Wind, Solar on the Way to the Mainstream

Wind turbines placed on a ridgeline in snowy Mount Storm, W.Va., produce up to 264 MW.

PHOTO COURTESY OF BLACK & VEATCH

Experienced crews help to drive down costs of solar power with streamlined installation of PV panels.

PHOTOS COURTESY OF BLACK & VEATCH

Experienced crews help to drive down costs of solar power with streamlined installation of PV panels.

PHOTO COURTESY FIRST SOLAR

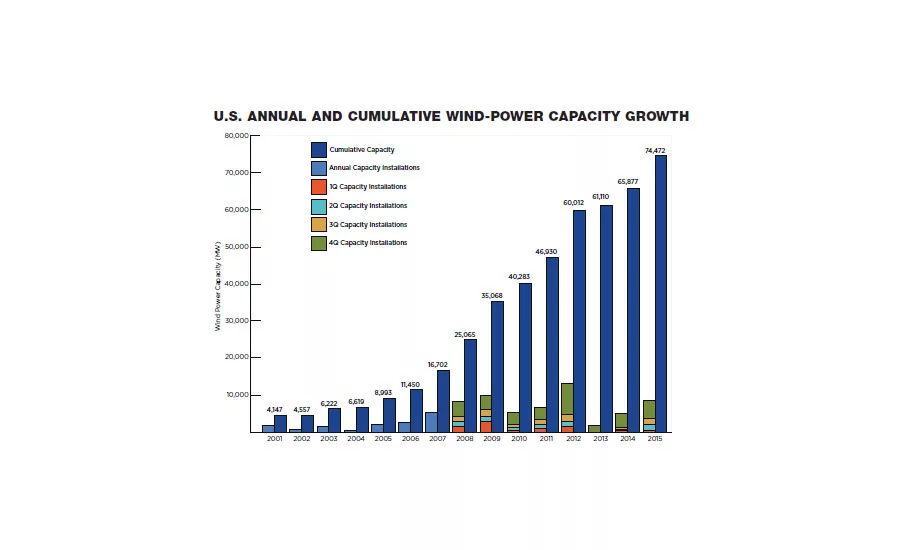

CHART COURTESY AMERICAN WIND ENERGY ASSOCIATION

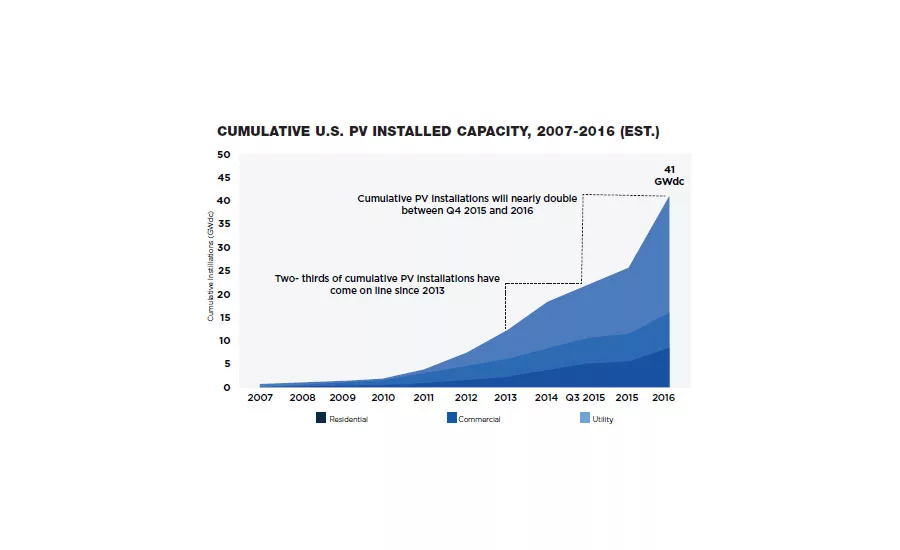

CHART COURTESY SOLAR ENERGY INDUSTRIES ASSOCIATION

Propelled by powerful and complementary forces, the U.S. renewables market is in the early stages of a multiyear period of sustained development and construction activity that may come to be viewed as the golden age of wind and solar power.

Article Index:

The pace of work is already brisk. According to a late-January report by the American Wind Energy Association (AWEA), 5,001 MW of wind capacity was installed in the fourth quarter of 2015 alone—more than the 4,854 MW put in place in all of 2014—and, as 2016 started, another 9,400 MW of wind capacity was under construction.

The solar market is just as hot. Final numbers for 2015 are not in, but the Solar Energy Industries Association (SEIA) says it expects the last year’s solar installations to total more than 7,000 MW, including about 4,000 MW in the fourth quarter. SEIA expects the pace of installations to double in 2016, with an estimated 15,000 MW of solar to be put in place by year’s end.

