2023 3Q Cost Report

High Interest Rates, Labor Woes Persist in Third Quarter

Supply chain issues have lessened as the year-end approaches

Related Link:

ENR 2023 3Q Cost Report PDF

(Subscription Reguired)

As the construction industry continues to grapple with the difficulties of the last several years, some sectors have fared better than others, and experts predict there is still some time to come before these issues have been settled.

“The construction sector is running into a headwind as the weight of higher interest rates, labor shortages and tighter lending standards restrains activity,” says Richard Branch, chief economist at Dodge Construction Network. “Unfortunately, these issues are unlikely to see a quick resolution.”

Branch predicts that while rate hikes are unlikely to continue, “the Fed won’t start cutting rates for some time—possibly not until the midpoint of 2024. As a result, construction starts will be under pressure for the next several quarters, ending 2024 down and not gaining strength until the back half of next year.”

Residential Starts Sluggish

In the residential sector, starts are “languishing”, says Branch. With mortgage rates at nearly 7%, demand for single family homes remains low after reaching its lowest point earlier in the year, and Branch expects the remainder of the year to follow suit.

Multifamily starts have fallen since peaking at the end of last year. However, says Branch, “Multifamily projects continue to enter the early stages of planning at a modestly positive rate. This suggests that as monetary policy eases in mid-2024, multifamily starts will see renewed growth.” The largest multifamily projects to break ground this quarter were the $1-billion Clarkson Square condominiums in New York and the $530-million Hub on Campus in Knoxville, Tenn.

“The Fed won’t start cutting rates any time soon—possibly not until the midpoint

of 2024.”

Richard Branch, Chief Economist, Dodge Construction Network

Non-residential starts are down 9% year to date, according to Dodge data. Commercial starts have dropped 8% in the same time period, which Branch attributes largely to declines in the traditional office space and warehouse markets. Data center starts continue to be a “bright spot,” while institutional starts rose 3%, largely due to education construction.

“After starting the year with a flurry of activity, manufacturing starts have settled back as project delays seemingly mount,” Branch says, but he adds that “while they have slowed, the level of starts so far this year is well above historical norms.” The largest non-residential projects to begin construction in the third quarter were the $2.5-billion John Palmour manufacturing facility in Siler City, N.C., and the $2-billion VinFace electric vehicle plant in New Hill, N.C.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

The infrastructure sector “is countering the negativity in the building markets with starts up 22% on a year-to-date basis,” says Branch. “This momentum should continue for the next few quarters provided that Congress is quickly able to come to terms on spending for the next fiscal year.”

Supply Chain Issues Ease

After years of difficulty through the COVID-19 pandemic, the supply chain has largely steadied, says Greg Casper, director of estimating at design and construction firm CRB. “On the aggregate, costs have been stable when compared to the volatility of recent years. Extended lead times remain for things like switchgear and transformers, but the supply of most commodities seems to have stabilized,” he says.

