The Top 225 International Design Firms

Oil Prices Spur Engineering and Architecture Market Downturn

Design work in the global energy sector sagged and brought an economic slowdown

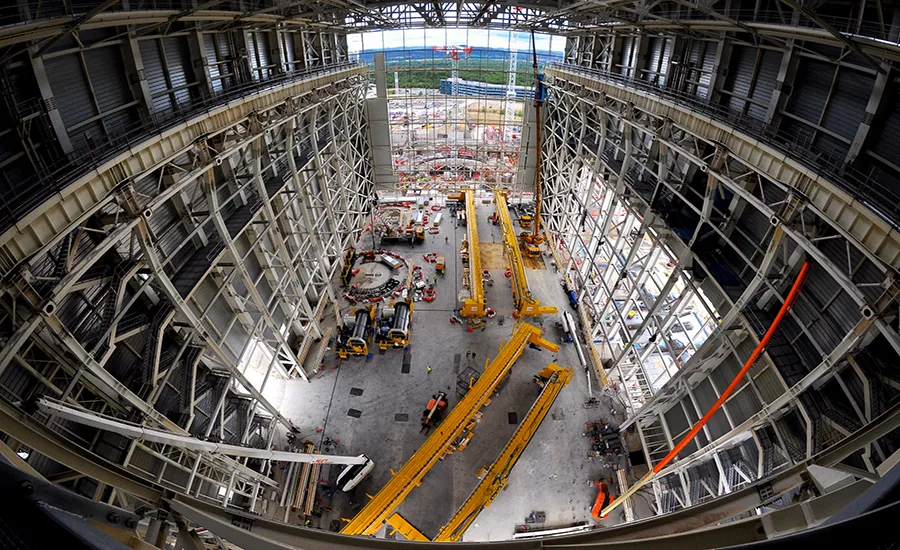

Atkins is the architectengineer, partnering with Assystem, Egis and Empresarios Argrupados, on the world’s largest experimental fusion reactor, in France.

PHOTO COURTESY OF ITER IO

The global market for professional design services is showing signs of softening as energy prices continue to be low. Weakened demand for petroleum and metals has had an impact not just on those markets for engineering and architecture but also on public and private spending in other sectors, particularly in resource-rich countries that depend on cash generated by exports to fund expanding infrastructure.

|

View the Complete Top 225 International Design Firms PDF (Subscription Required) View the 2016 Top 225 International Design Firms Chart |

The uncertainty in the market can be seen in the results of ENR’s Top 225 International Design Firms survey. The Top 225 firms generated $65.43 billion in design revenue in 2015 from projects outside their home countries, down 7.7%, from $70.85 billion, in 2014. They also had $70.76 billion in revenue from domestic projects in 2015, down 3.7%, from $73.48 billion, in 2014.

On the Top 225 International Design Firms list, firms are ranked based on design revenue from projects outside of their home countries, measuring their presence in international commerce. The ENR Top 150 Global Design Firms list measures total worldwide design revenue, regardless of the project location.

The petroleum market, the largest market for the Top 225, was the biggest loser, with international revenue dropping 20.2%, to $17.74 billion, down from $22.23 billion in 2014. Part of this falloff can be attributed to the absence from the list of France’s Technip, which reported $1.43 billion in petroleum design-revenue on last year’s list. Even discounting Technip’s presence on last year’s list, the petroleum market still fell 14.7%.

On a regional basis, the two largest markets for the Top 225 saw significant drop-offs in 2015, with Asia falling 16.0% and Europe down 11.9%. And, once again, low oil prices hurt the Canadian market, which dropped 14.2% in 2015, after falling 15.0% in 2014. Despite lower oil prices, the Middle East market rose 6.0%, while the U.S. market was up 1.8%.

Article Index:

Oil Pressure

The drop in oil prices and the general global economic slowdown have taken their toll on the petroleum market. “The oil-and-gas business has definitely been hit … we had a lot of stuff canceled in the Middle East and the U.S.,” says Keith Howells, chairman of U.K.-based Mott MacDonald Group.

