New Survey: Worldwide Construction Market to Grow 4% Annually to 2030

Under steady conditions, global construction output is set to grow, on average, by nearly 4% annually for the next 15 years—reaching, in constant 2014 dollars, $17.5 trillion by 2030, says a new global forecast. Construction’s share of the worldwide economy will rise 2.3% to nearly 15%—fueled by an 85% rise in global spending, with nearly half that growth to occur in China, India and the U.S., it adds.

Those market assessments are the crux of the 452-page “Global Construction 2030” forecast (GC30), released in London on Nov. 10. While the long view seems rosy, the survey authors emphasize that near-term prospects are at the mercy of inevitable central-bank lending-rate hikes from today’s historically low levels.

The three key growth nations the report cites—along with Canada, Indonesia, Mexico, Nigeria and the U.K.—account for 70% of expected growth, say research firms Global Construction Perspectives and Oxford Economics, authors of the GC30 survey, which is the fourth in a series. More than one-third of the $210 trillion predicted in cumulative construction volume will be, by 2030, in emerging Asian economies (ENR 9/21 p. 6).

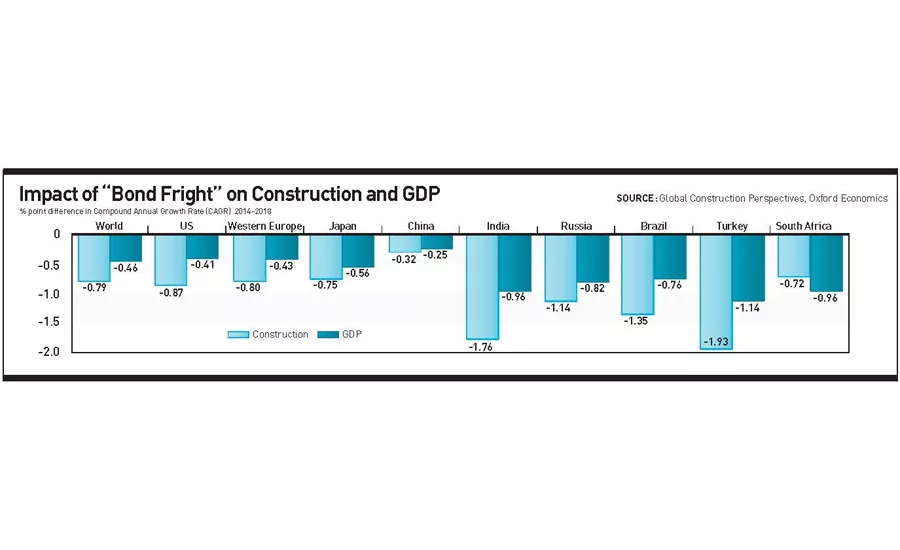

But the report also warns that an initial impetus for the growth could stall by nearly 1% a year in the medium term if the thrust of inflation leads to a hike in the U.S. Federal Reserve’s base rate—a scenario it refers to as “bond fright” (see chart, below). Two years ago, a jump in U.S. long-term bond yields, caused by the “mere mention of tightening of monetary policy” by then-Fed Chairman Ben Bernanke, resulted in significant capital flows from emerging markets to the developed world, the authors say. These hikes forced defensive interest-rate rises in India, Brazil, Turkey, Russia and elsewhere.

While rising borrowing costs tend to depress general economic output, the impact would be “considerably more pronounced on construction” because the sector relies heavily on debt, the forecasters say. In the U.K., 60% of contracting activity is debt-funded, compared to 40% for the rest of the economy, according to report’s data. The effect of rising interest rates on Indian construction output would be twice the impact on the country’s GDP.

Increasing oil prices represent a potential double whammy, possibly triggering a Fed rate rise and boosting construction costs. But a price hike would benefit oil-based economies such as Russia’s, in which construction activity was already on a slide. Its long-term economic prospects “are among the weakest in the emerging world,” says GC30, but construction likely would rebound with rising oil prices.

Even oil-rich Middle Eastern markets are flagging in the face of low oil prices. Cuts in infrastructure spending now are on the agenda in Saudi Arabia, where the fiscal deficit is forecast at 17.3% of GDP this year, says the report. Even so, it will remain the Middle East’s largest market. Qatar, with its huge gas reserves and preparations for the 2022 World Cup, is set to remain the world’s fastest-growing construction market to 2020, but output then will fall sharply, says GC30.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

Construction growth across the Middle East-North Africa region is set at half of the past decade’s levels, the forecasters predict, although they estimate $11.5 trillion in regional spending in the next 15 years. The sub-Saharan market is forecast to grow 120% by 2030, driven substantially by urbanization. Nigeria, set for a 160% rise in construction spending, is on course to become the world’s fifth most populous nation by 2030.

