Rebar Prices Slow after Wild First Half

| + click to enlarge |

|

Stabilized pricing on a broad range of structural steel products points to a much less frenzied market in the months ahead after a first-half marked by soaring prices and tight supply. The sharp price inflation that contractors struggled with over the past year has subsided, according to a broad contingent of buyers and sellers.

Demand for steel reinforcing bar, wire mesh and structural plate and beam is driven mostly by construction activity, particularly nonresidential work. While the commercial construction market is still doing well, the decline in new-housing construction has slowed demand for reinforcing bar used in residential construction, forcing some price rollbacks.

The market is “generally healthy” but it’s “not booming,” says a fabricator who supplies rebar throughout the Southeast. “The mills fill my orders a lot faster now,” he notes, adding that “there’s a lot of rebar on the ground.” Domestic rebar production is up about 2.5% this year, according to the American Iron and Steel Institute, Washington, D.C..

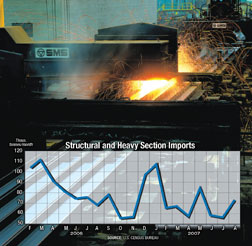

Another buyer points to an abundance of low-priced imported rebar piling up at Houston, Texas, Port Everglades, Fla., and several other East Coast ports. “There’s a lot more import available,” he says, noting frequent offers from traders trying to move the material.

In August, the country’s two largest rebar suppliers—Charlotte, N.C.-based-Nucor Corp. and Gerdau Ameristeel, Tampa, Fla.—decreased their base price for rebar in 20-ft lengths by $20 to $40 per ton, depending on the diameter and grade. Both companies say the price rollbacks excluded the Florida market, where selling prices were already said to be lower than in other states. Even with the Florida blackout, one buyer says Nucor has reduced selling prices in Florida to match competitors’ prices, as well as lower-priced imports.

This was the first price adjustment by domestic rebar producers since the scrap steel surcharge for the mills’ primary raw material was reduced in mid-April, following a series of three successive price hikes that pushed average rebar prices in the eastern U.S. to $624 per ton for standard A-615 rebar. Since then, mill selling prices have fallen back to about $585 per ton. The outlook now is for rebar prices to remain unchanged or edge slightly lower, unless scrap steel prices move up again.

Gerdau Ameristeel President and CEO Mario Longhi says price reductions on 20-ft rebar affect only “a small part of our residential housing business.” He does not foresee any spillover to other grades, such as 40-ft and 60-ft sections, which are primarily used in nonresidential projects. “We could see some pressure on nonresidential products in the back half of the year,” Longhi warns. But he says that is expected to be mostly the result of seasonal factors. .

Gerdau Ameristeel’s average steel prices in the quarter ended June 30 increased $82 per ton, which lifts prices 14.6% above a year ago. Average fabricated steel prices were up $130 a ton from a year ago, according to the company. Gerdau is preparing to take over Chaparral Steel, Midlothian, Texas, later this year, further consolidating the supplier side. Chaparral is the second-largest producer of structural beam in North America after Nucor-Yamato, the Blytheville, Ark.-based unit of Nucor.

Beam and plate prices remained firm for most buyers in August, according to a major steel plate distributor. He says beam and plate producers have done “a lot better than flat-rolled” mills at maintaining prices against deep discounting. This is due to steady demand from the nonresidential construction market, particularly powerplants, infrastructure projects and the office and school construction sectors. McGraw-Hill Construction, of which ENR is a unit, reported in August that total nonresidential construction was up 2% in dollar volume for 2007, giving some relief from the decline in residential construction.

“We expect our beam and plate mills to continue to enjoy healthy demand and post strong results over the second half of 2007,” says Nucor CEO Dan DiMicco. He notes that plate has the strongest demand of all Nucor’s products, and would generate “very attractive” profits.

Plate Is in Demand

| + click to enlarge |

|

Domestic production of structural shapes, including beams, is up about 1% this year but plate production is up 7%, according to AISI. The strong market demand for steel plate prompted Chicago-based ArcelorMittal Steel USA to announce in May that it would restart its 160-in. plate mill in Gary, Ind., which has been idle since 2003. It is to be fully operational this month, following some equipment renovations. The firm also operates two plate mills at the nearby Burns Harbor site in northern Indiana.

Despite the market strength, buyers rejected efforts by Nucor, ArcelorMittal and other producers to raise plate prices by $45 a ton in May and June after prices increased $25 a ton in April. The current transaction price for A36 carbon steel plate is about $800 to 820 per ton in the eastern U.S. for a typically sized spot-market order of 5 tons. However, several buyers say ArcelorMittal has made competitive offers of $790 a ton to attract business to the new production coming online at its Gary Works.

The September scrap-steel surcharge for plate, beam and other structural products was set at $116 a ton by most producer mills in the eastern U.S. The September surcharge represented an $11 increase from August, but it was matched by an equivalent $11 reduction in the base price. As a result the benchmark price for wide-flange 12x8 beams remained unchanged at $770 a ton.

Plate and beam prices should remain at the same level over the next several months. A sharp inflation in scrap prices could change this outlook, but that is not expected by most market observers. “We see scrap going sideways or down with less volatility,” says Nucor’s DiMicco.

There is little risk that contractors will see shortages of rebar or structural steel in the near term, as happened in 2004-2005. Through September, the industry was using only 85% of available raw steel making capacity, down from an average operating rate of 90% in 2006.

Looking ahead, escalating steel prices in 2008 could affect numerous public infrastructure projects, many of which are already delayed due to rising costs. Two important sectors––highway construction and bridge repair––are highly dependent on funding from the Federal Highway Trust Fund. Its highway account will have a projected deficit of $3.8 billion in fiscal year 2009, according to recent estimates from the Office of Management and Budget. Unless this budget gap is closed, further delays may occur in much-needed highway and bridge work.

Lower spending on big public infrastructure projects, combined with a pullback in some commercial construction projects, such as multi-retail shopping centers and multifamily apartment dwellings, could cause rebar and structural steel prices to level from recent highs, even as steel mills crank up production. In 2006, the domestic industry produced 7.4 million tons of reinforcing bar and 7 million tons of steel plate used in bridges. These production levels could be matched this year and next, if the money to finance projects is available.