Market participants say that four primary drivers—federal tax policy, declining project costs, state renewable portfolio standards and the Environmental Protection Agency’s Clean Power Plan (the enforcement of which is now on hold)—are providing the thrust. The drivers’ central theme is that wind farms and utility-scale solar facilities are not only good for the environment; in an ever-growing share of cases, they represent the most cost-effective way to generate power.

In December, Congress approved—and President Obama signed into law—extensions of the investment tax credit (ITC) for solar projects and the production tax credit (PTC) for wind that, together, give the renewables sector the longest period of tax certainty in its relatively short history.

Before that action, the 30% ITC for solar had been scheduled to ramp down to only 10% on Jan. 1, 2017; now, the ITC will remain at 30% through 2018, then gradually ramp down to 10% in 2022 and beyond.

The PTC for wind, which provides a $23-per-MWh tax credit for power generated by wind turbines during their first 10 years of operation, had been scheduled to expire at the end of this year (as long as the wind project in question started construction by the end of 2014). Now, wind projects that break ground by the end of 2016 will be eligible for the full PTC for 10 years, even if they do not come on line until 2018.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

Wind projects with 2017 construction starts will see a 20%—or $4.60/MWh—reduction in their PTC, while projects that break ground in 2018 and 2019 will see 40% and 60% reductions in their PTC, respectively.

“Previously, wind was a very cyclical market with some very big years and some quiet years,” says Ben Fischer, CEO at Signal Energy Constructors of Chattanooga, Tenn., a large wind and solar contractor. “But with the longer PTC extension, we expect the market to continue to grow at a steady pace. … The PTC provides certainty” to a market that, to date, has been characterized by ups and downs.

Longer-Term Viability

John Curcio, chief commercial officer of Cupertino Electric, a large solar contractor based in San Jose, Calif., says the ITC extension is “a huge deal because it makes the solar industry viable.”

Curcio says that, before Congress acted in December, solar developers had been rushing to complete construction in 2016—before the 30% ITC was reduced to 10%. “Now that the pressure is off” to finish projects this year, he said, there may be “a slight dip” in 2016 solar installations from prior expectations, but the outlook for 2017 and beyond is more positive.

AWEA CEO Tom Kiernan notes, “Having policy certainty with the PTC overcomes one challenge, but others still exist, including availability of the necessary power lines. New transmission can act as a renewable-energy superhighway, delivering low-cost wind energy from rural areas to densely populated U.S. cities where it’s needed the most” (see sidebar).

The PTC and ITC—combined with technological improvements and lower equipment and installation costs—have reduced wind and solar power prices to levels that, only several years ago, few would have considered possible. For example, in the Great Plains region, which has some of the nation’s best wind resources, several recent wind power purchase agreements (PPAs) have featured long-term, fixed prices of less than $25 per MWh.

Similarly, in the desert Southwest and Texas, which have the best solar resources, the price of power in some recent solar PPAs has been below $50/MWh and even $40/MWh.

Freedom From Fuel Costs

As utilities and renewables developers always point out, wind and solar projects—unlike plants fired by natural gas or coal—have no fuel costs and, therefore, no potential for power-price fluctuation over time. That provides an important hedge to utilities, which seek to diversify their generation portfolios to mitigate price risk.

On a per-MW basis, wind-farm and solar-facility costs have been on the decline for some time, and wind turbines and solar photovoltaic panels have been becoming increasing efficient in converting wind and solar rays into electricity.

Bruce Peacock, vice president of technical services and construction at Charlotte, N.C.-based Duke Energy Renewables (DER), a large developer of both wind and solar projects, says wind-turbine rotor size “has been increasing steadily: 101 meters [in diameter] in 2010, 110 meters in 2015, and we will be installing 126-meter rotors in 2016. Larger rotor size produces a higher net-capacity factor for a given turbine rating in a given wind-speed environment, driving a lower cost of energy.”

Improved wind-turbine design also is enabling wind farms to be developed in areas with only modest wind resources.

For example, Portland, Ore.-based Iberdrola Renewables is building a 208-MW wind farm in northeastern North Carolina that will employ 104 of Gamesa’s 2-MW G114 wind turbines, which have a 38% larger “swept area”—the size of the circle the blades spin within—and produce more than 20% more energy annually than earlier versions.

DER’s Peacock notes, “Our erection contractors’ productivity has steadily improved. On a large site, they can receive and erect up to 10 turbines per week. This rate is not significantly higher than four years ago, but you have to take into account that the turbine towers and rotors are now larger.”