Many global design firms in that market are seeing projects canceled or delayed, says Kim Wee-chul, CEO of Korea’s Hyundai Engineering Co. Ltd. He says the downturn has led to fierce competition among engineer-procure-construction firms in the sector, particularly in the Middle East, which increasingly is moving to a low-bid contracting mode.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

However, Kim says Hyundai Engineering is finding opportunities in Russia and the Commonwealth of Independent States, “where there is high demand for adopting international technologies.” Hyundai Engineering is working on the $3-billion Kandym Fields Gas Development Project in Uzbekistan and the $3-billion Kiyanly Ethane Cracker in Turkmenistan, he notes.

Kim also says the lifting of international sanctions against Iran has created a new, large market for petroleum EPC firms. “Iran has been increasing the oil production and is expected to continue the expansion” of its oil business until the country’s faltering economy recovers, Kim says.

On the power side, there is an increasing market for renewable energy. “Even Saudi Arabia, the world’s leading producer of fossil fuels, has recently launched a 100-MW tender to build new renewable-power projects,” says Umberto Sgambati, CEO of Italy’s Proger.

Sgambati says this Saudi tender highlights just how fast the scenario is changing. “We are witnessing the start of a new period for engineering that is leading to a significant change in the energy mix … with a partial transfer of investments from the oil-and-gas sector to renewable-energy sources.” The move to renewables is a major change of focus for the power industry, he says.

Social conditions are leading to an increase in interest in the infrastructure markets. “In a low-interest-rate environment, governments are borrowing to spend on public infrastructure,” says Neil Bruce, CEO of Canada’s SNC-Lavalin. Several factors are fueling this trend, including a growing demand for public infrastructure and an increase in urbanization, he notes.

Many firms see the global trend toward urbanization spurring infrastructure demand. For example, Hisham Mahmoud, CEO of Canada’s Golder Associates, says such projects are getting larger and more complex, adding, “There is also more demand for brownfield redevelopment projects.”

Mahmoud says there is a significant difference between developing and developed markets. “In developing markets, there is a significant demand for new infrastructure,” he says. “In developed markets, there is a demand for rehabilitation of existing infrastructure and a continued trend toward privatization of public infrastructure.”

Bruce says public-private partnerships are helping countries answer the need for infrastructure. “SNC-Lavalin Capital Inc. investment group provides a unique opportunity for the business to take a stake in infrastructure that is commonly provided by government-owned entities,” he says. “This places the designer in the heart of the developer organization and creates interesting new challenges for our people.”

European Uncertainty

The European market has been somewhat unsettled, but many large design firms have been doing well. For example, Sweden’s SWECO AB has grown by about 15% a year for the past 15 years. “We intend to keep growing,” says Tomas Carlsson, president and CEO. But SWECO will not enter emerging markets because of their low fees.

Another European firm doing well is U.K.-based W.S. Atkins plc. With sales up 6%, to $2.4 billion, last year, Atkins has achieved an 8% profit margin, which is “exactly the goal we set ourselves five years ago,” says CEO Uwe Krueger.

COWI A/S, Denmark, has been doing well, too. Lars-Peter Søbye, COWI’s CEO, also reports margin improvement. He notes that, generally, “the past 12 months have really been picking up. We have a much stronger order book and backlog.” Business in bridges, tunnels and marine is “really taking off,” he adds.

However, some firms are disappointed in the market. Facing a weakening order book, Mott MacDonald’s sales grew 7% to 8% below the firm’s 10% target, says Howells. Netherlands-based Arcadis NV has passed through “a mixed year,” with bad news from Brazil and difficult conditions in the U.S., says CEO Neil McArthur. But the firm has had good growth in Europe, Australia and Southeast Asia, he reports.

While COWI foresees a 10% to 15% demand drop in Denmark over the next two years, the buoyant Swedish market is “getting even stronger,” says Søbye. Norway is boosting infrastructure spending to counter the fall in oil activity and is “really picking up.”