Among developed countries, Australia is suffering most from reduced oil and commodities prices, says the report. Its weakened currency will support some aspects of construction, but the survey authors do not expect infrastructure spending to regain its 2012 peak until 2030.

U.S. Market Growth To Exceed China

|

| Graham Robinson, executive director of Global Construction Perspectives |

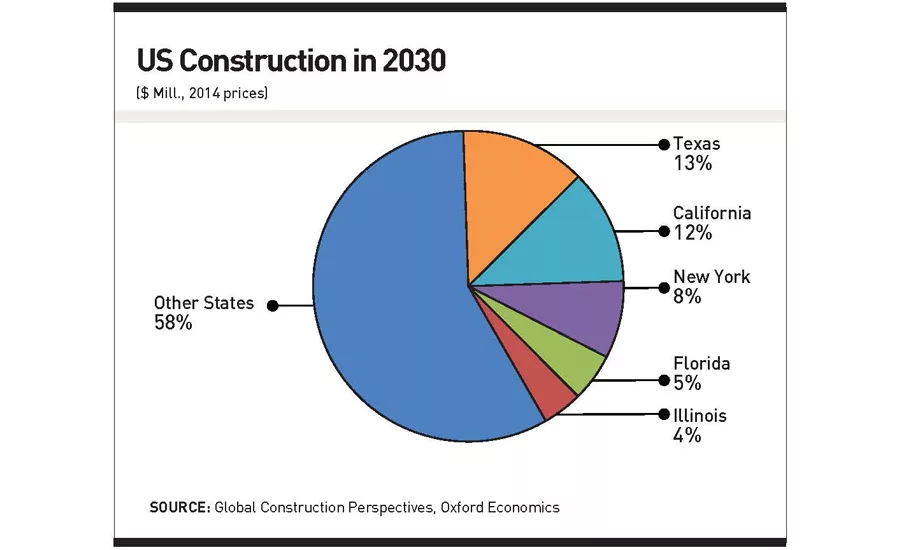

But the reports authors are more optimistic about the U.S., ranking it as “the fastest-growing developed-country market,” says Graham Robinson, executive director of Global Construction Perspectives. After shrinking by one-third between 2005 and 2010, it began to recover in 2012 and is set to exceed 5% a year to 2018, before easing off again. Investment in building construction will exceed infrastructure spending, he points out. Southern states will support faster construction growth rates than the U.S. as a whole, while the New York area will be the fastest-growing region, says GC30. One-fifth of all U.S. construction spending—about $500 billion by 2030—will be in the New York City, Houston, Los Angeles and Chicago metro areas.

Globally, U.S. construction expansion over the next 15 years will exceed that of China, which is experiencing a relative slump, with just 2.2% growth forecast for 2016. Chinese construction growth to 2020 is forecast at under one-third of the previous decade’s annual average. In the 10 years to 2030, forecasted growth is about 5%, leaving China with nearly a quarter of global construction output at the end of the period. Chinese infrastructure growth is forecast at 4% a year—faster than housing but slower than non-residential construction.

To take up construction capacity, China is set to boost its global activity, notes GC30. This activity includes bidding for work in new markets, such as the U.K., and creating opportunity with big foreign investments, including the grandiose maritime-and-highway Silk route through Asia, Africa and Europe. That route could involve some 900 projects, for which China Development Bank reportedly has promised $890 billion, says GC30.

Enhancing prospects for foreign firms in China is a resurgence in public-private partnerships. Restrictions in local government borrowing, triggered by the sector’s ballooning debt, has led to renewed interest in P3s in the past 12 months, say lawyers from London–based Pinsent Masons in the GC30 report. New standard contract forms and other rule changes could boost P3s—an approach adopted in China 30 years ago but moving sluggishly, the attorneys add. The government late last year announced 30 projects in the energy, transportation, water and environmental-protection sectors, valued at $29.3 billion total.

India is powering ahead at twice China’s rate to 2020 and is set to become the third-largest market soon after, predicted at $1.5 trillion in 2030. Indonesia is forecast to overtake Japan, to rank fourth; GC30 groups it with Vietnam and Myanmar as the new “ASEAN Tigers,” whose annual construction markets are set to grow more than 6% to 2030, when they will total more than $1 trillion. In Latin America, Mexico will overtake Brazil, which faces a “lost decade” due to stagnant construction demand. Colombia’s market is forecast to grow 2.5 times faster than Brazil’s.

With its aging population, Europe is not expected to see its construction market returning to pre-crisis levels until 2025—with annual growth averaging 1.6% to 2030, says GC30, although figures do not reflect the impacts of the recent migrant influx, particularly in Germany. It is set to have the continent’s largest market but one growing more slowly than Japan’s. By the forecast period’s end, Germany is set to be the eighth-largest global market, down from fifth. Overtaking it is the U.K., which is forecast to become the world’s sixth-largest market by 2030, pushing Canada to seventh place by around 2025.