Contracts, Caution On The Rise for Southeast Builders

More sectors are showing increased activity, but economics is beginning to dampen prospects for residential projects

Health care contracts, such as JE Dunn’s Morton Plant Hospital project in Clearwater, Fla., helped boost revenue in 2015.

PHOTO COURTESY OF JE DUNN CONSTRUCTION

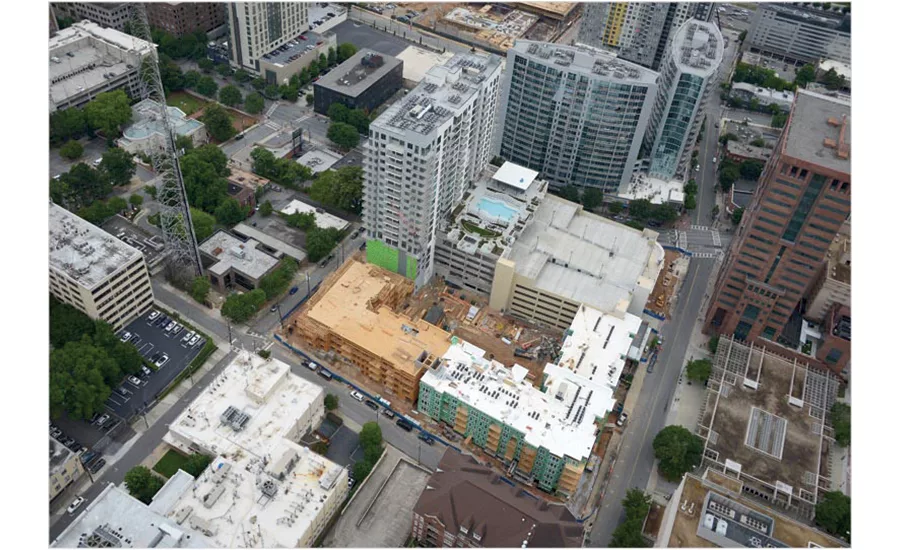

Multifamily residential construction, like Balfour Beatty Construction’s Alta Midtown project in Atlanta, is beginning to slow, say builders.

PHOTO COURTESY OF BALFOUR BEATTY CONSTRUCTION

DPR Construction is wrapping up construction of the U.S. Tennis Association’s National Campus in the Orlando area.

PHOTO COURTESY DPR CONSTRUCTION

Health care construction is strong across the Southeast. Pictured here is Brasfield & Gorrie’s Mission Health Surgical Tower, now under construction in Asheville, N.C.

PHOTO COURTESY BRASFIELD & GORRIE

Southeast contractors are poised to remain busy as contracting activity continues at an accelerated pace. At the same time, some sectors that have driven much of the Southeast construction market’s growth over the last few years, such as multifamily residential, are beginning to slow markedly, thereby raising a note of caution for builders.

“What’s slowing down some of the deals is the price pressures,” says Dan Kaufman, regional president for JE Dunn Construction, Atlanta. While economics is beginning to impact certain projects, some contractors are growing nervous as they also wonder about potential election-year impacts and historical boom-and-bust cycles. Still, a broadening swath of projects keeps moving forward. Lenders may nix a project one week, says Kaufman, “but then you go to the marketing department and they’ve got four opportunities this week that total $200 million. It still feels pretty good, it’s just that I feel a little bit of caution in the marketplace.”

Based on data submitted to ENR Southeast’s Top Contractors survey, construction activity in the four-state region of Florida, Georgia and the Carolinas increased during 2015, with the overall rate of growth accelerating from the previous year. For instance, the more than 100 respondents to this year’s survey collectively reported $23.45 billion in 2015 revenue, a nearly 11.7% increase from the $21 billion that survey participants posted the previous year.

|

Click Here to View the Southeast Top Contractors Ranking 2016 |

That 11.7% growth for 2015 is more than double the percentage gain of 5.6% that the Top Contractor survey respondents reported during 2014.