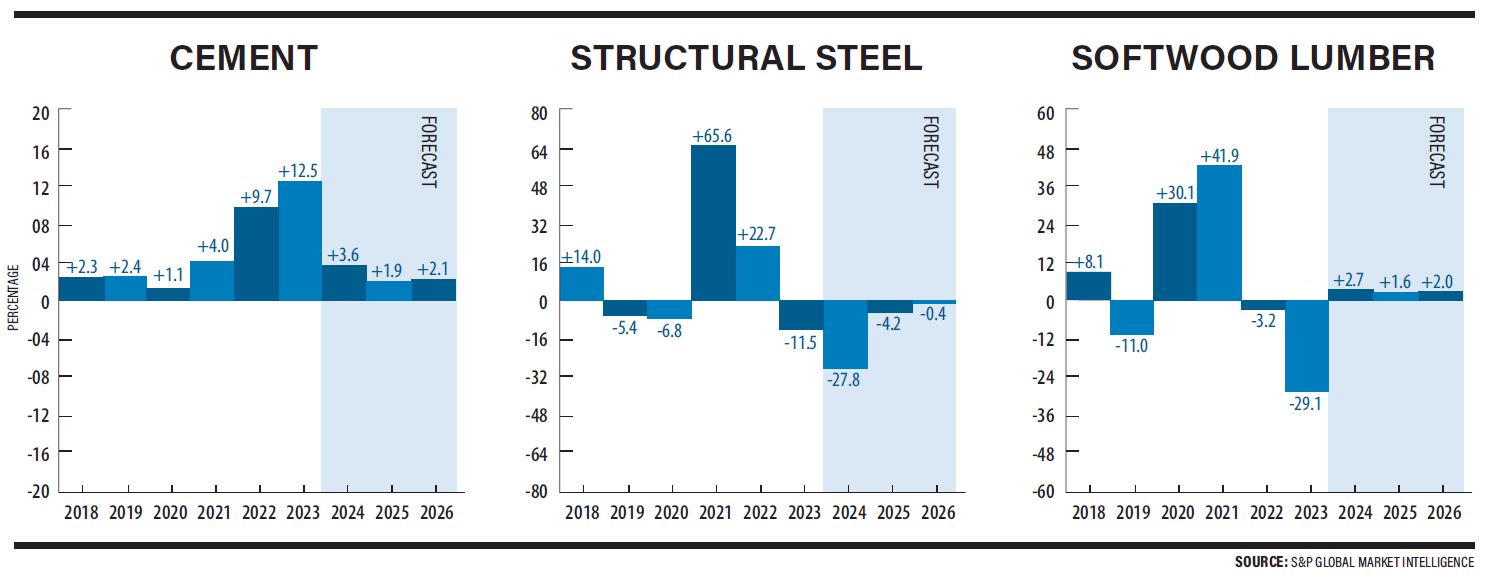

In terms of pricing, S&P Global’s third-quarter forecast predicts a 18.6% overall drop in plywood prices in 2023, followed by a further 4.7% decline in 2024 before rising 1% in 2025. Softwood lumber prices are forecast to finish out this year down 29.1%, then increase 2.7% in 2024 and an additional 1.6% in 2025.

“Softwood lumber prices are expected to return to more typical seasonal patterns in 2024 after years of disruption,” says Luke Lillehaugen, senior economist at S&P Global.

Due to the sharp swing in interest rates in the last few years, “a significant number of people ... can’t afford to sell their home because their budget now wouldn’t go nearly as far. Consequently, there are historically low numbers of existing homes on the market,” Lillehaugen says. “While the demand for houses is lower than it was in recent years, there is still modest demand for buying homes. But because historically low levels of existing homes are available for buyers, this demand has to be met with new residential construction, which is the primary demand driver for lumber.”

He adds: “This will keep softwood lumber demand high enough that prices won’t see significant declines in the near future and growth will return in 2024.”

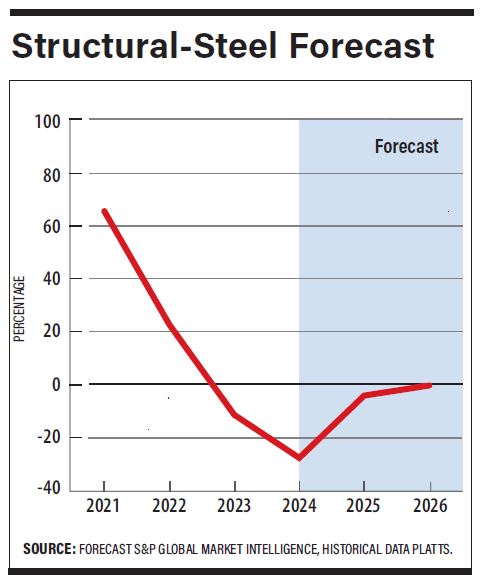

Prices for steel sheet are “nearing bottom” in the U.S., says John Anton, director, market intelligence at S&P Global. “For all other [steel] products, wait as long as possible,” he says. “Prices are far above sheet even though production costs are similar or lower. Bar, rod, structural and plate prices are declining slowly but steadily. They probably do not hit bottom until mid- or late 2024.”

However, when it comes to buying steel outside of the U.S., “the story is very different,” says Anton. “This is a good time to buy, although there is little urgency. Prices are so low that they cannot fall more without mills sustaining losses, but demand is so tepid that there is no upside pressure. Risk is low but asymmetric to the upside. For risk reasons alone we place a weak recommendation to buy now.”

.webp?height=200&t=1671747499&width=200 "4Q Cost Report Economics")