Sweden, “the strongest economy in Europe,” is good for SWECO, adds Carlsson. Business in Belgium, Germany, Norway and Denmark is also good, while the Netherlands and Finland are “challenging.” Further, since acquiring the Netherlands-based Grontmij NV last October, synergies in the first quarter of this year reduced costs by about $4.5 million of the forecast $30 million annual savings, adds Carlsson.

Design firms are pondering how the U.K.’s late June referendum to quit the European Union will affect them. “The consequences … remain unclear,” notes Howells, but “a lot of infrastructure projects seem to have momentum.”

Many firms worry the vote will hurt markets. “Brexit has brought a new level of uncertainty to our business and particularly to our biggest markets in the U.K. and in Ireland,” says Liam Foley, group director of business development at Ireland’s PM Group.

Brexit already has produced financial fallout, Foley says. “Currency exchange rates will have the most immediate impact following the drop in value in [the British pound] following the decision. It is too early to anticipate long-term effects, but the uncertainty over the next two to three years is likely to adversely impact investment decision-making,” he observes.

Most firms see continued opportunities in the U.K. “We will obviously see a period of uncertainty. Our commitment to serve our U.K. customers will remain the same,” says Carlsson. “There will be a period of uncertainty now for clients in deciding whether to go ahead with investments in the U.K.,” adds McArthur.

The Wild West

For international designers, North America remains the largest market. Two recent big contract wins in the U.S. underpin “the growth [Atkins] can expect … in the coming years,” says Krueger. However, bidding costs have eroded margins, to 5.6% from 5.9%, he says.

Mott is “growing quite well” in the U.S., says Howells. The firm has ended its long-standing North American joint venture with Canada’s Hatch Ltd. “We ended up with 75% of the business,” he notes. Mott still has about 55 staff in Canada. “We intend to build from that,” Howells says.

Arcadis’ U.S. business is going through a difficult period: As the demand from the mining and oil-and-gas sectors has dipped, the firm has been restructuring its environmental business, says McArthur. Arcadis is focusing on simpler remediation work, rather than large, complex projects.

For PM Group, the U.S. is a major market opportunity. “Drug approvals by the [U.S. Food and Drug Administration] are a continuing trend since 2014 and a big driver of new business in our core sector: pharmaceuticals,” Foley says. These product lines require new or expanded production facilities.

In Latin America, “deep recession [and] political turmoil” have driven down Brazil’s contribution to Arcadis’ sales by 50% in 15 months, according to McArthur. However, Brazil’s pent-up demand for basic infrastructure remains huge, he adds. And having “right-sized” its market, business in Chile “is doing well,” though mining-related work has fallen, he says.

New Potential in Asia

Free trade has spurred increased interest in the Asian market. “The openness across Asia to increasing levels of foreign direct investment in infrastructure is creating opportunities in the region,” says Greg Lowe, group chief executive of New Zealand’s Beca Group Ltd. An anti-corruption push in many Asian countries is providing investors a greater level of comfort, he says. Lowe says free trade is increasingly driving economic growth in Asia. “While anti-free-trade policies appear to be gaining traction in the developed world, countries such as Indonesia, Thailand and India are welcoming foreign developers and investment.”

A growing middle class in many developing countries in Asia also is driving the market for consumer products plants. “In all of our core sectors, especially life sciences, food, med tech and mission-critical data centers, the fundamentals for growth are strong—a growing population, urbanization, exploding middle class in Asia,” says PM Group’s Foley.

The Asian infrastructure market continues to be a major growth area for international design firms.

“Urbanization in the ASEAN region is growing at the fastest pace in the world, and emerging Asia is expected to account for almost half of global infrastructure investment going forward,” says Lowe. The region’s infrastructure needs are huge and indicative of a long-term, West-to-East geographic shift in infrastructure spending, he says.

In Southeast Asia, Hong Kong is “still a strong market in our home base,” says Krueger. “On the basis of a very strong operation in Hong Kong, we diversified the business even more, with project wins in Singapore, Malaysia and Vietnam,” he adds.

