4Q Cost Report: Executive Confidence Falls as Recession Nears

Construction sector foresees a difficult market in the first half of 2023

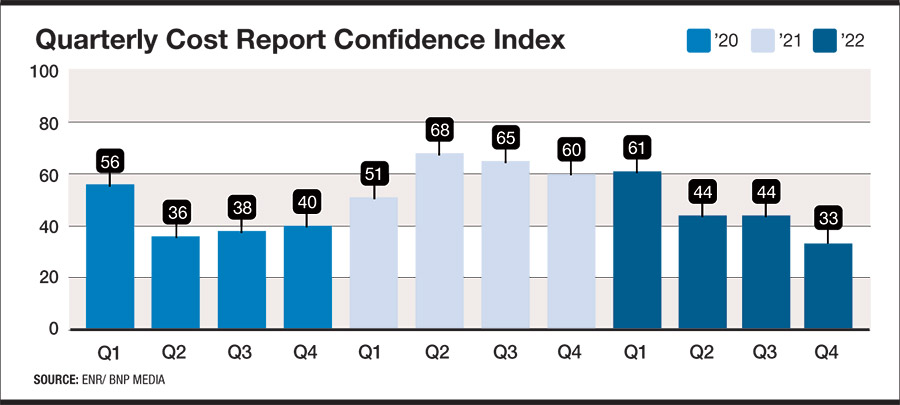

The recession that many economists are predicting has not yet come to pass, but construction industry executives foresee a shrinking market in 2023. ENR’s Construction Industry Confidence Index fell to a 33 rating in the fourth quarter—the slowest reading since the third quarter of 2010. The index had been holding steady at a slightly pessimistic rating of 44 in Q2 and Q3 of this year.

The index measures executive sentiment as to where the current construction market will be in the next three to six months and over a 12- to 18-month period, on a 0-100 scale. A rating above 50 shows a growing market. The measure is based on responses by U.S. executives of leading general contractors, subcontractors and design firms on ENR’s top lists to surveys sent between Oct. 24 and Dec. 5.

