Fixing Construction's Fixed-Price Conundrum

illustration by Scott Hilling for ENR, original elements courtesy of Getty Images

Florida’s I-4 project P3 team seeks $100 million more to finish work. Two of its contractors now are exiting fixed-price work.

PHOTO: FLORIDA DOT

Montreal's fixed-price REM light-rail project, which will require deep tunneling in a tight urban environment, is on track, says the builder.

PHOTO: RESEAU EXPRESS METROPOLITAIN

Contractors set to build the planned $30-billion Rovuma LNG project in Mozambique seek more risk-sharing with clients.

The largest single road construction project in Ohio history could have taken decades and busted the budget at the state Dept. of Transportation had it been executed traditionally.

But the state opted for a public-private partnership (P3) that brought in investors to share execution and financial risk at a fixed price.

Completed last December in less than five years, the $429-million Southern Ohio Veterans Memorial Highway project was handled by a Dragados USA Inc.-led team that also will manage operations and maintenance over 35 years, which could boost total project payback to $1.2 billion to the P3 members.

“It allowed us to minimize risk on a very expensive but needed project,” says ODOT project manager Tom Barnitz. “The team benefits by contracting a larger project of higher value with an opportunity to innovate new methods.”

Chad Ratkovich, senior project manager at Beaver Excavating Co., Canton—an equity member of the design-build team that removed 20 million cu yd of earth, mostly rock, and built 22 bridges and several interchanges—says his firm took a “calculated risk” in signing on to the P3 fixed-price project after looking at the challenges “through a different lens.”

ODOT transferred design, construction, finance, schedule and all geotechnical risk to the developer but “retained more risk than might normally be seen on a P3 project … to keep it on time,” says Barnitz. That included relocation of high-voltage transmission towers, tree clearing, environmental surprises and scope changes.

“All stakeholders had their own assumptions for how things would go, and we had to actively partner and really focus on clear communication to ensure different assumptions and expectations didn’t derail progress,” says Ratkovich.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

The project gained an upgraded Fitch Ratings score of A- from BBB, based on the credit rating firm's assessment of its lead firm's experience, project exposure to cost volatility and scope risk and its "sizable security package that covers the worst-case replace cost scenario."

The fixed-price approach appears to have worked on Ohio’s project and is becoming more core to more public and private projects across the U.S. and beyond, but the growing prevalence in a more competitive marketplace and on more complex megaprojects, P3 and non-P3, has led to an increasing financial squeeze for contractors that is showing up on balance sheets as negative numbers.

Fixed-price contracts, also known as lump sum, have become essential to owners moving forward in the tumultuous energy megaproject market and for public-sector entities struggling to stretch funds and quickly execute transportation and other infrastructure jobs.

Experienced contractors have historically been able to manage fixed-price projects to some level of profit or recover from a loss—but aggressive bidding to build backlog, as well as acceptance of growing levels of project risk, have taken a toll.

Observers say fixed-price fallout pervades the industry, but publicly-held industry firms that have to disclose quarterly financials have had to share increasingly bad news on fixed-price red ink.

"Contractors all tend fo fall in love with a job, since they've spent so much money chasing it. They don't want to be priced out," says one P3 contractor executive. "Talk about risk-sharing mode. There is none. A new model has to take place that's more disciplined."

Heavyweights including Fluor Corp., Skanska USA, SNC-Lavalin Inc., AECOM and Granite Construction have piled up recent losses linked to project charges and disputes based on public disclosures, with CEOs announcing dramatic changes in bidding strategies and intentions to limit P3 participation and fixed-price contracting.

"It’s a reflection of the economy being so good for so long. Contractors can walk away," says Keith Molenaar, associate engineering school research dean at the University of Colorado-Boulder. "When things are tighter they have to take more risk."

“We Can’t Keep Doing This”

Montreal giant SNC-Lavalin Inc. stunned the market with its announced plan earlier this year to withdraw from fixed-price work, with CEO Ian Edwards citing a “broken model,” as project losses mounted. The firm now has separated its construction and more stable services businesses but still must finish work on about $3 billion of fixed-price public and private-sector project backlog.

