Economics

Architecture Billings Swing Back Positive But Headwinds Persist

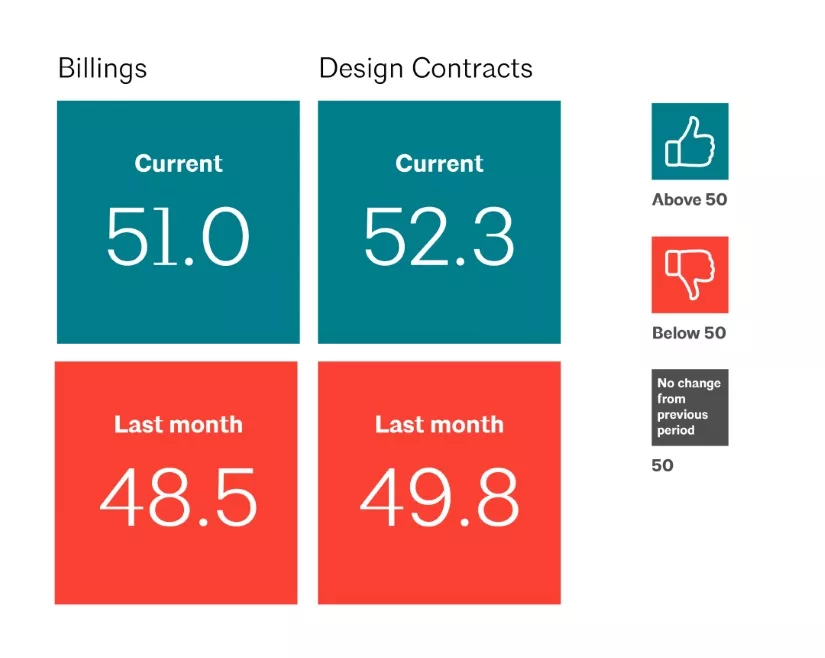

The AIA/Deltek Architecture Billings Index swung back into positive territory in May (any score above 50 reflects an increase in architecture billings), but economists warn that there are still major concerns at architecture firms about the business environment, particularly ones that focus on multifamily residential and commercial construction. Chart courtesy of the American Institute of Architects

Architects experienced a rebound in billings in May after a fall in April, according to the latest Architecture Billings Index from the American Institute of Architects and Deltek based on member firm reporting.

The index score of 51 for May (any score above 50 reflects an increase in architecture billings) was the highest it has been since September 2022. Inquiries into new projects and design contracts also increased, reaching their highest levels since February.

The billings score increased from 48.5 in April. AIA member firms also reported that inquiries into new projects accelerated to 57.2 from 53.9 in April. The value of new design contracts also moved up to 52.3 in May from 49.8 in April.

“The modest improvement in overall demand for architectural services that we saw last month is encouraging news," said AIA Chief Economist Kermit Baker in a press release. “However, there continues to be variation in the performance of firms by regional location and building specialization. This suggests that overall business conditions for the profession likely will continue to be variable."

Despite growth in the overall ABI this month, business conditions remain variable in different regions of the country, AIA reported. Billings improved in the South for the second consecutive month in May, while they were essentially flat in the Midwest, following six months of growth. However, billings continued to decline at firms located in both the West and Northeast, where scores have been below 50 since last fall.

Business conditions deteriorated further at firms with a multifamily residential specialization in May, falling to the lowest level in two years, AIA said. Billings also declined for the ninth consecutive month at firms with a commercial/industrial specialization. Business conditions improved, however, for the second month in a row at firms with an institutional specialization, as they reported their strongest growth since last year.

The index is derived from AIA’s Work-on-the-Boards survey and reflects a roughly 9-12 lead time between design billings and construction.

Data from the May ABI

- Regional averages: South (52.3); Midwest (49.6); Northeast (48.7); West (47.7)

- Sector index breakdown: institutional (53.4); mixed practice (firms that do not have at least half of their billings in any one other category) (52.7); commercial/industrial (47.5); multifamily residential (43.0)

- Project inquiries index: 57.2

- Design contracts index: 52.3

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →