Equipment Makers Prepare for Tariff Fight

Heavy equipment manufacturers such as Caterpillar are already facing increased production costs in the U.S. from tariffs on imported steel.

PHOTO: CALLAGHAN O’HARE/BLOOMBERG VIA GETTY IMAGES

Strong sales across the board in the equipment sector may face price pressures due to tariff actions and trade disputes.

PHOTO: JEFF RUBENSTONE FOR ENR

While larger U.S. manufacturers may be able to absorb costs from tariffs, makers of small equipment and attachments are more vulnerable.

PHOTO: JEFF RUBENSTONE FOR ENR

When the U.S. Dept. of Commerce announced new tariffs on imported steel and aluminum in March, the construction industry’s initial concern was inflated building-material costs. But in the months since the tariff debate began, the reality of new surcharges on all sorts of imported materials and finished goods has begun to reverberate through the global supply chain for construction equipment. Facing a jump in steel prices and tariffs on crucial components imported from abroad, manufacturers and dealers are beginning to reevaluate their options in what was already a bull market for construction equipment sales.

“Everyone loses in a global trade war.””

– Kip Eideberg, AEM

“Everyone loses in a global trade war,” says Kip Eideberg, vice president with the Association of Equipment Manufacturers, an industry trade group representing more than 1,000 U.S. equipment makers. “Tariffs are taxes on American consumers and businesses: They add costs to the manufacturer and affect U.S.-based manufacturing’s ability to compete globally.”

After the Commerce Dept. announced its 25% tariff on steel and 10% on aluminum, the effects on U.S. construction were felt immediately (ENR 7/2 p. 16). Since March, real price increases hit the steel sector. Hot-rolled coil prices, for example, were up 48.9% year-over-year, according to July data from Platts S&P Global (see p. 17). Some construction equipment manufacturers didn’t wait to see the effects on steel prices and adjusted their pricing immediately following the first mention of tariffs by the Commerce Dept. Terex announced an across-the-board surcharge on its U.S. equipment shortly after the first news of the tariffs. In a letter to customers, CEO John Garrison wrote that “the longer-term impact of the trade action is uncertain, but the inflationary impact on steel prices and related components is already increasing our product cost.”

Since then, other major manufacturers have hiked prices to reflect higher up-front costs of steel and other materials and products, citing the tariffs and related uncertainties around global trade policies as a major factor.

“As a global manufacturer, Caterpillar has long advocated for free trade because it enhances global competitiveness and helps U.S. manufacturers grow U.S. jobs and exports,” Cat CEO Jim Umpleby told analysts and reporters during the company’s second quarter 2018 earnings call on July 30. He outlined the impact of the jump in steel prices on Cat’s business. “Based on the current situation, we’ve assumed incremental tariff-related costs of $100 million to $200 million for the rest of the year.”

But a large manufacturer like Cat can absorb a hit like that, and Umpleby remained upbeat about the near future. “Even with these new costs, we are raising our 2018 outlook. We are confident that our strategy positions us to capitalize on current market opportunities and manage through dynamic environments,” he explained. Caterpillar declined to comment further to ENR on the tariff issue and the company’s response strategy when contacted.

Among the larger equipment manufacturers, the immediate impact of tariffs and possible trade restrictions are not necessarily seen in balance sheets, where rising costs are offset by strong sales. John Deere and Co. has been more concerned about how China’s tariff on U.S.-produced soybeans affects the agricultural market. Still, the company has adjusted prices within its construction equipment division. Citing rising production costs, Deere put in place what effectively was a price increase on its construction equipment starting in July by reducing the available discounts on new machines through year’s end.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

“I think on the construction side we have continued to see a pretty competitive market,” said Deere Vice President Ryan Campbell in the company’s third quarter earnings call on August 17. “We saw the benefit of that [discount reduction policy] in July and our expectation is that we’ll continue to see that benefit in the fourth quarter. And as we begin to think about model year ’19, we’ll continue to look at the market base, what is going on. And cognizant of the fact you got material prices and other things moving up.”

Steel accounts for roughly 10% of the manufacturing cost in large construction equipment, according to AEM’s Eideberg, and a jump in steel prices when negotiating purchasing contracts can seriously cut into manufacturers’ margins. But the tariffs on specific components worry AEM member companies even more. In addition to the tariffs on steel, the Commerce Dept. also undertook a Section 301 tariff action, saying it was investigating issuing additional tariffs on a long list of components and parts imported from China. Announced in April, the list of goods covers $50 billion worth of imports a year, including machinery components used in a wide range of U.S.-made construction equipment.

The issue of the so-called 301 tariffs came up during a Senate hearing with Commerce Secretary Wilbur Ross on June 30. Sen. Chuck Grassley (R-Iowa) asked Ross how the Dept. of Commerce might distinguish between product codes for auto parts in the tariff schedule when the same codes are used for components in “similar products such as heavy-duty trucks, buses, construction equipment, agricultural equipment and industrial engines.” Grassley cited as an example, “Water pumps used in the cooling system of construction equipment are classified as ‘fuel, lubricating or cooling-medium pumps for internal combustion piston engines,’ ” and would be subject to the tariffs. He pointed out to Ross that “the harmonized tariff schedule code does not differentiate between auto and construction-equipment parts.”