Looking into the numbers, activity in the Florida market and the multifamily residential market appeared to account for much of the Southeast region’s growth. Survey respondents reported a collective $10.98 billion in Florida revenue for 2015, a gain of roughly $1.6 billion, or 18%, over the previous year. Likewise, contractors reported roughly $3.6 billion in 2015 revenue from multifamily residential projects, which equated to a 33% gain over the previous year’s survey total of $2.7 billion.

This year’s top 10 ranked firms also contributed to the overall gain, with that group reporting a collective $1.2-billion improvement–or an 11.2% gain—as they earned roughly $9.1 billion in 2015 Southeast revenue.

Despite Some Declines, an Increase Expected

As strong as 2015 proved to be, the overall Southeast market for construction services may be even better this year, despite the flagging residential market, says Al Petrangeli, president for Balfour Beatty Construction’s Georgia division.

“Multifamily is clearly slowing down from the incredible pace it’s had,” he says. “We’re starting to see some tightening of lending, and deals are harder to do.”

“We’ve seen the top of the multifamily market,” agrees Kaufman, with JE Dunn. “If not this year, early into ’17 we’ll see half the (number of) projects.”

Despite the slowing residential sector, Petrangeli believes the overall activity level in the Southeast is higher in 2016 “because there’s diversity coming into the platform of jobs,” with the revival of the long-lagging office sector a noticeable change.

“The office market is starting to heat up, even outside of the build-to-suits,” Petrangeli says, noting numerous corporate relocations in the Atlanta area and ongoing projects in Charlotte as examples of this improving market sector. “We’re starting to see more life in that market.”

Across the Southeast, JE Dunn’s Kaufman sees “significant activity” in the health care, higher education, hospitality and manufacturing sectors. “In a number of markets there is a lot of opportunity,” he says, adding that “health care is going to either stay like it is or get stronger.” The contractor is currently building a $90-million addition for Morton Plant Hospital in Clearwater, Fla.

Infrastructure work is showing a similar changing dynamic, says David Casey, president of Archer Western’s heavy civil division, Atlanta.

The contracting opportunities from the aviation and rail sectors were what set the 2015 transportation market apart from this year, Casey says. But agencies’ increasing use of various forms of design-build delivery is boosting this year’s potential volume of contract awards.

“This year we are seeing opportunities in all four (Southeast) states for design-build infrastructure work, with the work split moving back to a more traditional road and bridge lead work split, though transit and aviation work is still coming to market,” Casey told ENR Southeast via email.

While the design-build market for infrastructure work is expanding, “for the first time in a few years we are seeing some challenging bid-build work make it to the market,” he says.

But it’s not all positive, with Casey noting: “The volume of smaller bid-build projects is still not plentiful enough for the industry to be healthy.”

Despite that, “all four Southeast state DOTs appear to have as good a program as has been available over the last few years,” he says.

The increasingly active market for projects hasn’t lessened the competition to win contracts—a factor that JE Dunn’s Kaufman speculates could be the result of contractors’ increasing nervousness about what the near future holds.

“You’ll still see the same competitors for the $80-million medical office building,” he says. Moreover, “the fees will be pretty similar to what they’ve been for the past three years, which is still too tight. That may be concern about the future, interest rates increasing and a crazy election year with a lot of uncertainty. People are still pricing things lower than they probably should if you were just looking at the opportunities that are there.”

Continuing Workforce Pressures

The well-documented search for sufficient workers continues in this robust market and is impacting project economics. Specialty contractors continue to need to figure out which contracts they can compete for based on workforce availability, which can limit selection for general contractors.

“There’s available people, but are they the ones you really want doing the craft on your job?” asks Kaufman. “You can feel the pressure. You can feel it as a general contractor in the pricing.”

The Ranking

ENR Southeast’s Top Contractors survey ranks firms based upon their 2015 revenue from the states of Florida, Georgia, North Carolina and South Carolina. In addition to revenue, the main ranking includes other information about each firm, such as top markets and largest recent contracts across the region. Breakout lists rank firms based upon state and specialty market sector revenue.