In December, DER announced that its new, 200-MW Frontier wind farm in Kay County, Okla., will feature 61 of Vestas’ 3.3-MW V126 wind turbines. Vestas says the Frontier project represents the first order for V126 turbines in the U.S., where 2-MW wind turbines have been the norm in projects developed over the past two or three years and where, earlier, 1.5-MW and 1-MW turbines dominated the market.

Even bigger turbines are on the way: Deepwater Wind’s 30-MW Block Island project, under construction off the Rhode Island coast, will feature 6-MW wind turbines with rotors 150 m in diameter.

Especially in the past year or two, the effects of renewable portfolio standards (RPSs) have been supplemented by voluntary efforts by corporations and the U.S. military to reduce their carbon footprints by building or buying power from wind farms or big solar projects.

For example, last month, Pattern Energy completed the Benton County, Ind.-sited, 150-MW Amazon Wind Farm Fowler Ridge, which sells all its wind power to Amazon Web Services. In Clay County, Texas, the new 204-MW Shannon wind farm is providing power to Facebook, and in the Florida panhandle, Coronal Development Services, Charlottesville, Va., is building three solar projects totaling 120 MW at Navy and Air Force bases.

Driving Down Costs

Meanwhile, solar technology “is continually improving in multiple ways, the most important being efficiency,” says Trent Mostaert, vice president and general manager of Solar & Emerging Renewables Operating Group at M.A. Mortenson Co., Minneapolis, a leading builder of solar and wind projects. “A few years ago, a [solar photovoltaic] panel might be able to generate only 275 watts of electricity while in operation. … Now, the same panel is able to generate 315 watts, which drives down the overall costs of generation.”

Mostaert adds that other types of technology, “such as trackers and supervisory controls and data acquisition [SCADA] systems, are improving, as well.”

The pace at which solar facilities move from concept to completion also is picking up. “Our [engineering-procurement-construction] partners have continued to get more efficient in their installation practices,” says Paul Donley, a DER engineer. “Logistics, materials designed for construction efficiency, and familiarity [with installing solar projects] have all contributed to increased construction velocity.”

Donley says that, while installing 2 MW per day of solar capacity was “once considered at the fringe of reality,” it is now “almost routine on large, utility-scale solar projects. … Five years ago, a 1-MW project could take up to six months for construction,” he says. “Now, it is possible to see a 100-MW project being installed in roughly the same timeframe.”

Signal’s Fischer agrees that productivity gains have been sizable, mostly due to “design and process improvements as well as logistic management practices.” He adds that Signal has “a unique capability, in that we self-perform the mechanical and structural installation of piles into the ground that serve as the foundation for the trackers and the structural racking that holds solar modules, which is the critical element to ensuring the project meets schedule.”

For several years now, decisions by utilities to add wind and—more recently, utility-scale solar—to their portfolios have been driven, in large part, by state RPSs, which typically require more utility power to come from wind, solar and other renewable sources.

According to a January study by the Dept. of Energy’s National Renewable Energy Laboratory and the Lawrence Berkeley National Laboratory, 29 states and the District of Columbia currently have an RPS. Most of them were enacted in the late 1990s or 2000s, and many have been updated and expanded since then. “[We] estimate that RPS-related renewable capacity additions over the 2013-14 period averaged almost 5,600 MW/year,” the study said, with 48% of the additions tied to utility-scale solar and 19% of them tied to wind. Much more wind and solar will be added over the next few years to comply with RPSs, particularly in states such as California, which has established a 33% renewables mandate for 2020 and a 50% goal for 2030.

Another Driver—Maybe

Yet another boost for renewables—particularly wind and solar, due to their low cost and relative simplicity—is expected to come from the EPA’s Clean Power Plan (CPP), whose aim is to reduce, by 2030, greenhouse-gas (GHG) emissions from fossil-fired power plants by 32% from their 2005 levels. The boost would come as utilities and states develop and implement CPP-compliance plans that cut the use of coal-fired generation and ramp up the use of wind, solar and other power sources that do not produce GHGs.

This driver has hit a roadblock, however, at least for now. Responding to legal challenges to the CPP by 25 states and several utilities and coal companies, the U.S. Supreme Court on Feb. 9 issued a stay that blocks implementation of the CPP until the legal challenges to it are resolved.

The CPP’s effect on wind and solar development would be over the longer term, though, most likely beginning in 2020 or so. Other factors—the PTC, the ITC, declining wind and solar power costs, and state RPSs, chief among them—will be driving the renewables market for the remainder of this decade.

And how much wind and solar is likely to be added? “Several market analysts predict as much as 10,000 to 15,000 MW of new [solar] capacity in 2016, with continued double-digit, year-over-year increases over the next three to five years,” says DER’s Donley. The outlook for wind is equally upbeat. “My best guess [for the pace of new wind capacity] is between 5,000 and 8,000 MW per year,” says DER’s Peacock.