In response, Ross deferred, saying that the tariff investigation was still ongoing and he could not offer a definitive answer. He did, however, note that “the intention is to deal with automotive parts, not to deal with parts throughout the economy.”

Looking back on that particular exchange, AEM’s Eideberg sees an opening for the construction equipment industry to carve out an exemption from the 301 tariffs. “We think this inadvertently hit construction equipment,” he says. “This seems to have targeted the automotive industry, but we use a lot of the same codes as the automotive industry for parts and components.” But so far the group’s lobbying has not resulted in a formal action or exemption from the Commerce Dept.

Supply-Chain Complications

Duties on specific components can have unexpected effects on the costs of machines that were designed around a global supply chain. Some parts are not manufactured in the U.S. at any sort of usable scale. Most small diesel engines found in compact equipment, for example, are sourced from South Korea or Japan.

Eideberg also cites the specialty high-strength steel used for applications such as the roll-over protection systems in equipment cabs, which many OEMs currently source from Sweden and Finland. “Things like that simply aren’t made here,” he says. As trade barriers are erected and tariffs are applied to imported specialized components, there may be no U.S.-based manufacturers that can step in and offer competitively priced options, he says.

U.S.-based equipment manufacturers were in a relatively good place at the end of 2017, says Eideberg, based on AEM’s own data. Strong order books complemented newly realized benefits from the recent tax reform bill. But the tariff actions have upended all that. “Any of those benefits [from tax cuts] have been wiped out, primarily from the cost of U.S. steel from tariffs, and the increased cost of parts and components from the 301 tariffs on goods out of China,” say Eideberg.

But while large firms can absorb higher up-front costs and count on their booked sales to carry them through rough quarters, that lag can disguise much more serious long-term problems, says Eideberg. “Some of the impact of these tariffs are still hidden. There’s a lot of momentum going on, a lot of orders already in, orders being filled with steel purchased from last year. But obviously as we go into next year and after that, we’ll need to buy new steel, and that will be a real challenge.”

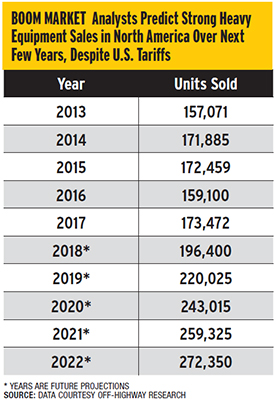

Storm Clouds for an Otherwise Sunny Market

The confusion surrounding the current U.S. trade policy comes at a time when U.S. and global equipment manufacturers were expecting a period of steady positive sales. The construction equipment world has been in the midst of a period of strong performance, and this added uncertainty is an odd aftertaste for what had been a booming market.

“The [global construction equipment] market is going fairly well at the moment,” says Chris Sleight, managing director at U.K.-based analyst Off-Highway Research (OHR). “Globally, we forecast 12% growth [in the heavy equipment market] this year, and that’s after 27% growth last year. Markets are now in a good place after a couple of bleak years.”

Sleight says that the strong markets may delay the signs of trouble from tariffs and price increases for materials and components, but the effects can be felt down the road. “Most large manufacturers have contracts in place to purchase steel at a certain price. It is a very long-term effect.” But when those agreements run out and new prices are agreed upon, the material costs could be passed on to equipment buyers.

According to OHR’s data, sales volumes and prices for construction equipment have risen steadily over the last years, not only in the U.S. but in most other world markets as well. And despite the effects of the tariffs, OHR is still forecasting steady growth in equipment sales in the U.S. and other regions through at least 2022.

“It’s hard to put numbers on how tariffs will shave growth,” says Sleight. “The demand is still there. I don’t expect demand to falter, but growth will not be as high as could be if tariffs were not in place.”

If the tariffs remain contained largely to up-front components and materials in the U.S., Sleight says major OEMs will likely shift production of machinery to other territories than try to absorb the cost at U.S. manufacturing facilities.

“If [U.S. tariff policy] pushes up costs for U.S. production in particular, [construction equipment manufacturers] might say ‘let’s go make them in China or Brazil instead.’”

– Chris Sleight, Off-Highway Research

“We are waiting to see how OEMs react to this if these tariffs are here to say. They are already moving production around the world as needed,” he observes. “If this pushes up costs for U.S. production in particular, they might say ‘let’s go make them in China or Brazil instead.’ That’s one potential change we may see, as manufacturers change where they produce machines so they can still meet demand.”

Having to dodge specific trade barriers could also be the final push for large multinational equipment manufacturers to pull more production out of the U.S., says Sleight. “What I think is the most imminent impact [of the tariffs] is it goes back to where manufacturers choose to build machines.” Manufacturers already are accustomed to moving production outside the U.S. as a cost-cutting measure. “These tariffs and retaliatory tariffs will put U.S. manufacturing at a disadvantage, because dozens of OEMs have facilities around the world. It will tip the balance and they’ll just move out of the U.S. to make the equipment somewhere else,” says Sleight.

