ENR 2023 Top Owners Sourcebook: Owners Caught Between Shifting Markets

November 8, 2023_ENRready.webp?height=334&t=1702394118&width=640)

ENR 2023 Top Owners Sourcebook: Owners Caught Between Shifting Markets

November 8, 2023Designed by Seattle-based design firm NBBJ, Microsoft's new Thermal Energy Center is a sustainable heating and cooling source for the tech giant's Redmond, Wash.-campus, powered by geoexchange technology.

Photo by Sean Airhart, NBBJ

On the surface, an increase in construction in progress spending last year illustrates greater owner confidence in a post-COVID-19 market. But deeper industry challenges still remain. Owners and owner representatives anticipate that higher interest rates, materials costs and limited labor pools will dampen project prospects.

Around this time last year, the construction market had a different set of priorities, says economist Anirban Basu, chairman and CEO of Sage Policy Group.

“Just about every contractor was busy. There wasn’t much discussion about credit tightening. Backlog was elevated for just about everyone, and most major segments of construction were still experiencing substantial spending growth,” he says. “And people were looking forward to 2023.”

In the interim, Basu says there has been a shift that has widened the disparities between sectors and what opportunities are available for owners. “Some segments of construction have weakened, meaningfully,” he explains, “while others have been becoming stronger. Therefore [there are] growing disparities in performance across the construction industry.”

The X factor driving many sector disparities has been megaprojects, says Basu.

“This is the era of the megaproject. And perhaps people realized that a year ago, but many of these megaprojects have now actually broken ground,” he explains, which has resulted in a greater strain on limited construction resources.

Related Links:

ENR 2023 Top Owners Sourcebook (PDF)

(Subscription Required)

ENR 2023 Top Owners Sourcebook (Articles)

Economic Transformation

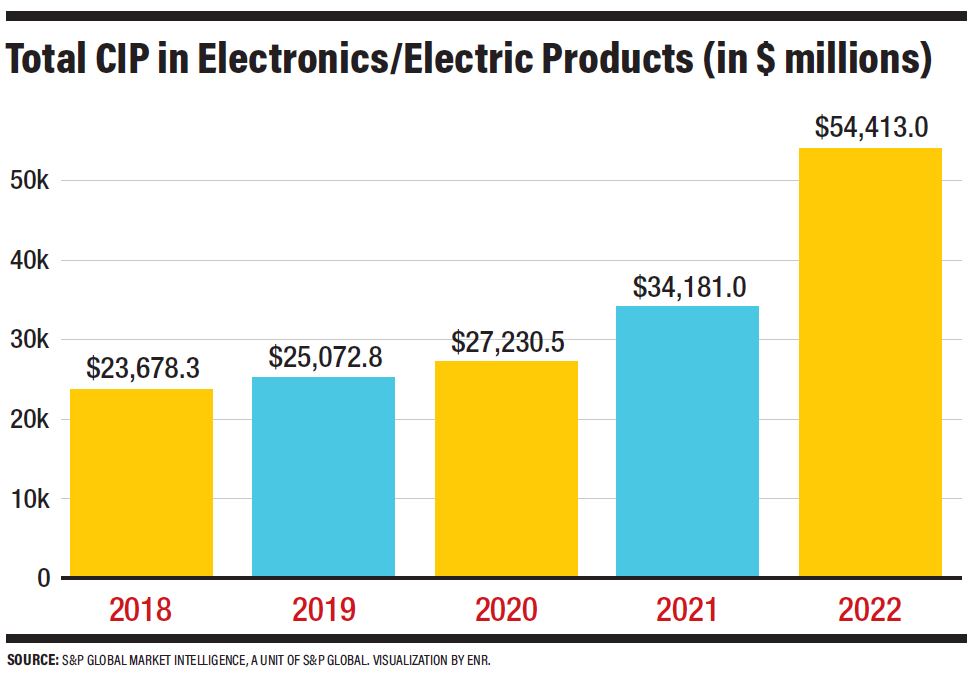

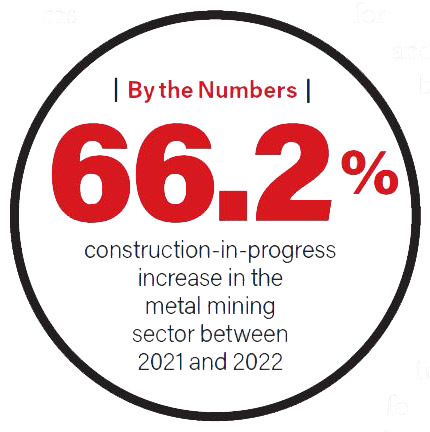

Overall, construction-in-progress spending has increased 24.1% this year, up $506.59 billion from $407.74 billion last year. The largest spending increases are in the areas of metal mining (66.2%), photographic, medical and optical goods (63%) and electronics and electric products (59.2%). On the other hand, there have been decreases in paper and allied products, petroleum and coal products, and amusement and recreation services.

Yet Basu argues that construction spending is “not so much a function of economic growth” as it is a function of “economic transformation.” He adds: “The economy is transforming in major ways, and not surprisingly, that coincides with major construction projects, otherwise known as megaprojects.”

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

While some supply chains are back moving at pre-pandemic levels, some companies, such as General Motors, have chosen to invest in their manufacturing abilities to reduce reliance on international supply chains, Basu explains.

“That is generating some enormously impactful construction projects related to the manufacturing sector—and that sector, not coincidentally, has generated more construction spending growth than any other segment of nonresidential construction during the pandemic and subsequent recovery period,” he says. “That has been in many ways driven by a combination of CEO decisions regarding supply chain locations amidst various logistical issues and public policies being promulgated by the federal government.”

