Global Acquisitions Fall in Q3, But Strong Activity in Some Areas

The buying and selling of firms in the engineering-and-construction sector, particularly across borders, has fallen off this year as participants "wait and see" whether global economic, financial and political signs improve, say merger-and-acquisition industry experts.

Financial investors appear to be stepping into the E&C sector in a big way, while deal-making remains strong among design firms and in burgeoning energy and natural-resource markets.

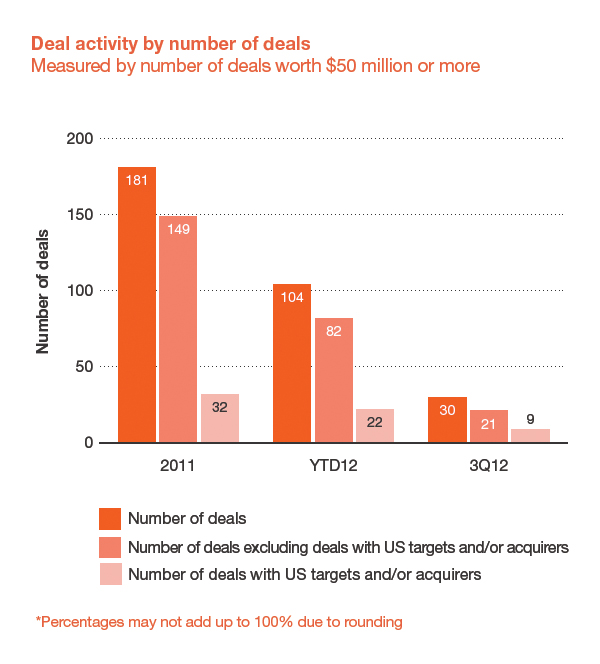

In its third-quarter update released last month, PricewaterhouseCoopers reports 30 deals with a value of $50 million or more, for a total of $11.8 billion, in the three-month period ending on Sept. 30. That compares to 52 deals worth $22.7 billion for the same time in 2011 and 37 transactions worth $10.3 billion in the second quarter of 2012.

PwC says total deal value was up slightly in Q3 due to three "mega-deals" valued at $1 billion or more, compared to only one in the previous quarter. But the firm's survey says the average deal's value "remained flat" at $400 million, year over year.

Mick Morrissey, principal of M&A consulting firm Morrissey Goodale, says the number of global deals the firm has tracked to date is down 7% over the same period last year, with Europe's sovereign crisis and China's slowdown making an impact.

He says, however, that growing energy markets in Canada and Brazil are pushing strong M&A activity there. "Firms in these sectors are commanding premiums," Morrissey says.

Wait-and-See Attitude

“After a very sluggish first half of 2012, M&A activity in the engineering and construction industry continues to lag well behind that of the past two years," says H. Kent Goetjen, a PwC partner and its U.S. engineering and construction leader, citing The continuing global economic slowdown as well as the slowed growth in emerging markets and sluggish U.S. recovery.

Goetjen says that company divestitures "seem to have reached a plateau" over the last several months, "potentially indicating that the right-sizing and geographic reshuffling that was a significant part of transaction activity in 2011 has already happened.”

"As the European Union began experiencing significant difficulties in 2011, E&C companies adjusted their market and product exposure and limited or completely eliminated their presence in this market," Goetjen continues. But PwC's study notes that local M&A activity continued in Europe in Q3, indicating "the continuing reorganization and right-sizing" of the continent's E&C sector.

Goetjen tells ENR that buyers are uncertain about future sources for work, tax-rule changes ahead in 2013 and how acquisitions will be financed. These buyers are wondering how to retain staff to recover their acquisition investment and whether there is sufficient funding to complete a deal and fuel future growth.

Among the specific types of firms whose deals PwC tracked, M&A activity was strongest among construction companies, although most of their transactions were smaller in value. Transactions involving construction-equipment firms and materials suppliers ranked second and third, respectively, in deal volume.

"Geographically, the deals varied, including both local and cross-border transactions in developed countries, such as the U.S. and Luxembourg, and in emerging markets, such as India, Turkey, South Korea and South Africa," says Goetjen. He says China-based firms were the most active in acquisitions both domestically and across borders, followed by the U.S.

Design Firm Deals Are Hot

Consolidation trends appear to be fueling higher-value deals among architecture and engineering firms.

The survey's three mega-deals involved engineers. Chicago Bridge & Iron plans to acquire The Shaw Group Inc., a $3.2-billion transaction set for a shareholder vote on Dec. 20; France's CGG Veritas seeks to buy the geoscience division of Holland's Fugro NV for about $1.55 billion; and Waste Connections Inc. made an offer to buy R360 Environmental Solutions Inc., a Houston provider of oil-field waste management services, in a deal valued at $1.3 billion.

Andrej Avelini, managing director of financial consultant and M&A broker EFCG Inc., which specializes in the engineering sector, reports strong deal activity this year. Based on projections by industry CEOs in a company survey, he foresees about 200 transactions closing by year-end. "There has been a bit of a flurry of deals closing at the end of this year to make the tax deadline," says Avelini. "We see valuations are all-time highs."

Avelini says EFCG was involved in 11 M&A deals this year, about half including non-U.S. participants. While the number is down from 16 transactions it helped broker in 2010, he says "the backlog for 2013 is very strong."

He foresees private equity-fueled deals to continue next year as well as a trend in possible "merger of equals" transactions. "I’d expect one of those to come to fruition in 2013, such as large, employee-owned firms in a stock-for-stock merger."

Adds Goetjen, "after quarters of right-sizing, leaner operations and leaving slower growth markets, E&C companies are running out of ways to improve profitability and are in much better condition to take advantage of the benefits of M&A."