Another issue is how manufacturers might react if one type of machine suddenly becomes more expensive to produce. “OEMs might take different approaches,” says Sleight. “For example, if one kind of equipment would be affected heavily, they might not pass on cost and just eat it on that machine.”

The prospect of a trade war with China would also have a negative impact on U.S. equipment manufacturers’ export sales. Relatively little construction equipment is imported to the U.S. from China, but China imports a considerable amount of U.S.-made equipment. According to AEM, the U.S. exported more than $1.5 billion worth of construction equipment to China in 2017. If China decides to place heavy duties on U.S.-made equipment coming in, that could be another blow to U.S. manufacturers.

While Sleight and the researchers at OHR see some ability for global companies to absorb the new costs of a more protectionist mindset, he echoes AEM’s Eideberg’s concern over damage in the longer view. “The point about tariffs is the effect doesn’t come the day after, it comes the year after. The economic impact, the loss of jobs, the loss of business in the community—that is a very long-term effect.”

SOURCE: DATA COURTESY OFF-HIGHWAY RESEARCH

Lobbying and Uncertainty

Equipment manufacturers are still working through backlogs of orders today, and the increase in production costs may not be realized until 2019 in some cases. But that hasn’t kept the equipment dealers and rental shops from worrying about the impact of having to pass along costs to their customers.

Firms concerned about refreshing their fleets are racing against time, according to analysts. Major manufacturers have long-term purchasing agreements in place for steel and other commodities, but once they move through that stock they will likely have to renegotiate at higher prices. And that price jump has equipment dealers worried about sticker shock.

“The tariffs on steel and aluminum from Canada and other U.S. allies and machinery and parts from China pose a significant threat to the construction equipment industry’s prosperity.”

– Brian P. McGuire, AED

“The tariffs on steel and aluminum from Canada and other U.S. allies and machinery and parts from China pose a significant threat to the construction equipment industry’s prosperity,” says Brian P. McGuire, president and CEO of the Associated Equipment Distributors. “While equipment distributors are currently firing on all cylinders, the looming risk of a prolonged trade war is having a negative impact on the industry as manufacturers are increasing prices and contractors are uncertain if economic growth is sustainable.”

Both AED and AEM are currently lobbying Congress and the Dept. of Commerce for relief from the tariffs, which would largely take the form of exemptions carved out for specific industries. But progress is slow, and dealers in particular are worried that customers will delay purchases in the new year to wait and see what happens with prices.

“AED will continue to deliver the message to the administration and Congress that the tariffs are disrupting the supply chain, increasing costs for equipment purchasers and exasperating shortages of new construction equipment to rebuild America,” McGuire told ENR. He emphasized the urgency of the situation for dealers in particular. “Without a resolution in the immediate future, it will ultimately curtail economic growth and job creation in the United States.”

Down on the equipment lots, customers are asking dealers about the impact of tariffs on prices, with a focus on whether it’s time to buy or if they should shift more of their fleets into rentals.

Michael Brennan, CEO of Louisville, Ky.-based Brandeis Machinery and Supply Co., has found himself having to reassure some fairly anxious equipment owners as of late. “We’re very concerned about what our customer reactions will be and how it will affect their buying habits. Every time I talk to one of our customers, that’s the first thing they ask me about,” he tells ENR.

Stable Prices … for Now

Brennan expects the lag on price increases will keep prices from growing too much this year, but his customers are already seeing the impact of rising steel prices in their work. “I’m not so worried about tariffs on Chinese-made equipment—we don’t offer any stuff made in China, but with steel it’s across-the-board. These steel makers in the U.S. have raised their prices. My fear is the inflationary impact of that on the entire industry.”

While he expects the big manufacturers will be able to realign their global supply chains to stay competitive, Brennan says he is more concerned about the smaller U.S.-based companies that produce specialized machinery and attachments. “Some smaller manufacturers we deal with, they have small lines of equipment that are very niche, they are starting to pass on the price increase,” he explains. “They don’t operate globally, they don’t have the ability to absorb the costs. These local U.S. companies—that make this coupler or this bucket or this broom—they don’t know what to do right now.”

If anything, Brennan expects more customers will consider shifting a larger share of their fleets toward rentals in the next year, as higher prices could make refreshing equipment fleets an expensive proposition. “Just being in the equipment business for some time, when you see uncertainty like this, contractors like to rent more; it’s one factor that moves the needle toward rental in this country.”

With typical lead times from the big manufacturers usually in the three- to six-month range, Brennan thinks there’s enough equipment in the pipeline to carry the market through the end of the year. But when his customers press him for answers about what 2019 will look like, he sighs and admits it’s very much a wait-and-see situation. “The manufacturers are all playing it close to the vest at this point,” says Brennan. “We’re asking them to get some answers, we’re evaluating the impact, checking our sources. I take that as people are waiting to see how it all shakes out.”