“Projects are getting larger and more complex, with a desire by governments and clients to transfer an asset’s whole risk,” Edwards told ENR in an interview. “They want someone to deliver this at the lowest cost, and the cheapest person wins. I’ve been in this all my life, and we can’t keep doing this.”

Fluor posted losses of hundreds of millions of dollars in its two most recent quarters linked to acceptance of major project risks under former CEO David Seaton. "With a focus on growth, they took their eye off a strong go-no go process," says a former executive. "Monthly risk reviews were rigorous, but attendance became more optional. Project erosion got big enough to put the whole company at risk. Where was the board?"

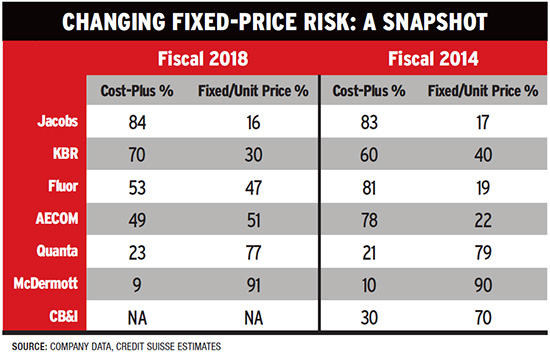

With a top management change this year that reinstated executives with more operational discipline, the firm has restricted its pursuit of fixed-price energy work, exited lump-sum government contracts and cut back where it bids on big infrastructure jobs. A September Moody’s Investors Service report says Fluor project charges grew as its backlog shifted to 49% fixed-price inf June, from 19% in 2014. See chart below

“Lump sum is not going to go away, but a balanced lump sum is going to be the model for the future; it has to be,” said new CEO Carlos Hernandez on the firm’s quarterly results call on Oct. 31. “There will be projects we will walk away from, for sure. But overall we are in a very positive position in our industry because of our ability to execute the large projects.”

Market watchers await results. In a Nov. 21 research note, Jamie Cook, a leading E& C sector analyst at Credit Suisse, pointed to good prospects for Fluor contract awards in petrochemical and LNG construction, noting "changing competitive dynamics and shrinking competition ... [that] should be a positive ... in terms of improving terms and conditions on future projects and winning new work. In fact, customers are concerned on the short list of competitors left that can do EPC work."

She added that while executives report the estimated $30-billion fixed-price LNG Canada megaproject in Kitimat, B.C., now underway with partner JGC Corp., "is on track, we believe this project will continue to be an overhang ... unless Fluor can renegotiate terms."

Fluor confirmed on Nov. 22 that Tappan Zee Constructors, the consortium it led for the fixed-price design-build of the $4-billion Tappan Zee replacement bridge across the Hudson River north of New York City, filed suit Nov. 18 against the New York state Thruway Authority in state Supreme Court. seeking documents to support a previously filed $900-million claim for additional payment.

The consortium's suit says the state violates public disclosure law by impeding its access to records needed to pursue that claim for added costs on the renamed Gov. Mario Cuomo bridge. Politico first reported the potential of that claim in 2018.

A Thruway Authority spokesman confirms the claim was partially submitted last year and revised this year. A Fluor spokeswoman declined further detail on the suit or claim.

"The project remains within its $3.98 billion budget and the claim filed by the contractor is obviously nothing more than an ineffective negotiating tactic," an authority spokeswoman said in a statement.

“E&C firms aim to avoid fixed-price projects with higher risk. But changes will not materially transfer risks to clients in the near term due to competitive market conditions.”

– Michael Corelli, Vice President, Moody’s Investors Service

Skanska and Granite Construction have also announced P3 and civil construction pullbacks after quarterly losses beginning last year.

In its recent earnings call, Tutor-Perini noted losses and market exits of peer firms, with CEO Ron Tutor touting the firm’s “reach and success” to bid and win large fixed-price infrastructure projects. But they represented 78% of backlog in June vs. 55% in late 2015, says Moody’s.

"There may be a dozen financial leads in the P3 market, but they can't do anything without a giant like us to guarantee price and guarantee schedule and deliver,” Tutor said on the firm's latest quarterly results call this month. The firm reported a quarter profit, but UBS analyst Steven Fisher raised concern in a note ”about execution risk, as [the firm] is taking on many very large projects; some have faced delays already and contract terms are not transparent to us.”

