Next Generation for Nuclear is Big Market in Taking Plants Down

In Wisconsin, the LaCrosse reactor closure continues under a 2015 license-transfer deal between a power co-op and EnergySolutions.

PHOTO COURTESY OF ENERGYSOLUTIONS

Getting started in California, the $4.4-billion San Onofre D&D project could be the largest in the U.S.

PHOTO SOUTHERN CALIFORNIA EDICSON

The $1-billion decommissioning of the Zion nuclear plant in Illinois is 1.5 years ahead of its 10-year schedule, says a cleanupteam executive.

PHOTO COURTESY OF ENERGYSOLUTIONS

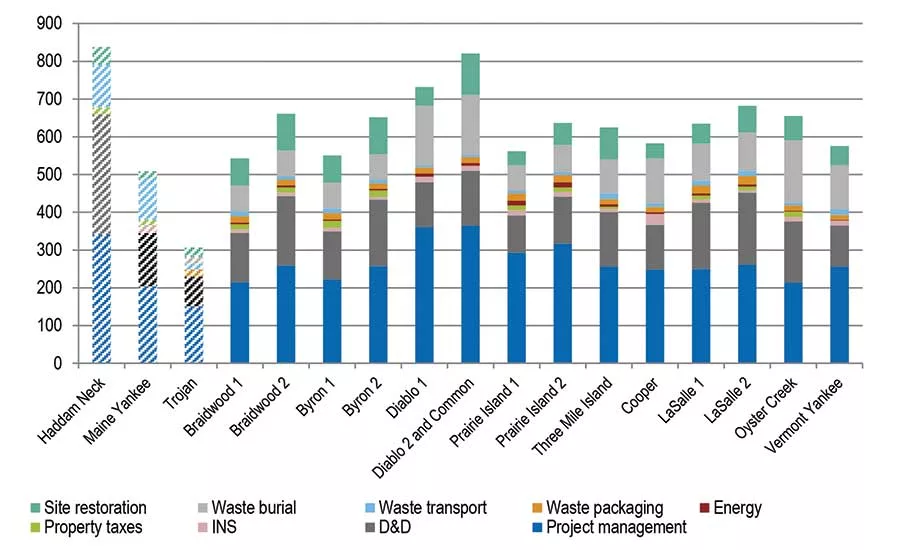

A Look at U.S. Nuclear-site Decommissioning Costs

SOURCE: PACIFIC NORTHWEST NATIONAL LABORATORIES

Crews from cleanup-demolition firm North Star work at an industrial site. The firm has partnered with global nuclear-waste giant AREVA to buy a U.S. nuclear plant and manage its decontamination and decommissioning.

PHOTO COURTESY OF NORTH STAR GROUP

Energy economics and politics may have derailed the “nuclear renaissance” and put operating plants in peril in the U.S. and elsewhere, but low natural-gas prices have accelerated a huge potential market—estimated at up to $200 billion—to clean up and take down nuclear facilities that are uncompetitive or at the end of their useful lives.

The market potential for D&D—decontamination and demolition—is compelling to industry firms with skill and risk appetite for the work.

The market potential for D&D—decontamination and demolition—is compelling to industry firms with the skill and risk appetite for the work, as is the existence of federally required utility funding pools specifically set aside for the task, that firms say could eliminate aging structures quicker rather than have them sit idle for up to 50 while radioactivity decays.

Financial consultant Callan LLC’s latest annual review found that decommissioning “trust fund” balances rose 6%, to $64 billion, in 2016 from the previous year, aided by the strong stock market.

But, regulatory risks and community opposition could still extend—and even derail—prompt cleanup of certain plants, says Paul Patterson, an energy sector analyst with Glenrock Associates.

Even so, industry firms—buoyed by cleanup-fund availability at key sites and the potential of added billions of dollars in work abroad that is being driven by pressure for pre-closure, particularly in Europe and Asia—are forming joint ventures and pushing new financial strategies to pursue the market.

“There’s probably very few if any [companies] that can handle the entire decommissioning process soup to nuts – different vendors that play in that sandbox with various expertise in specific areas," says Mark Richter, senior project manager for decommissioning, at the Nuclear Energy Institute, the industry's advocacy arm. "It's going to take teaming and partnering effectively to do the complete decommissioning. It's certainly a business opportunity for suppliers, it's going to be a body of work in the next 10 or so years.”

NEI is working with the U.S. Nuclear Regulatory Commission on a rule making that would allow plants that are being decommissioned to scale back staffing and security, Richter adds. He says currently, that’s not allowed without a lengthy NRC approval process that can take up to 18 months, requiring “tens of millions of unnecessary cost." According to Richter, a utility spends $1 million a month for every 100 people retained.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

The NRC rulemaking should be complete by 2019 and implemented in 2020, but he says, it's "really going to be too late.”

