Firms Are Hopeful But Challenged in KPMG Global Market Outlook

Urban growth around the world will generate big demand for new infrastructure, particularly in the energy sector. But uncertain economic conditions, added project risk and workforce skill gaps will challenge engineering and construction firms to take advantage of new opportunities, says a survey of 161 CEOs and top executives of large global industry companies.

In its 2012 global construction survey, released Jan. 30, management consultant KPMG International says respondents report some performance improvements over the past year, with 56% of the firms noting increased backlog in 2011 and only 18% reporting a decline. Based in a total of 27 countries, firms range in size from $250 million to about $5 billion in revenue.

The survey analyzed all firm responses as well as those from companies in three key regions: the Americas, Asia-Pacific and the Europe-Middle East-Africa (EMEA) sector. Overall, about 53% of executives surveyed were in the EMEA sector; 30% in Asia-Pacific and 17% in the Americas.

About 64% of Asia-Pacific firms report hiked backlogs, while 21% of EMEA firms posted a decline—with Europe's economic woes a key factor, according to KPMG. Backlog margins appear to have fared better, with twice as many firms reporting a 2011 increase over the previous year, says the survey. The largest-revenue firms and those based in the Americas did worst, according to KPMG.

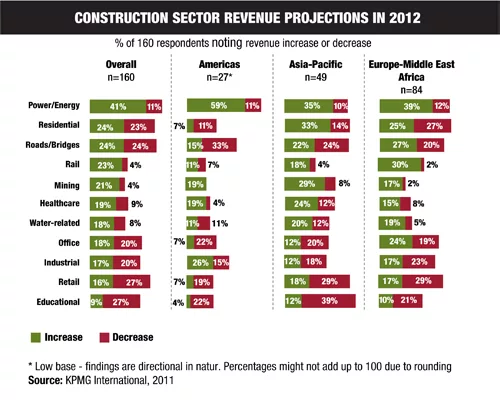

Energy topped the list of market sectors mostly likely to improve revenue, with 41% of respondents predicting an increase in 2012. Residential and roads-bridges construction tied for second, each noted by 24% of executives. Peter Kiss, KPMG power and utilities global chief, notes that long development cycles for energy projects "puts incredible pressure on a manpower base that is already stretched."

Respondents Are Optimistic

Companies still seem to be optimistic despite the changing global economy. Nearly three-quarters of respondents cite economic uncertainty as their biggest ongoing concern, followed by a skills shortage (31%) and government deficits (30%). More than half of the Americas respondents ranked the latter as their No. 2 business concern.

Even so, only 11% of respondents anticipate a backlog decline in 2012; 61% of even the largest firms believe backlog will hold steady. But in noting the continued boom in sector mergers and acquisitions, Tony Bohnert, KPMG's U.S.-based transaction services partner, says, "Historical operating results may be distorted by the recent economic downtorn, which requires even further in-depth analysis of prior operating results, current backlog and projected future earnings."

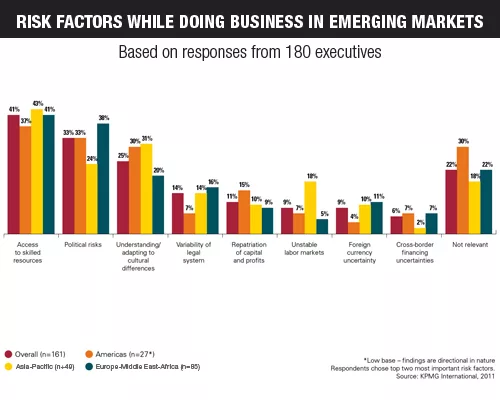

With projects becoming larger, more complex and subject to more global impacts, mitigating risk is a major concern for most respondents. Globally, 45% say that quantifying risks is the chief concern; 52% of those in the Americas say that identifying risk is key.

“Despite considerable investment, risk management still comes up a bit short,” says Geno Armstrong, international sector leader of KPMG’s engineering and construction practice. He says only 36% of those surveyed "believe that their project review processes are very efficient.”