Methodology

Inflation measured by ENR's two cost indexes traditionally moves in tandem, separated by perhaps half a percentage point. On occasion, however, the trends shown by the Construction Cost Index (CCI) and the Building Cost Index (BCI) can diverge, showing very different escalation rates. That was the case for most of last year. At their greatest degree of separation, during July of last year, the CCI showed an annual inflation rate of 3.1% and the BCI only 0.7%. By March 2003, the indexes had come back in line, with annual inflation measured by the CCI at 1.9% and the BCI at 1.5%. The mechanics of what drives ENR's indexes are explained below.

ENR began systematically reporting materials prices and wages in 1909, but it did not establish the CCI until 1921. The index was designed as a general purpose tool to chart basic cost trends. It remains today as a weighted aggregate index of the prices of constant quantities of structural steel, portland cement, lumber and common labor. This hypothetical package of construction goods was valued at $100 using 1913 prices.

The original use of common labor as a component of the CCI was intended to reflect wage rate activity for all construction workers. In the 1930s, however, wage and fringe benefit rates climbed much faster in percentage terms for common laborers than for skilled tradesmen. In response to this trend, ENR introduced its BCI in 1938 to weigh the impact of skilled labor trades on construction costs.

The BCI labor component is the average union wage rate, plus fringes, for carpenters, bricklayers and structural ironworkers. The materials component is the same as that used in the CCI. The BCI also represents a hypothetical package of these construction items valued at $100 in 1913.

Both indexes are designed to indicate basic underlying trends of construction costs in the U.S. Therefore, components are based on construction materials less influenced by local conditions. ENR chose steel, lumber and cement because they have a stable relation to the nation's economy and price structure. The selected materials also govern price trends because of their predominant use in construction.

|

As a practical matter, ENR selected these materials because reliable price quotations are available promptly for all three, ensuring that the index can be computed swiftly and on a timely basis. While there might be some weaknesses in any index based on a limited number of components, ENR feels that a larger number of elements would increase the time lag between verifying prices and releasing the computed index. Also, an index made up of fewer elements or components is more sensitive to price changes than one made up of many.

On the downside, the use of just a few cost components makes indexes for individual cities more vulnerable to source changes and misquoted prices. These aberrations tend to average out for the 20-city indexes.

|

Since the indexes are computed with real prices, the proportion a given component has in the index will vary with its relative escalation rate. In the late 1970s, labor's share of the index dropped because materias prices were in the grip of hyperinflation triggered by an energy crisis and construction boom that caused severe shortages. For example, in 1979 lumber prices increased 16%, cement 13% and steel 11%. But common and skilled labor rose 8%. This resulted in materials gaining a larger percent of the index total. The opposite occurred in 1969 when labor costs increased 14% while materials eked out a 1.7% increase.

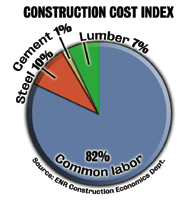

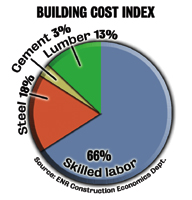

In the original CCI, the components were weighted at 38% for labor, 38% for structural steel, 17% for lumber and 7% for portland cement. Since 1921, the shifting tide of inflation changed the weight of the CCI components to 82% for labor, 10% for steel, 7% for lumber and 1% for cement. This shift was less dramatic for the BCI, which today consists of 66% for labor, 18% for steel, 13% for lumber and 3% for cement.

A number of readers have incorrectly assumed that the ENR cost indexes are based on quantities of materials used in construction during 1913. They ask if the original weighting should be adjusted to quantities of materials now used. Actually, the original base used was much broader, taking into account production in the overall U.S. economy.

PRODUCTIVITY MEASURE

Both indexes are not adjusted for productivity, managerial efficiency, labor market conditions, contractor overhead and profit or other less tangible cost factors. However, the indexes can be used to get a fix on these intangibles.

During times when productivity is low, the selling price of construction, represented by the final cost of structures in place, will be relatively higher than the ENR index. At the other extreme, when productivity is high and bidding competition is sharp–such as in a recession–the selling price of finished construction will generally fall below ENR's materials and labor costs.

Special-purpose indexes exist that measure selling prices, and many are published in ENR's cost issues (see p. 38). The extent that these vary above or below ENR's indexes gives a rough measure of construction productivity. At the end of 2002, the averaged annual increase for these indexes was 2.2% lower than ENR's CCI, indicating a degree of discounting in a slowing market.

Click below to read more from First Quarterly Cost Report >>

![]() Summary: Surge in energy prices causes cost headaches

Summary: Surge in energy prices causes cost headaches

![]() Asphalt: Oil prices hammer asphalt paving costs

Asphalt: Oil prices hammer asphalt paving costs

![]() Equipment: High fuel prices squeeze operating costs

Equipment: High fuel prices squeeze operating costs