Risk Management

Will Contractors Limit Weather Risk With Indexed Insurance?

Record rainfalls, such as those from Hurricane Harvey in 2017 that led to floods engulfing equipment in West Columbia, Texas, have provoked ideas about weather insurance and how it could help construction.

PHOTO BY LUKE SHARRETT/BLOOMBERG VIA GETTY IMAGES

A winter nor’easter, described in the media as “snowzilla” because of its historic proportions, slammed the U.S. mid-Atlantic states on a January weekend in 2016, dumping more than 2 ft of snow on New York City. At times, winds exceeded 35 mph. Among the projects where heavy accumulations had to be shoveled the following Monday was Manhattan’s sprawling Hudson Yards mixed-use development. Photos (see cover) show crews doing the shoveling and a crane being used to remove the snow.

It isn’t clear if contractors at work there, such as Tutor Perini Corp., were affected, since the public company’s financial reports contain standard warnings about how weather can affect revenue and profitability. The company’s filings make no special mention of the blizzard, and the firm did not return a call for comment.

But the complications of figuring out how much snow actually fell can be appreciated by the amount of time it took the National Weather Service to fix the final totals. Four months after the storm, the service declared the readings in the city’s Central Park and at nearby Newark (N.J.) Liberty International Airport to be slightly off, blaming measurement errors and miscommunications.

While what is reliable data is not always 100% clear, such coverage feels especially important amid stronger signs of climate change and the more turbulent weather patterns it is driving.

Reliable weather data is at the heart of parametric weather insurance, a popular form of coverage in the energy sector that insurers and brokerages believe could gain traction and alleviate some risk for those in construction and engineering. While what is reliable data is not always 100% clear, such coverage feels especially important amid stronger signs of climate change and the more turbulent weather patterns it is driving.

“We are seeing parametric insurance gradually taking off,” says Nigel Brook, a partner at Clyde & Co., a London-based legal practice. “It’s not the kind of thing where a customer says ‘I want parametric insurance.’ It is usually a thing they find their way indirectly to.”

Weather insurance of all kinds has a long track record in energy, agriculture, events and retailing. Just what it can mean for construction isn’t clear yet. Parametric insurance can provide an extra level of protection for contractors and project owners. One attraction is its seeming simplicity, with a clear trigger to a comparatively quickly delivered payout and no convoluted claims process, participants say.

While a builders’ risk policy, which covers property damage during construction, can run to dozens of pages in length, parametric policies can be as short as 10. Parametric insurance is designed to eliminate the cumbersome claims process and the myriad exclusions that can lead to disputes, but it is hardly foolproof.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

In one form or another, parametric insurance has been around for roughly three decades. In its early years, companies, major public owners and insurers looked to hedge their bets in the event of a disaster such as an earthquake or hurricane through a form of reinsurance called catastrophe bonds. Utilities and energy companies were also early pioneers, using derivatives to hedge against spikes in demand and prices on wholesale markets during cold snaps.

Utilities would reap payment under the so-called “heating degree day” derivative contracts, the trigger being when the temperature fell a specified number below 64° F.

Building on that risk-hedging derivative concept, insurance carriers and brokers have developed other indexed weather insurance products that have gained broader appeal across the larger business community.

“We took that derivative concept and transformed it into an insurance product,” says Paul Ramiz, a director for innovation and solutions at broker Aon. “That is where you are seeing more appetite. It’s coming from the business community.” The ever-expanding array of new products are now reaching into new sectors, such as construction and engineering.

Where it has been used, parametric insurance can complement traditional builders’ risk policies, which may not work as well in situations such as project delays and where there is no physical damage on which to base a claim.

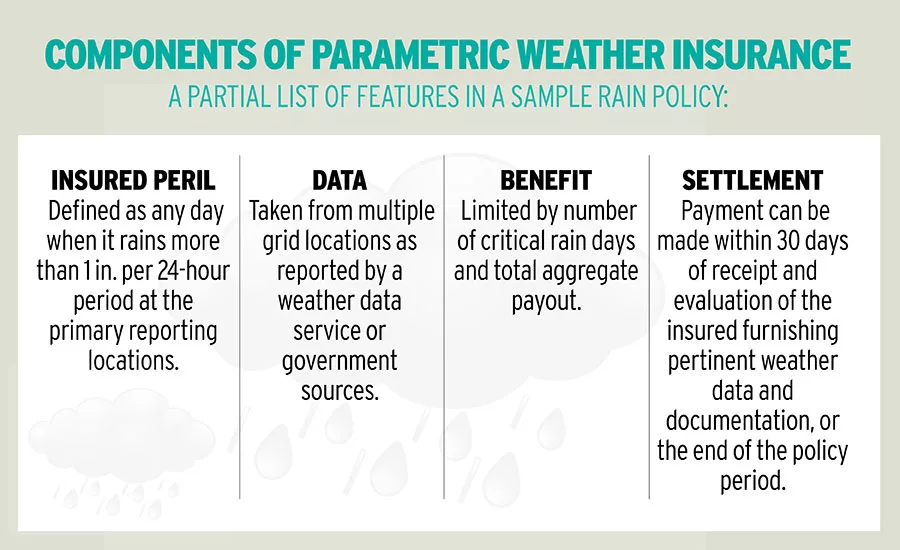

Parametric insurance in theory cuts out what can be a time-consuming and cumbersome claims process, with coverage triggered by a certain agreed-upon measurement or condition, such as the designation of a named storm. Once that trigger is reached, the insurer makes the payout, whether or not there is actually any damage to the project. The payout, according to one sample rain policy examined by ENR, may be subject to an evaluation of the data and documentation provided by the insured to the insurer. But 30 days after receipt and evaluation, or the end of the policy period, the check should go into the mail, the sample policy states. Terms, of course, will vary.