Public spending in the form of the $1.2-trillion Bipartisan Infrastructure Law and the $280-billion CHIPS and Science Law has also boosted work for contractors connected to infrastructure and energy sectors, says Basu. A desire for the private sector to simplify logistics and better protect intellectual property, combined with federal government subsidies to promote reshoring, resulted in “a boom in manufacture related construction,” says Basu.

“Again, [it’s] not necessarily a function of economic growth or global economic growth; more a function of economic transformation,” he explains.

Rosy Outlook

Despite the Federal Reserve’s attempts to slow economic growth with higher interest rates, and fears of an impending recession, last month the Commerce Department reported that the economy expanded at a 4.9% annual rate from July through September. Gross domestic product output indicated that consumers seemed to have a rosy economic outlook, indicated by increased spending.

In the construction market, Basu explains that an impending influx of infrastructure projects are having the same effect on the market.

“The Bipartisan Infrastructure Law was signed by President Biden in 2021. A year later, not many of these projects have moved forward,” says Basu. However, there is anticipation that more of those projects will enter the shovel-ready phase in the next few months. “So the outlook continues to be quite rosy, for those infrastructure-oriented contractors,” he says.

For sectors more susceptible to higher interest rates, Basu says owners will have to weigh the greater risks against the rewards of moving forward with their projects. “And so a year later, it is really those developer-driven activities that are beginning to really stumble,” he explains. “Those developers are more sensitive to interest rate increases, and they’re finding project financing much more difficult to acquire.”

The result is an increasing dichotomy between developer-driven segments and publicly-financed segments, with publicly-financed segments continuing to offer lots of opportunities while the developer-driven segments are winding down in terms of momentum.

In segments such as office space, Basu says demand “will never come back to the way it was,” due to many companies adopting a hybrid work model or scrapping their office spaces altogether.

“What can happen, however, is that you could have at some point in the future an equilibrium between the demand for office space and its supply,” he says.

Labor Pains

Owner capital project teams are being stretched thinner and thinner, says Greg Sizemore, executive vice president of the Construction Users Roundtable (CURT). Not only are labor resources increasingly scarce, but the scale of their projects has increased. “I have never seen so many mega large [$1-billionplus] projects in my life,” says Sizemore. “That used to be big news. Now it’s common.”

The competition for talent is fierce. Sizemore, who also teaches in the University of Cincinnati’s construction management program, relates that 85% of his seniors already had signed job offers in hand when they walked into his classroom in August.

For owners, attracting talent often comes down to offering fulfillment and a sense of purpose, says Howie Ferguson, executive director of the Construction Owners Association of America. “I’m not saving someone’s life, but maybe I’m helping build a better [medical] facility so a patient has a better experience. That matters.”

Charles Hardy, chief architect of the U.S. General Services Administration, also sees opportunities for professional growth as an advantage for owners. He explains, “You’re not going to come to the GSA and become the stair guy in an architectural firm kind of thing. You’re going to do a lot of different projects.”

It’s the labor shortages facing their contractor partners that can put owners’ projects most at risk, however, says CURT director of strategic initiatives Daniel Groves.

Groves calls labor risk the “overarching concern” for all projects. “There is not a sufficient level of engagement with contractors [during pre-construction planning] to ensure that labor risk is identified, and then an appropriate process put in place to manage it or avoid it,” he says. Subcontractors are already evaluated for safety and their financial and insurability capability but “very, very little” is done in the area of workforce and training, he adds.

Tracking Workforce Development

Duke Energy is increasingly looking at workforce development when evaluating contractors, says Andy Browning, general manager of engineering and construction services at the utility company. “What are you doing as a company to help develop the next round of craft that’s gonna benefit me? Because I see the need coming,” he says. “If you do it, and your competitor doesn’t, then it’s my responsibility to give you a leg up because you’re helping the issue.” Otherwise, that competitor’s lower overhead will give them an advantage, he adds.

Carnegie Mellon already includes workforce development in its RFPs, says Andrew Reilly, the university’s senior director of engineering and construction. “If you don’t track it, it doesn’t happen. So we’re tracking it monthly on large projects and twice a year on small projects,” he says. When the owner requires metrics-driven accountability, the higher up-front cost ends up becoming a return on investment, says CURT’s Groves. “The investment in the workforce produces a workforce more likely to operate on schedule, within budget, safer and so on. There’s a lot of data to support this,” he adds.

Groves also calls for collaborative opportunities to overcome labor risk. “We see contracts that have fairly onerous penalties built into them for missing certain milestones,” he notes. “When you have serious workforce challenges, and workers get drawn to more financially attractive projects, you’re going to miss schedules,” he says. Inevitably those costs will flow back to the owner. “[Contractors are] going to say: ‘We’re going to build in the costs of missing the schedule, because we know it’s impossible’.”

Contractors are already functionally financing many projects due to payment terms, Groves opines. “When contract terms and conditions state that the contractors will be paid in 90 or 120, or 175 or 180 days, that becomes very painful to those contractors, particularly the smaller ones.” Those costs too, will be built into rates over time, he says.

Work Packaging

At the Construction Industry Institute, an organizational best practice called “effective work packaging” has emerged among its member firms as a way to address limited labor resources while keeping jobsites safe and efficient, says executive director Jamie Gerbrecht.

“They are implementing the fundamentals of that practice to really bring about efficiency and effectiveness in project planning and execution that will make a positive difference for them,” he explains.

Because the practice addresses delivering the right work with the right amount of workers at the right time throughout the project lifecycle, Gerbrecht says that everyone benefits from its implementation. “Ultimately, it creates an environment where you are helping the project to achieve its objectives. We know that first objective, most importantly, is about safety. But then it’s also about productivity, cost, scheduling, quality, predictability.”