sector bids shut down as the debate in Congress over budget cuts heated up. “This time, I think the private sector will lead us out of the recession.”

John Dionisio, CEO of AECOM, says firms have learned to work smarter and will be better prepared when the market turns around. “Yes, we have all been pressed, but there are some really good signs in the market for the next 12 months,” Dionisio says. He did not elaborate on what those signs are.

“That the economy seems to be on a steady course toward sustained growth is a cause for optimism, but not exuberance,” says Kathleen McGinty, senior vice president of Weston Solutions. She expects weak growth in the short term.

For most, if not all, the firms on the list, the biggest concern is project funding in the public sector. “No one has money, and no one has a good way to get money, so the public sector is going to be problematic in the near term,” says Jacobs' Martin. Only those segments within the public sector that have revenue streams attached through such sources as tolls or ratepayers will remain steady to strong, he says.

Some firms say a pause in new projects hasn't stopped public agencies from preparing for a turnaround in funding. “Utilities are continuing planning activity,” says Dan McCarthy, president of Black & Veatch's global water group. “Even in California, where activity is down by half, agencies are engaged in long-term planning. They know they can't ramp up programs quickly, so they want to be prepared when funding does become available.”

Who Owns Them Now?

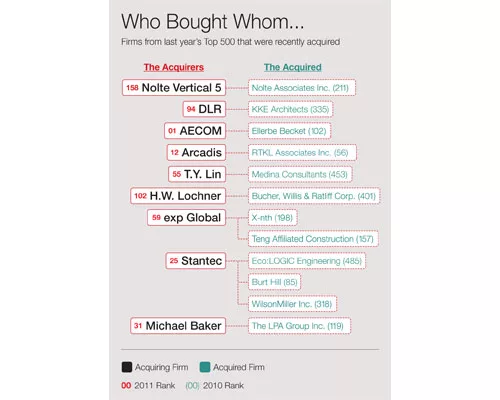

One of the biggest trends in the design profession is consolidation among firms. This year, 12 firms from the 2010 Top 500 were acquired or absorbed into their parent companies. And two firms on this year's Top 500 already have been acquired this year.

Among the larger deals was Jacobs' $675-million purchase of the mining and metals operations of Norway's Aker Solutions. Mining and metals is a very robust market, and the acquisition is squarely in the firm's sweet spot, says Martin. He says the acquisition puts Jacobs at the top end of that market, along with Fluor and Bechtel.

Martin says many design firms have a lot of cash but few places to invest it other than through acquisitions. “Acquisition prices have finally come down from previous highs, with multiples now back down to single digits,” Martin states. He says Jacobs is looking for deals in upstream oil and gas markets as well as the right opportunities in power markets.

Canada's Stantec is one of the most active companies in acquisitions in the U.S. In 2010, it bought three firms from last year's Top 500 Design Firms list: No. 85, Burt Hill, Philadelphia, for $36 million; No. 318, WilsonMiller, Naples, Fla., and No. 485, ECO:Logic, Rocklin, Calif. And this year, it has acquired Anshen+Allen Architects, which is No. 284 on this year's list. “I believe we have achieved critical mass in the U.S., with nearly 5,000 staff to go [and] 6,000 in Canada,” says Stantec CEO Robert Gomes.

Gomes says acquisitions were difficult in 2008 and 2009 because it was tough to value firms in a down market based solely on expectations. Also, many firms had unrealistic estimates of their own value in a recessionary market. “As it turned out, we made no acquisitions in the first half of 2010 but 10 in the second half,” he says.

Stantec believes in the strength of its own brand. “While there is value in brand names of acquired firms, we are acquiring talent, not just a name,” says Gomes. That is why it rebrands the firms it acquires under the Stantec name. “We realize that it is difficult for some firms, but we try to provide the people of the acquired firms with greater resources to match greater challenges,” he says. Seven of the Stantec's 11 senior vice presidents are from acquired firms.

Another Canadian designer that made a splash in the U.S. in 2010 was exp Global, which changed its name from Trow Global on April 4. The firm acquired Teng Affiliated Cos., Chicago, which ranked No. 157 on last year's Top 500, and X-nth, Maitland, Fla., which ranked No. 198. “We had been in the pipeline and oil sectors in the U.S., but two years ago we redirected the company to be more global in a broad variety of sectors,” says Rob Petrov, senior vice president of exp Global. “We are now a full-service firm in the U.S.”

Defense contractor SAIC has made a major move into the construction design market. In the pastthree years, SAIC has acquired Oklahoma City-based Benham Group and Denver-based R.W. Beck. “We are one of the few major defense firms that have moved into the construction market through acquisition,” says J.T. Grumski, senior vice president of SAIC. He says that SAIC is continuing to look to add new firms but not to build size. “We are looking for specific expertise in enduring markets, such as energy and technology.”

Buying Markets

Many firms are looking to acquire firms so they can expand in their strongest markets. One of the biggest was CDM's acquisition of Wilbur Smith Associates, a deal that was announced on Feb. 25. WSA is ranked No. 70 on this year's Top 500. “This has moved us into the water market and transportation,” says Fox.

Another firm getting into new market sectors is CDI Engineering Solutions, which last year purchased L. Robert Kimball & Associates, Ebensburg, Pa. Kimball was ranked No. 155 on last year's Top 500. This move gives the firm new capabilities in the infrastructure market, says Bob Giorgio, CDI's president. Kimball's capabilities let CDI to play in the general infrastructure markets as well as allow it to provide added infrastructure support to its industrial customers, both in the U.S. and abroad, he adds.

But not all design firms are looking to grow through acquisition. HNTB topped the $1 billion mark in 2010 by just $60,000, but the company did it through organic growth. The milestone was a long time coming, says Paul Yarossi, president of HNTB Holdings. “We have not made a major acquisition in the past 10 years.”

The move toward consolidation has put many mid-size firms on the defensive. However, some midsize firms say expertise is more important than size. “Firms like AECOM are huge compared to us, but their bridge division is no bigger that ours,” says Mike Britt, vice president of Modjeski and Masters Inc. “I have never had a client ask me how big we are. They are more concerned about whether we can provide them with a highly skilled team on-site,” says Craig Goehring, CEO, Brown and Caldwell. He adds that consolidation also has removed a few competitors that have been absorbed into larger firms.

The recession has taken its toll on design firms, but relatively few have failed. This is because most major firms have paid attention to their bottom lines, despite pressures to maintain the top line. “We have been more selective in selecting projects,” says Carl Roehling, CEO of SmithGroup. “We don't want to pursue work just for the sake of volume.”