Confidence Index

2023 1Q Cost Report: Construction Execs Are Wary, But Their Confidence Still Rises

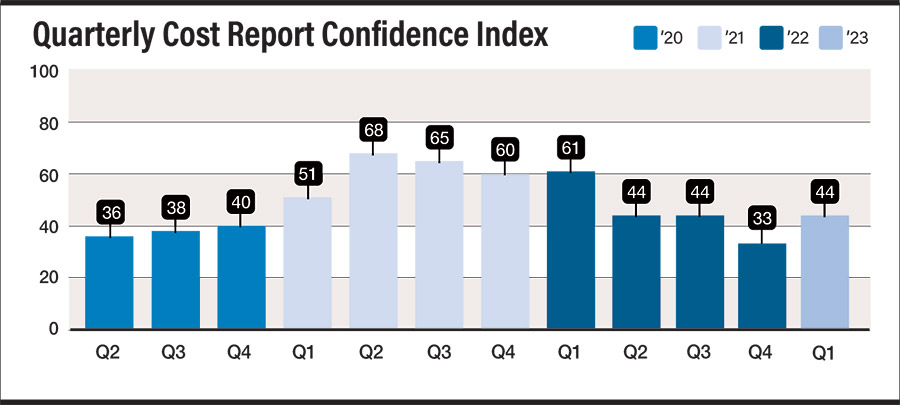

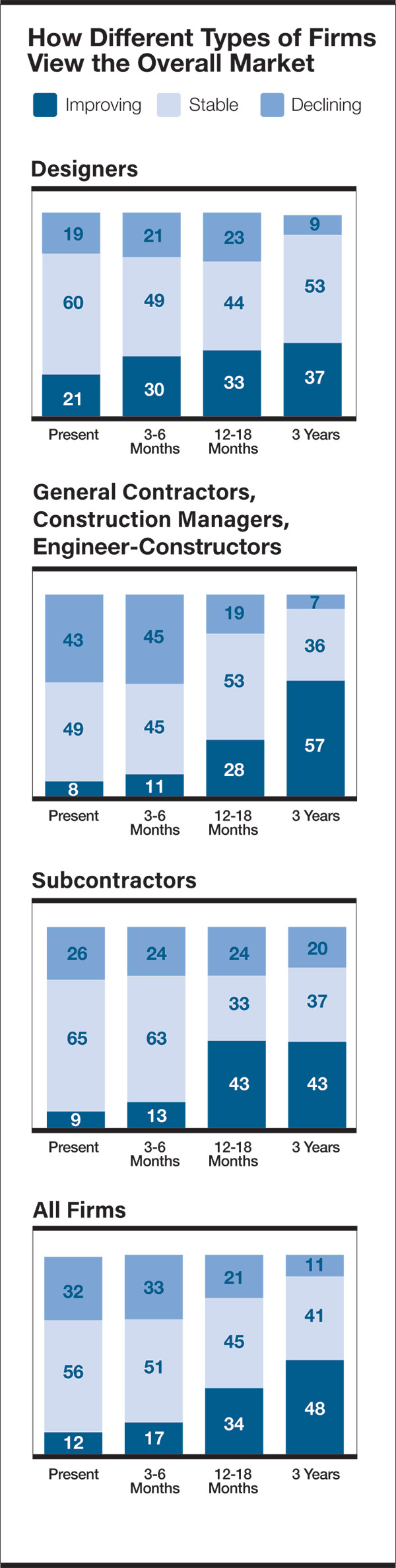

With the economy so far navigating through recession risks, ENR’s Construction Industry Confidence Index shot up 11 points this quarter to a cautiously pessimistic 44 rating, with 68% of survey respondents seeing the current market as either stable or improving, up from 62.7% last quarter.

The index measures executive sentiment about where the current market will be in the next three to six months and over a 12- to 18-month period, on a 0-100 scale. A rating above 50 shows a growing market. The measure is based on responses by U.S. executives of leading general contractors, subcontractors and design firms on ENR’s top lists to surveys sent between February 6 and March 13.