The problem-plagued rebuilding of Interstate-4 in Orlando, Fla.—a $2.3-billion P3 project on which Skanska and Granite are part of the concession team—has generated big financial headaches. Florida transportation officials have yet to agree to a request from the consortium, I-4 Mobility Partners, which includes Lane Construction, for a $100-million added payment and a time extension. The project is about 271 days behind its scheduled end of 2021 finish.

Moody’s Investors Service, in a June credit opinion, repeated a previous “negative outlook” for the consortium. It said work has accelerated but there is above-average turnover of employees, "You own it so no change orders. It's tough," says one industry management consultant. "People will be a lot more careful and get contract language that works for them."

Insiders and observers both say Denver airport’s now terminated $1.8-billion P3 contract with a Ferrovial-led team—which included an estimated $650-million terminal renovation and 30 years of concessions management —should never have been done as a fixed-price job. The two sides battled over multiple change orders, airport micromanagement, slow team responses and a dispute over weak concrete.

“With those potential problems, the project shouldn’t have gone to financial close,” says Rodney Moss, senior vice president of the Hunt Cos. and a project advisor. “This was more or less a progressive design-build project, but conditions below ground weren’t what they thought. They got mad at each other, and it became a personality issue.” With an estimated $200-million cost settlement still being negotiated and a new, airport-managed team selected, “it gave P3 a black eye,” says Moss.

Norman Anderson, CEO of infrastructure consultant CG/LA, questions P3 as a “salvation,” saying the “model is difficult, and you have very different cultures involved.”

At a recent Design-Build Institute of America conference, where attendees debated P3s, one privately-held construction firm speaker whose company has participated in P3 concessions emphasized that contractors must “have their eyes wide open about the risks.”

Other P3 proponents agree. “Owners need to pick partners carefully," says Matt Girard, civil division group head at P3 developer-concessionaire Plenary Group USA. Along with Walsh Investors LLC, it has provided financing and long-term management since 2015 for Pennsylvania’s $942-million Rapid Bridge Repair program to expedite repair of 560 deficient state bridges, bundled as a P3. Work is set to finish this year.

But some executives point to more participation in U.S. and Canadian projects of non-North American contenders with higher risk tolerance as a key factor in more recent aggressive fixed-price bid competition. Several contacted by ENR declined further comment.

But fixed-price contract issues also have been problematic in the UK, with aggressive bidding seen as a key factor in the bankruptcy of contractor Carillion, that has had major industry impacts there.

Industry respondents to a survey by U.K. construction publication Building reported widespread price discounting to secure contract awards, particularly after the June 2016 Brexit vote. Building reported on Nov. 8 that the new CEO of contractor Galliford Try, which had recent big losses on two infrastructure projects in Scotland, said the firm will do no more fixed-price work.

Loss of Discipline

Ron Oakley, a former contractor CEO and executive, says banks won’t finance P3 deals “unless someone is on the hook for overruns, and it’s the contractors that have taken them.” He points to some loss of discipline in bid/no-bid analysis that recognizes when projects are “below the water line … and could take the company down. I’m not sure if companies have gates now.”

According to Oakley, “owners want the best price and push as much risk to the contractor and supplier side, driving fixed-price without the project scope fully defined. Customers have gotten used to it and want us to take more.”

Observers see issues in owners gravitating to fixed price. “This is a big issue with public transit—it costs too much and takes too long to build, so let the private sector do it,” says Robert Puentes, CEO of the Eno Center for Transportation. “But there are problems locking in a price that probably results from lack of communication and coordination within an agency on what it wants.”

Michael Horodniceanu, former president of MTA Capital Construction in New York City and now chairman of the IDC Innovation Hub at NYU Tandon School of Engineering, says risk-sharing requires starting with "a much more coherent approach to what you want to achieve."

He points to the need for owner agencies to reduce project specifications "that are not necessary" and carefully assess midstream changes that can ratchet up costs "dramatically." Says Horodniceanu: "Once you go into change order mode, there is constant disputable environment in which everyone is trying to get where they want to go. It's like negotiating in a Middle east bazaar."

