After a Rocky Year, PCA Forecasts Slight Growth in Cement Demand in 2021

Cement consumption in the U.S. was wildly uneven in 2020, reflecting the effects of COVID-19-related construction shutdowns and economic disruptions.

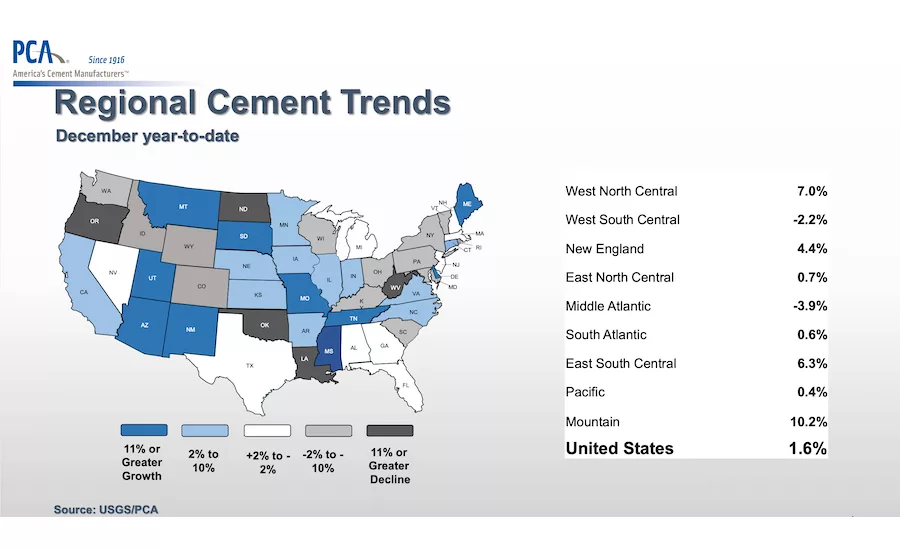

Graphic Courtesy of PCA

PCA is forecasting steady growth in cement consumption after 2021, but much of that may be contingent on a federal infrastructure bill.

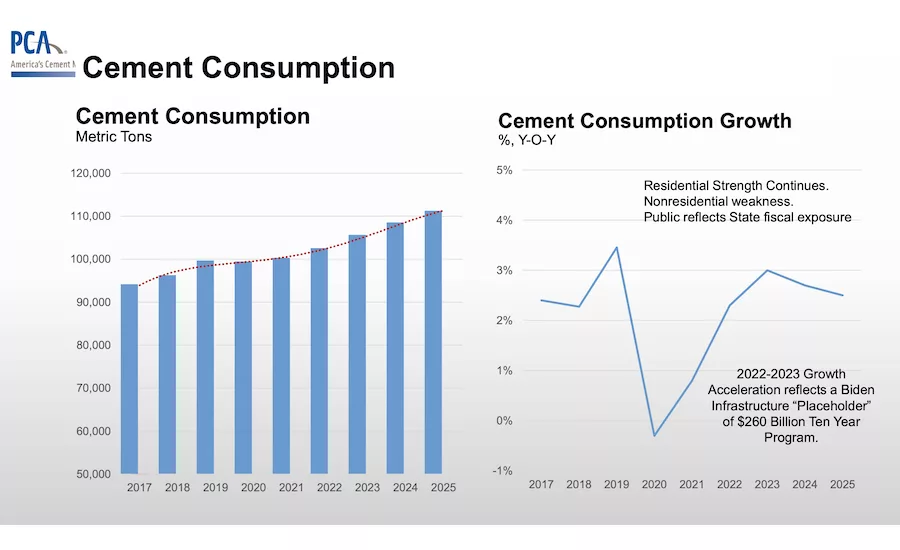

Graphic Courtesy of PCA

Disruptions to the U.S. construction industry caused by the COVID-19 pandemic were significant, but not enough to fully derail what had been an active market, according to new economic forecast data from the Portland Cement Association.

Despite a drop in cement consumption in the middle of 2020, demand came roaring back, and the PCA is now forecasting 1% of growth in cement consumption in 2021.

“Shortly after COVID materialized, we saw second quarter growth drop more than 20%,” says Ed Sullivan, PCA chief economist, who adds cement demand dropped with subsequent COVID outbreaks. But despite the recent resurgence in COVID cases later in the year and ongoing volatility in the economy, the cement market still grew by 1.6% overall in 2020. “It’s remarkable that growth occurred in 2020,” says Sullivan, who notes the last two months of the year saw particularly strong year-over-year growth in concrete consumption, perhaps signaling a stable base for 2021 performance.

PCA’s 1% forecasted growth in cement consumption in 2021 is driven entirely by residential construction, with non-residential and public construction expected to continue their weak performance through 2021.

Shifting habits due to the pandemic has some office and retail construction work on hold or delayed, says Sullivan, and state governments are facing reduced revenues, curtailing new public projects.

The lack of federal funding so far to shore up state budgets is partially to blame for holding back economic growth and dragging public construction projects, says Sullivan. “The fiscal duress [in state budgets] is significant,” he says. “It will cause some states to cut back, to lay off workers, to curb construction efforts, resulting in less cement consumption.”

When a COVID relief bill passed in December did not include significant aid to states, the crisis only deepened, adds Sullivan. “There’s discussion that yet another federal COVID relief program is coming,” he says, referring to the $1.9-trillion package currently being advocated by the Biden Administration. “But the critical avenue that must be addressed is support for the states. Otherwise, the adverse impact on our forecast going forward looms somewhat larger.”

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

The proposal advocated by Biden and congressional Democrats does include state aid. But Sullivan remains skeptical, as direct aid to state governments has ended up on the chopping block in previous COVID relief negotiations in congress.

“To the extent that [aid to states] isn’t supported in a federal COVID relief bill, and if the vaccination effort takes longer than expected, that means the [nation’s] economy will run subpar," says Sullivan. "Revenue collections won't accelerate as fast as some expect, which suggests fiscal duress on states could continue. I could then see a continued drag on public construction, not only this year but next year as well.”

The COVID-19 pandemic has also led to a broad shift in the working and shopping habits of many Americans, and if some of these changes became permanent it would have a considerable effect on the non-residential construction sector, says Sullivan. PCA has examined some of these trends, a few of which were already underway. “With non-residential, there’s a lot of latent structural factors at work occurring on a long-term basis,” says Sullivan. “The shift to work-from-home, the growth of e-retail, COVID accelerated all of these factors.”

Changes in the office market as some companies move to a hybrid model of onsite and remote workers could impact demand for office space, but PCA is more concerned about the accelerated decline of the retail market. “Because of COVID we’re seeing more people shop online, and those that weren’t as comfortable with that route are now OK with it,” says Sullivan. “That suggests less retail space, fewer parking spots. And parking garages are a big cement consumer.”

But the long-term outlook overall for the industry is still fairly optimistic. While growth in cement consumption is expected to be relatively flat this year, PCA is forecasting slow, but steady growth in the years after 2021, which could be even further accelerated if the effects of federal spending kick in as well. “The big wildcard [for the cement market] is the potential of a federal infrastructure bill,” says Sullivan. “Otherwise the recovery could be very slow and tepid.”