Related link: ENR 2023 1Q Cost Report PDF

Subscription Required

Construction executives’ faith in the economy as a whole has also rebounded significantly, although they are still pessimistic on the whole. The economic index jumped 11 points to a 35 rating, its best since Q1 of last year. For the last quarter, 62.2% of respondents saw a declining economy. That number fell to 41.1% this quarter. The near-term economic outlook is also brighter than last quarter. The percentage of respondents who see either a stable or improving economy three-to-six months from now jumped from 30.6% last quarter to 52.6% this quarter.

Confidence in individual markets is a mixed bag this quarter. Execs are most confident in the water, sewer and waste market, which was up four points to a 74 rating. That is the highest confidence rating on record for the market. On the other end of the spectrum, the distribution-warehouses market continued tumbling, down seven points to a rating of 46. That is the market’s lowest rating since Q4 of 2011 and a 32-point drop from a year ago.

Results of the latest Confindex survey from the Construction Financial Management Association (CFMA) shows increasing optimism among construction CFOs. Each quarter, those from general and civil contractors and subcontractors are polled on markets and business conditions.

The Confindex is based on four separate financial and market components, each rated on a scale of 1 to 200. A rating of 100 indicates a stable market; higher ratings indicate market growth.

The Confindex rose 3.9% between Q4 2022 and Q1 2023, to a rating of 107. All other indices are also up. The “current conditions” index rose 2.8% to a 112 rating. The “business conditions” index is up 1% to 104. Most notably, the “financial conditions” index increased 5.8% to a 109 rating—up 3.8% in comparison to the March 2022 ConfIndex reading.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

“[The financial conditions index] is precisely the indicator one might have expected to be most negatively impacted by the Federal Reserve’s goal of reducing monetary accommodation,” says Anirban Basu, CFMA advisor and CEO of Sage Policy Group. “Yet money still seems to be available.”

Association CEO Stuart Binstock points out that “everyone is anticipating [recession], but these numbers don’t reflect it.” He notes that profit margins are up slightly in the Confindex survey results, and reported material prices have improved significantly.

Basu does not see the rollout of Infrastructure Investment and Jobs Act money as a primary driver in the relative optimism of construction CFOs. “A lot of [those] projects remain in the planning stages,” he says. “One of the things that has departments of transportation on the back foot is that the costs are so much higher than they anticipated.”

The results of AGC’s 2023 Construction Hiring & Business Outlook survey showed that 11% of respondents said they had either worked on or won bids for projects funded by the law, while 21% planned to bid but nothing suitable had been offered yet.

Recession-Resistant Construction?

Economist Basu instead attributes at least some of that optimism among CFOs to what he calls “the era of the mega construction project.” He says that “the level of construction activity is not so much dictated by the level of economic growth, that’s a factor, but by the level of economic transformation.” Basu also sees the pandemic era as a highly transformative one.

Supply chain issues have pushed companies to reshore and near-shore, leading to an explosive growth in the manufacturing sector. “There’s not even a close second [among non-residential construction categories],” Basu adds. “You see $200 billion of development in computer manufacturing plants, $40 billion of battery manufacturing plants in development. A lot of contractors in Texas, Arizona, New York, Ohio are going to be swamped with work, even if the economy enters recession later this year.”

Basu expects to see a greater disparity in performance across contractors during the years ahead. “Contractors in those communities who are not fed by megaprojects stand to see a deterioration in performance,” he suggests.

The Sage CEO also sees an increase in mergers and acquisitions on the horizon, despite currently high interest rates. “You are going to have some contractors who are way too busy and other contractors with now excess capacity,” he says.

Related links:

2023 1Q Cost Report: Intro

Bank Failures, High Interest Rates Stoke Recession Fears

Construction Execs Are Wary, But Their Confidence Still Rises

Executive Pay Saw Significant Increase Throughout 2022

Demand for Heavy Equipment Remains Strong as Prices Show Signs of Stabilizing

Materials Costs Remained Elevated Overall at Year’s End