Big effects from project disputes, overruns and charges on construction-sector value and project financial strength concern investors and analysts.

“Competition among … companies led them to bid aggressively on projects, and they were then hurt by lower-than-expected labor productivity, unforeseen execution issues and unusual weather events,” says Michael Corelli, Moody’s senior credit officer, in a September report. He notes in the last two years, firms' "increased earnings volatility and weaker credit matrics," highlighting "inability to anticipate issues or include contingencies in bids as an indication of shortcomings in risk management and execution.”

Scott Zuchorski, Fitch Ratings managing director for U.S. project finance, makes it clear: “Risk allocation affects ratings.”

“At 30% complete drawings, there's a lot of risk and owners want builders to take that risk. On megaprojects, with the level of complexity, it's almost impossible to identify all the risk.”

– Paul Trombitas, FMI senior consultant

Jamie Cook, Credit Suisse managing director and lead E&C sector analyst, noted in a June report that “for investors to buy in, [firms] need to demand better contract structures to de-risk business models. This is long overdue, given limited competition in the space and … reflecting unnecessary risk consistently placed on the contractors.”

Mario Angastiniotis, Fitch Ratings’ Canada infrastructure finance director, says “margins are so thin, there’s not enough meat on the bone. It’s OK to take a loss once in awhile. But if it’s sequential, you can’t keep bidding like that.”

Says Andrew Wittmann, lead E&C sector analyst for Baird Equities: “It’s hard to know what is the contractor’s fault vs. the marketplace. There’s a fair debate around that.”

No Silver Bullet of Procurement

Market participants agree that fixed-price P3s are “not a silver bullet of procurement,” says Lee Clayton, Toronto-based vice president of contractor PCL. “There is a higher chance of success with greater standardization of P3s, but we still see clients reinvent the wheel and start from square one.” He says since “contractors are inherently optimistic, they will bid on a project and hope risk problems never happen. For contractors who have left the space, the risks came home to roost.”

Design issues often become a construction risk. "At 30% complete drawings, there's a lot of risk and owners want builders to take that risk. On megaprojects, with the level of complexity, it's almost impossible to identify all the risk," says Paul Trombitas, FMI senior consultant and P3 specialist.

Stephen Mulva, Construction Industry Institute executive director, contends that “the glamour of the benefits outweighed the reality for years. Contracts were written faster than insurance products could keep up.”

Surety bond firms say they have beefed up P3 project oversight, even as some states have relaxed requirements, with a recent WSP analysis noting the default on Indiana's I-69 P3 project of Madrid-based Grupo Isolux Coran, which had bid 30% below its closest competitor. The state had to take over the $325-million project after four contractor delays, paying millions more in added costs.

Michael J. Garvin, associate construction professor at Virginia Tech, who also advises P3 advocacy group AIAI, says “when P3s started to come out, there was a tendency to think the market was going to develop, so contractors decided to be aggressive in pursuing earlier projects.” But project flow has not been strong enough to sustain the experience curve, he says

Meanwhile, owners in some sectors will likely remain locked into fixed-price awards to gain customer commitment and an advantage over rivals.

Reuters reported in June that LNG developers are seeking approval for nearly $200 billion in global projects in the next two years to meet anticipated demand, racing particularly to lock in contractor lump-sum awards.

Some analysts highlight that KBR, while nearly transformed into a low-risk government services firm, is still negotiating fixed-price EPC construction contracts for LNG projects—including the $10-billion Goldboro project in Nova Scotia for Pleridae Energy.

“We have been curious why KBR would take on the risk of lump-sum LNG work, given its message about de-risking and prioritizing consistent performance,” said UBS analyst Steven Fisher recently.

Inability to strike a fixed-price construction arrangement, however, caused at least one large-project cancellation. Backers of a $1.5-billion urea and methanol complex in Becancour, Quebec, pulled the plug on the project this month after years of development because they could not reach a firm EPC contract deal.

The project’s competitive bidding process “will not have resulted in a viable option,” said a spokesman for the developer group.