Last December, Salt Lake City-based nuclear D&D leader EnergySolutions and AECOM, including its market veteran unit URS Corp., won a 10-year cleanup-and-demolition contract to clean up the San Onofre Nuclear Generating Station (SONGS), which closed in 2013. Sited in San Diego County, Calif., the estimated $4.4-billion project, was awarded by lead utility owner Southern California Edison and others, and will be one of the country’s largest D&D efforts, the cleanup firms say.

They are pursuing other takedowns, as well. “It is a growth market. In the next 10 to 20 years, there will be a continuous chorus of nuclear units that are shut down and decommissioned,” says Matt Marston, AECOM senior vice president, who is supervising the operation.

New York City-based cleanup-and-demolition firm NorthStar Group and AREVA Nuclear Materials, a U.S. subsidiary of the French giant, are combining technical, management and regulatory expertise to take on large-scale D&D projects, too. North Star, supported by AREVA as a subcontractor, now is negotiating to buy the Vermont Yankee nuclear plant, in a move it says will speed dealing with regulators, boost cost-efficiency and lower risk.

“For us, it’s business as usual, and we can accelerate the decommissioning time,” says AREVA unit CEO Sam Shakir, who notes the firm’s global experience. “We have a business managing nuclear materials worldwide … from reactor to burial,” he says. “We move fuel between countries and have a recycling facility in France.”

Other companies eyeing the burgeoning market include Bechtel, as well as Canada’s SNC-Lavalin Group, which licenses the country’s CANDU reactor technology and its more efficient uranium-fuel recycling.

The firm’s just-completed buy of U.K.-based design firm Atkins adds personnel familiar with British nuclear sites set for D&D, as well as those in the U.S., says CEO Neil Bruce. Also, in July, it signed a teaming deal with U.S.-based Holtec International to pursue that market and work in small-modular-reactor development.

The U.K. has plans to decommission major parts of its nuclear power complex, but in the wake of a government report last month that outlined private contractors’ management problems at 12 Magnox plants, industry participants are watching whether authorities will outsource nuclear-cleanup procurement or manage it in-house.

Moving to DECON

Firms eyeing the U.S. market are primarily interested in what the U.S. Nuclear Regulatory Commission calls “DECON,” or accelerated immediate decommissioning, rather than “SAFSTOR,” in which plants can sit for at least 50 years while radioactive material decays.

“The market is huge, about $200 billion,” says Ken Roebuck, EnergySolutions president of disposal and nuclear decommissioning.

Decisions to seek D&D contracts are based on both technical and business factors. EnergySolutions’ analysis shows funding to be “robust,” with trust-fund earnings slated to reach $121 billion to $182 billion, plus the U.S. Energy Dept.’s $42 million to pay for spent-fuel management, he says. Plants do not need to go into SAFSTOR while trust-fund interest is accrued, he noted.

There are 13 plants that already have announced closings and 29 more are expected to close—all merchant plants that cannot compete with low natural-gas prices for power production without subsidies. A total of 99 still are operating.

EnergySolutions approached utility company Exelon, which owns a fleet of nuclear plants, to show that it could decommission a plant with a predictable cost and schedule. It hoped that its 10-year decommissioning of the two-unit, 2,080-MW Zion plant in Lake County, Ill., north of Chicago, which was begun in 2010, would jump-start the DECON market.

The $1-billion project, the largest U.S. nuclear plant D&D to date, is one and a half years ahead of schedule and within $6 million of its expected cost, Roebuck says. “Zion has gone well, and it’s a role model setting new standards,” he contends.

Exelon transferred Zion’s nuclear license to EnergySolutions; it will be returned when decommissioning is complete, and the utility company will retain control of spent fuel stored on site.

EnergySolutions owns an integrated packing, transportation and logistics provider for radioactive and hazardous materials, as well as a processing plant near Oak Ridge, Tenn., and the Clive disposal site in Utah for power-plant waste and interim storage of spent fuel.

DECON has been used at the Maine Yankee, Connecticut Yankee and enough other sites to better predict the cost and schedule, says AECOM’s Marston. But selection of the decommissioning method depends on site circumstances. In Waterford, Conn., Dominion Energy’s Millstone Unit 1 is in SAFESTOR because its two other units are still operating.

The most technically risky part of a project has been segmentation and disposal of the reactor vessel. EnergySolutions completed the first large commercial reactor segmentation in the U.S. in 2015 at the Zion plant, cutting the structure with an oxy-prone torch connected to a robotic fixture outside of it.

“Extensive design, analysis, mock-up testing and planning resulted in a fast-cutting sequence with no release of radiation,” said John Sauger, then-executive vice president of Zion Solutions LLC, the EnergySolutions unit managing the D&D. Cutting the vessel into smaller pieces also reduced risk in disposal and transportation. Roebuck says the task took two years of off-site and on-site engineering.