Across the region, “we are looking for the big opportunities in tunnels, bridges and marine,” says Søbye. The firm is reinforcing its presence in Singapore’s tunnel market. After a lull, Singapore now offers “a very strong list of projects,” adds Howells. With rail work, emerging Indonesia is improving, while Thailand remains “a tough market,” he says. In China, Mott focuses on direct foreign investment. “That seems to be holding up, despite all the troubles,” adds Howells.

Another large market is Indonesia. “Indonesia has one of the fastest growth rates in the region,” says Lowe. It has become an increasingly important market, he says, adding, “Within Indonesia, we see particularly good opportunities in mining, food and beverage, and the active building sector.”

Atkins’ Krueger welcomes China’s current anti-corruption drive, even as it has led to a slowdown in work. But he believes the market has stabilized. McArthur also sees signs of stability, though the market “clearly slowed down” last year.

India is a promising market that has been slow to yield results for many design firms. “India is picking up a bit, though ambitious plans have yet to materialize,” says Howells.

On the other hand, SMEC has been finding work in India. “SMEC has a solid reputation in India for delivering important infrastructure design projects, including the Rohtang Highway Tunnel and Karnataka State Highways Improvement Project,” says Andy Goodwin, SMEC CEO. Further, the company in June 2016 launched its first off-shore design center, in India. “Operated by global engineering outsourcing consultancy Cyient, SMEC’s new design center will support SMEC’s global design work primarily around civil and structural,” Godwin says.

Middle East Holding Its Own

SNC-Lavalin’s position within the international design market has become increasingly resilient, thanks mostly to work in the Middle East, says Bruce. “The Gulf Co-operation Council [GCC] region and our home market in Canada are currently leading to a record backlog in 2016 of $13.4 billion, with a stream of project awards over the past year. In the GCC alone, SNC-Lavalin’s presence has grown significantly, to 8,000 people,” says Bruce.

SNC’s 2014 acquisition of Ireland’s Kentz Engineers and Constructors, an oil-and-gas engineering and construction business, has helped to propel the business in the region, says Bruce. He says SNC now has capabilities ranging from front-end engineering and design to detailed engineering and construction to commissioning, maintenance and operations.

In the Gulf region, “Dubai is OK, but the oil-price fall has hit Abu Dhabi,” says Howells, adding business in Qatar is “quite uncertain.” Rail and metro works in the region “are booming,” adds Krueger, who reports a “record year” in the region.

Dubai is insulated from the oil slump as petroleum represents only 5% of its GDP, notes Ammar Al Assam, CEO at Dewan Architects + Engineers, Abu Dhabi.

“Dubai has an aggressive government investment policy in infrastructure and tourism and is preparing for Expo 2020 and this is further driving the growth,” he adds.

Al Assam says there has been a drop in government projects in Saudi Arabia. However, he says private investments are continuing to get the green light as developers are looking for the cheaper construction opportunities from firms desperate for work “as a result of the competitive market conditions.”

Proger has shifted its focus to Africa and the Middle East, particularly Saudi Arabia, says Sgambati. It is providing consultancy, design-review and project-management services and construction supervision on security compounds under the KAP 3 and KAP 4 program throughout Saudi Arabia.

Iraq has been a troubled market. “The ongoing war with ISIS, oil-price slump, and acute mismanagement and corruption have affected [Iraq’s] growth tremendously. Projects are almost non-existent, and collection of receivables is a great concern,” says Al Assam.

Despite political difficulties, Turkey “is picking up” through foreign financed infrastructure, says Søbye. Howells finds “there are not as many projects coming through as there were, but there are still grand ambitions.” Mott continues to pick up P3 advisory work.

In Africa, Arcadis works mainly for multinationals, says McArthur. South African demand is “in a poor state,” adds Howells. Atkins targets work with Chinese contractors—“that’s where the action is,” says Krueger. Atkins is using its acquisition this year of Howard Humphreys to expand in East Africa.

Many designers are relying on a hefty backlog to get through any downturn. For example, Dewan Architects + Engineers is growing in Africa, with projects in the Congo and Egypt. However, Al Assam says the firm will develop that market slowly. “Our order backlog has never been greater, and this gives us a good two-year cushion as we continue to develop new markets and grow our business in our existing markets.”