4Q Cost Report: Pessimism Lingers for Construction Executives

Firms report access to project financing, labor shortages among their top concerns

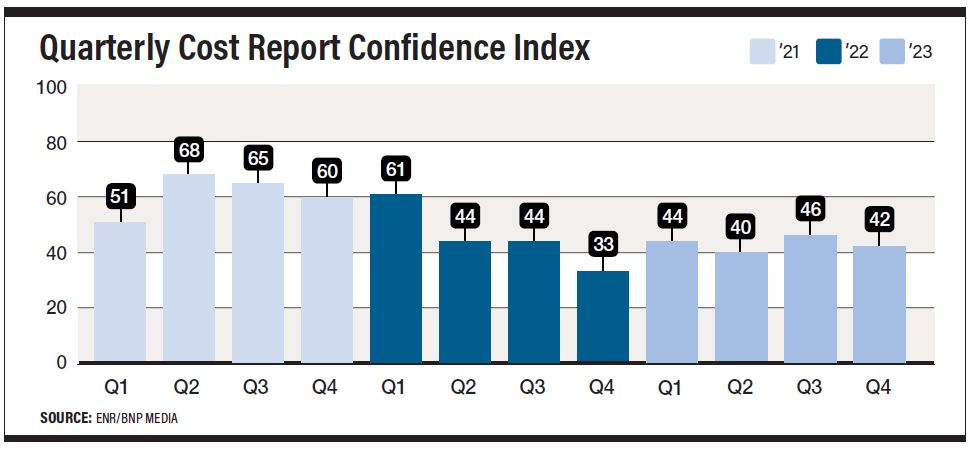

Despite a surprisingly strong economy, construction industry executives report that they enter 2024 with much of the same trepidation they faced at the start of 2023. ENR’s Construction Industry Confidence Index fell four points to a rating of 42 in Q4. Confidence in the economy is also slightly down, to a rating of 38.

The index measures executive sentiment about where the current market will be in the next three to six months and over a 12- to 18-month period, on a 0-100 scale. A rating above 50 shows a growing market. The measure is based on responses by U.S. executives of leading general contractors, subcontractors and design firms on ENR’s top lists to surveys sent between Oct. 30 and Dec. 11.

As with last quarter, confidence is highest among firms who list the Midwest as one of their primary work regions—reported at a stable 51—and confidence in the economy comes in at 42. Most pessimistic are firms working in the Northeast/New England/Mid-Atlantic region, which report overall confidence at a 38 rating, and economic confidence at 34.

ENR survey respondents report relative improvements in materials and equipment prices with 57% noting upward pressure on materials or equipment, down from 60% in the last quarter. That number was 86% in Q4 2022.

CFOs Increasingly Pessimistic

Each quarter, the Princeton, N.J.-based Construction Financial Management Association (CFMA) polls chief financial officers from general and civil contractors and subcontractors on markets and business conditions. The resulting Confindex is based on four separate financial and market components, each rated on a scale of 1 to 200. A rating of 100 indicates a stable market; higher ratings indicate market growth.

The overall Confindex fell 3% to a 96 rating this quarter—down 10.2% from Q1 of this year. The “current conditions” index is down 7.7% to a 96 rating. The “business conditions” index fell 14.7% to an 87 rating. It had been above 100 since Q4 of 2020. Both the “financial conditions” and “year ahead outlook” indices are up slightly, to ratings of 103 and 96 respectively.

The nature of the contractor quandary is changing, according to Anirban Basu, CEO of economic consultant Sage Policy Group and CFMA advisor. Labor shortages are still a pressing concern, but a growing number of firms are worried about future demand for their services, the economist explains.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

“Only 17% of [CFMA Confindex] respondents this time said that they are not concerned at all by demand for construction. That’s different,” he says. “Because anytime you walk into a room with contractors, what did they tell you? We’re busier than ever. All of a sudden, that narrative is starting to shift.”

Access to financing appears to be a primary driver of that shift—with 88% of CFMA survey respondents having at least some concern about availability of financing for projects. About 64% of ENR survey respondents report that client access to financing is somewhat or much tougher than it was six months ago.

CFOs are watching their firms take on a lot of cost to work through their backlogs “and now I might have a period [where] the revenues don’t match up with the expenditures,” Basu says. “I’m trying to warn CEOs about these dynamics with [them] saying, ‘We’re still busy. It’s not time to cut back on costs’, and so this tension is starting to build.”

The economist also stresses that concern is highest among those contractors that depend on independent private developers to generate demand for their services, particularly those who specialize in commercial offices. Confidence in that market sector rose three points in Q4, according to ENR survey respondents, but remains at an anemic 22 rating.

Confidence remains strong in the transportation market at a 78 rating, power is at 74, healthcare is 67 and water supply is 66.

Debt Maturity Wall Looms

About $1.5 trillion in commercial mortgage backed securities is set to hit the debt maturity wall in 2025, leading to fears of a commercial real estate crisis.

For these building owners “2025 comes and you’ve got a totally different debt service payment. The value of that building as collateral is now less than what you owe,” Basu explains. “You might be tempted to throw your keys to the bank and call it a day.”

According to Neil Shah, president and CEO of CFMA: “The last time we saw that was during the [2008-2009 financial crisis]. The only confounding factor that’s different this time is our return to office policies, and that’s going to probably exacerbate it.”

In 2008-2009, banks were left holding single-family residences, assets that there would ultimately always be a demand for. “But this is different,” says Basu. “These are discretionary assets. [Businesses] don’t necessarily have to have workers go back to the office. Contractors know this. They’re praying for people to go back to the office, but it’s just not going to happen. Why should it?”