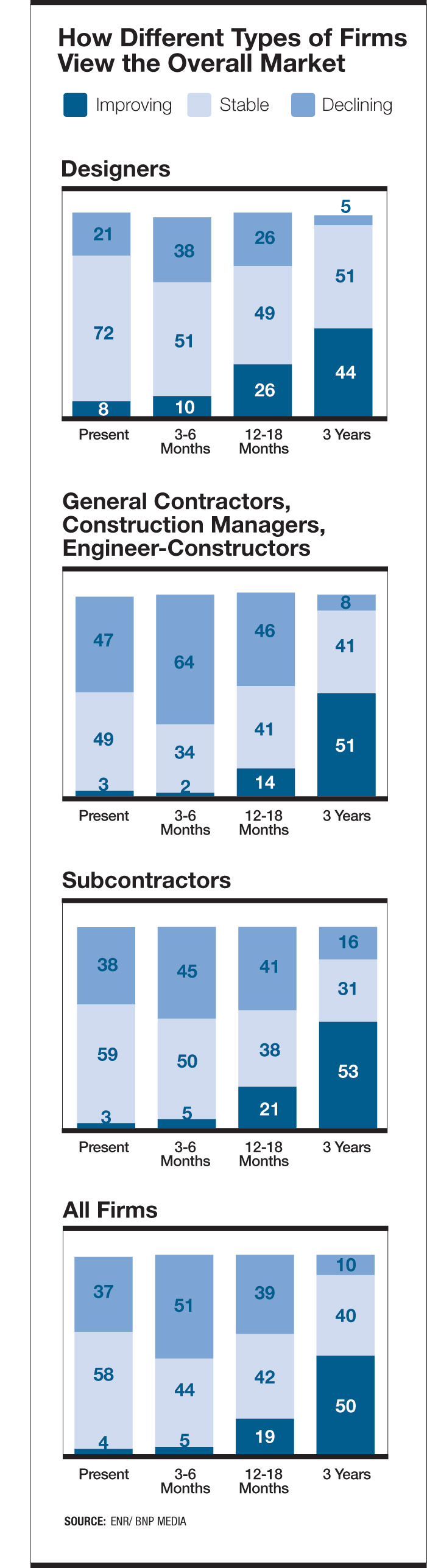

The percentage of respondents who currently see a stable market is nearly unchanged from last quarter, falling from 59.7% to 58.3%. But the proportion who see an improving market dropped precipitously, from 16.2% last quarter to just 4.4% in Q4. Among designers, that drop was especially sharp. About 25% of designers last quarter saw an improving market but only 8% do this quarter. AIA’s Architecture Billings Index fell below 50 in October, the first decline in billings since January 2021, the organization reports.

Construction execs foresee a difficult first half in 2023, with 50.6% anticipating that the market will decline three to six months from now, up from 40.9% last quarter. Construction managers and general contractors are especially pessimistic, with 64% seeing a first half decline next year. Executives are somewhat more optimistic when considering the 12-to-18 month range, with 60.8% seeing the market as stable or improving, although that is down from 65.5% in Q3.

index respondents are even gloomier on the economy as a whole. About 62.2% currently see a declining economy, but that number jumps to 69.2% when considering three to six months in the future. The economic confidence index fell six points to a rating of 24, the second lowest value in index history after the 23 rating in Q2 of this year.

However, results of the latest Confindex survey released by the Construction Financial Management Association (CFMA) still show a fair amount of optimism among construction chief financials officers. Each quarter, the group polls CFOs from general and civil contractors and subcontractors about markets and business conditions. The Confindex is based on four separate financial and market components, each rated on a scale of 1 to 200. A rating of 100 indicates a stable market; higher ratings indicate market growth.

The Confindex stayed steady between Q3 and Q4, at a rating of 103. Remaining indices likewise saw little movement. The “current conditions” index rose 2.8% to a 109 rating. The “financial conditions” index also rose, up 2% to 103. The “business conditions” index fell slightly, down 2.8% to 103. “There’s a lot of positivity about the market right now,” says Stuart Binstock, CEO of CFMA. “Last quarter, 25% [of Confindex survey respondents] said profit was significantly or slightly better. This quarter it was 32%.”

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

*Click on the chart for greater detail

*Click on the chart for greater detail

A Tough Year Ahead

Anirban Basu, the group’s economic adviser and CEO of consultant Sage Policy Group, is surprised by upbeat assessments he hears from construction professionals. Despite the rising cost of capital, continued high materials prices and the worst year for the bond market in decades, “it’s not as if the lightning has flashed and they are waiting for the thunder.” He notes that the Confindex “year ahead outlook” component is only down 3% to a value of 96.

Basu expects a more negative assessment of the market from CFMA members in Q1 of 2023. “The lag in terms of the complete effect of mapped interest rate increase may not be felt for 12-18 months. You’ll start to see the weight of that really hit the economy in 2023.”

Equity markets are yet to respond fully to changing economic circumstances, Basu thinks. “The market is still highly valued. It’s been waiting for the pivot, the Federal Reserve saying, ‘we’re not going to raise rates anymore’.” The Sage CEO does not foresee that happening anytime soon. For him, a tumbling equity market added to the high cost of capital spells a moderate recession. “Something akin to the 1990-1991 recession,” Basu adds.

There is some elevated concern among Confindex respondents, notes Binstock. “Last quarter 18% of CFOs were very or highly concerned about financing. That jumped to 25% this quarter.” Among respondents to ENR’s Confidence index, 60% said client access to financing was somewhat or much tougher than last year.

With supply chain issues lessening, Basu sees rising wages as the principal driver of inflation now. “To get back down to our 2% target inflation, we need something like 3.5% wage growth,” he suggests. Currently, average hourly earnings and other measures of wage inflation are running at around 5%. “The Federal Reserve will need to break this labor market equilibrium,” Basu contends.