“There’s tremendous opportunity for suppliers to minimize the impact of waste in destruction of the physical plants," says NEI's Richter.

Veterans of Maine Yankee, Zion and of D&D work at U.S. Energy Dept. former nuclear production sites have taken their lessons learned to the SONGS project to mix it with younger workers’ penchant for new technology. “Knowledge transfer is a big deal for us,” Marston points out.

Once all permits have been approved, SONGS demolition is set to begin in 12 to 18 months. Lead utility Southern California Edison in September settled a 2015 lawsuit filed by opponents of an on-site dry-storage plan, allowing the operation to proceed. Work will then begin to move 2,668 spent-fuel assemblies to a just-completed addition to an independent, on-site spent-fuel storage installation from pools in reactor Units 2 and 3.

The previous facility housed 51 stainless-steel canisters entombed in high-strength concrete; now in testing, the addition will house another 73. “The plant has the highest seismic qualifications of any nuclear plant in the country. The dry-storage pads have more than double that,” says Maureen Brown, a SONGS spokeswoman. “Once all the spent fuel is removed from Units 2 and 3, that gives [the D&D crew] access to completely decommission the site,” says James Madigan, technical adviser to the utility’s chief nuclear officer, noting challenges, however, in the tight, 85-acre site.

Brown says the Southern California Edison will maintain ownership of the plant during the D&D: "Our approach to decommissioning leverages the experience of a global joint venture with diverse dismantlement and decontamination expertise while ensuring SCE, as majority owner, retains responsibility as the licensee to manage state and federal regulatory requirements, and direct a safe decommissioning."

Elsewhere in California, crews at the Humboldt Bay Power Plant near Eureka almost have completed demolition of its buried nuclear reactor. Located along the Pacific Ocean, Unit 3 was the first commercial nuclear power plant to feature a below-grade reactor core. Built in the late 1950s, the vessel, housed within a 60-ft-dia concrete caisson, was sunk 80 ft underground and nearly 66 ft below sea level.

Looking Ahead

NorthStar and AREVA have yet to begin Vermont Yankee D&D as part of a deal reached last November under which Entergy agreed to sell NorthStar the 620-MW plant and transfer its NRC license. Plans also include placement of all of the facility’s spent fuel in dry-cask storage by 2018.

Despite continuing disputes over cleanup standards that could add to costs and even scuttle the deal, the firm expects it to close late next year.

NRC and state regulators must approve the transfer. “They are asking us to take a leap before we know what we’re leaping to,” says Chris Recchia, former chairman of a state utility regulatory agency, noting that NorthStar has not done a complete nuclear powerplant D&D project before. The firm has completed five smaller nuclear research reactor decmmissioning projects at university and medical sites, according to its website.

Another question is whether NorthStar lowballed the D&D costs since Entergy’s estimate was $57 million higher.

“Entergy’s estimate was based on an entirely different assumption and approach,” NorthStar CEO Scott State says. “The major risk is project execution, and we have experience on projects larger than a nuclear plant and the nuclear owners do not,” he contends. “It’s a large industrial demolition project with a radiological component.”

The company’s link with AREVA under one umbrella organization is an advantage, say the firms’ chief executives.

NorthStar’s other partners on the project are Burns & McDonnell and Dallas-based Waste Control Specialists, which will store radioactive waste from Vermont Yankee demolition in its NRC-permitted facility. in Texas. The power plant's used fuel will remain on its onsite storage pad until DOE removes it to a yet-to-be-developed federal storage site.

AREVA CEO Shakir says the Waste Control Specialists facility has applied to the NRC to buiid an interim storage site for high-level radioactive spent fuel, which will take several years to obtain.

“The problem is that there is no place to move it," says NEI's Richter. "An interim facility or facilities could be licensed or operational, but until that happens, the fuel is not going to go anywhere.”

He notes: “The greatest challenge with decommissioning is in the regulatory arena rather than technology. [Industry] "is pretty good in terms of tearing things down and breaking them up.”

Entergy had chosen SAFSTOR for Vermont Yankee, with decommissioning to start in 2053, but NorthStar proposed to have it completed in 2026. As a general rule, DECON represents a 10% to 20% savings over SAFSTOR, State says, adding that Vermont Yankee’s trust fund of about $580 million will cover the cost.

NorthStar prefers to buy the plants, which is the utility’s only way to transfer the risk, says AREVA’s Shakir.

Entergy already has announced it will close the 690-MW Pilgrim plant in Massachusetts and the 805-MW Palisades unit in Michigan, although cleanup details have not been aired.

But utility Vice President T. Michael Twomey, noting the cleanup firms’ D&D experience, in-house labor force and vendor relationships, acknowledges that “Entergy’s primary expertise is in operating nuclear power plants, rather than decommissioning them.”