Making Adjustments

Some owners are adjusting their risk focus. Fluor’s Hernandez said on the Oct. 31 call that for its recently-won Rovuma LNG project in Mozambique, an estimated $30-billion project to be built with JGC and Technip, clients are responding to its call to de-risk the job. He described high-level conversations about what’s happened “with allocation of risk having been disproportionately shifted to the contractor.” While not offering details, Hernandez noted risks “that are remaining with the owner.”

SNC-Lavalin’s Edwards also noted its push to complete remaining fixed-price work in its backlog, including the $4.8-billion Montreal REM light rail, which it leads for the project overseer, a Canadian pension fund that also is a firm investor.

Observers have questioned if the project, with major tunneling challenges, will stay on cost and schedule track. “REM is an incredibly complex project with 60 km of urban railway, but the key is a close relationship with the client,” Edwards says. “We have it in a good place.”

He also notes a more collaborative “alliance contracting” risk-sharing bid approach begun in Ontario to rebuild Toronto’s Union Station.

Companies are not pursuing bids “unless owners understand the risk and keep some in house,” says FMI's Trombitas. He says Washington state’s DOT and Seattle-based Sound Transit share best practices, and other owners are creating their own training. DBIA also is developing programs to build owner expertise in understanding risk allocation on fixed-price contracts.

After two of three bidders pulled out of the $3.9-billion Edmonton, Alberta, LRT project last month, “the government has returned to the table to change terms and restarted the process,” says Fitch Ratings’ Angastiniotis.

“ We have .... a consistent approach to our private sector partners. They're taking on a large amount of risk with P3s and want to work with a partner who will carry through.”

– Rob Carey, Virginia DOT deputy commissioner

Virginia, a pioneer in private transportation finance for nearly a quarter-century, has a key focus on risk management.

"Virginia has an AAA bond rating, which allows us to price out a project as if we were going to do it ourselves. This sets the baseline for us to determine whether it makes sense to do it as a P3, or as a state-funded project," says Rob Carey, Virginia Dept. of Transportation deputy commissioner. ““We have … a consistent approach to the private sector partners we do business with. They’re taking on a large amount of risk with P3s and want to work with a partner who will carry through.” Adds Thomas A. Sherman, deputy director of VDOT’s Office of Public-Private Partnerships: “Risk has to be understood and accepted by both sides to find the sweet spot.”

But in the U.S. "insurance products and rating agencies are still in their infancy when it comes to P3s," says CII's Mulva. "They could use a little more work to have a better picture of the risks."

Also according to a transportation P3 policy researcher in Virginia, contractors and owners "need to know what are each other’s deal-breakers. Owners may want to tweak the structure of a P3 to make it more attractive to contactors so that they’ll get bidders."

Resource Challenges, New Tools

Experts point to project management staffing shortfalls, particularly at top levels, as a key project delivery challenge. “It all comes down to people—you need managers who understand what risks to assess,” says FMI’s Trombitas.

And experts see a key role for new methods. Olfa Hamdi, an advanced work packaging consultant, says AWP can “close the gap between the practical execution of capital projects and contractual risks.”

Chris Bell, vice president of project management software firm e-Builder, a unit of Trimble, adds that fixed-price contracts often result in contractors “taking a more independent posture ... as they own much of the risk, so joint technology decisions are unintentionally lost ... which unintentionally lowers collaboration when it is needed the most" on higher risk projects.

He adds that in the past, technology integration "was all about system to system in the same organization" of a contractor or owner. "Now, modern integration is between similar systems but also between different organizations. This is what creates a common platform that improves project performance."

According to Bell, that is the case for a large P3 project for a major northeast airport he declines to identify. "The consortium on this invested the time to select a technology platform for project management that allowed all parties to collaborate," he says. "Much of the focus upfront was to define the way that the teams would work (owner, contractor and design firm) and share data. They chose a platform that allows other parties to bring their own system but exchange data when necessary," something he sees as a "risk mitigation strategy for organizational barriers."

P3 boosters emphasize that the delivery method is not losing market to more risk-averse contractors.

“Risk challenges are not the only factors affecting contractor decision-making,” says Lisa Buglione, AIAI executive director, noting “logistical issues” such as skilled worker supply and material or equipment price hikes. “Generally there is far more to the business decision than just an aversion to a single procurement model,” she says.