Satellite Eyes

The still-unfolding technology revolution—and the explosion in both satellite-gathered weather data and computing power—has played a key role in helping parametric insurance come of age. A rapidly growing number of satellite eyes gazing down from space now allow insurers and risk managers to slice and dice data in an ever more granular fashion.

With use of satellite imagery, it now is possible to track historic weather patterns on a grid back to 1979, zeroing in on three- to six-hour increments, even in remote areas without nearby weather stations, notes Martin Malinow, president of Sompo Global Weather, a unit of insurance giant Sompo International.

There are now as many as 10 different satellite weather databases to use, according to Malinow, with NASA and the National Oceanic and Atmospheric Administration (of which the National Weather Services is a part) as prominent players. NOAA’s Climate Reference Network uses instrument stations equipped with a weighing precipitation gauge that has three load-cell sensors to provide three independent measurements of depth change, in millimeters, at 5-minute intervals. Those values are then used in an algorithm to derive the station’s official 5-minute and hourly precipitation values. There are now several governments and international organizations across the world with their own weather tracking agencies offering data to be crunched and analyzed.

Photo by Famartin via Wikimedia Commons

The data explosion, in turn, has enabled risk managers, contractors and insurers to develop products and ever-more sophisticated triggers for coverage. In addition to named storms as triggers, other types include storm intensity, such as all hurricanes up to Category 3.

The array of weather policies has expanded dramatically since the early days of the field, with variations available to cover extreme heat, cold, rainfall and now snowfall. As the amount of data and the ability to analyze it have grown, risk managers, brokers and insurers have been able to get ever more granular in their design of policy triggers. They now include the number of inches of rain over a certain time period, heat and humidity levels, wind speed, waves reaching particular heights, or so many inches of snow.

“You can control materials and labor,” Malinow says. “The one thing you can’t control in construction, and that is [too often] left swinging in the wind, is the weather.”

Volatile weather, whether connected to climate change or not, is a major selling point, with contractors, engineering firms and others having to grapple with delays caused by extreme rainfall and supercharged hurricanes. A pivotal event was Hurricane Harvey in 2018, which left large swaths of the Houston area underwater, playing havoc with construction sector firms and project owners.

|

Michael DeLio, director of brokerage analytics and risk strategies at Aon’s construction services group, says there is growing interest in construction.

Sompo’s beachhead in the U.S. market came after the insurer and Malinow landed a major parametric insurance contract in 2013 on an iron mine and port complex in northwest Australia. The mine developer was on the hook to cover any construction work stoppage because of a named storm, so the project’s lender insisted the developer insure itself against possible cyclone damage. Working with the developer and a broker, Malinow created a policy that provided coverage for the two-year construction period and another year as work wound down. There was also a trigger in case of extreme rainfall, with a separate specified payout rate for each millimeter above an agreed-upon threshold at three weather stations near the project site.

By the late 2010s, Sompo had decided to build on its experience in Australia to tap potential demand in the construction industry in the U.S.

“For six or seven years we kept asking ourselves, ‘Why aren’t more contractors doing this?’ ” Malinow recalls. “ ‘Why are they escrowing money away on the balance sheet as opposed to buying a parametric policy?’ ”

Pipeline construction is particularly sensitive to weather delays, and provided Sompo a chance to customize a parametric weather policy in the U.S.

Last year, extreme rainfall had triggered a series of big delays on a major crude oil pipeline extending several hundred miles. With the work roughly two-thirds complete, and deadlines and penalties looming, the contractor decided it would need some insurance protection against the weather. The contractor started working with broker Aon and Sompo, but designing a parametric insurance policy for the project, with work taking place in remote parts of multiple states, was easier said than done. There were no nearby weather stations from which to take readings.

Sompo turned to satellites that would monitor the pipeline route at six different points plotted on a grid. The insurer also researched historic rainfall at those points. The parametric insurance policy was to cover only the last few months of work on the pipeline. When rainfall at any of the six grid points rose above a certain number of inches, the policy would have called for a payout to cover a lost workday.

The second layer of the policy covered extreme rainfall over a 10-day period. If rainfall exceeded 20 in. at any one of the six grid points along the project, the contractor would be in line to receive a multimillion-dollar payout. The policy’s third layer covered catastrophic rain damage that resulted in several days or more of lost work. All told, the policy provided $10 million in total coverage to the pipeline contractor.

Higher Stakes

The stakes can be higher with weather that affects offshore projects, such as wind-farm construction. That type of work, which involves ships and large amounts of expensive equipment, is likely to have triggers based on wave heights or wind speed.

For example, if a ship cannot leave port for several days because of choppy seas—but the policy’s trigger is 3.9 meters and the waves are 3.8 m high—the contractor could be left without coverage for a multimillion-dollar loss, notes British attorney Brook. One option is progressive payouts based on tiered triggers. This could help reduce the amount of basis risk—the difference between the actual damage suffered and the amount of the payout.

Then there is the issue of measurement accuracy and the well-known truth that weather is an extremely local phenomenon. One contractor building a 250-mile-long pipeline in Virginia had a big problem that its parametric insurance policy was supposed to solve, yet it hadn’t. A tropical deluge had dumped a massive amount on rainfall on the project, disrupting construction and causing extensive damage. The policy trigger had been set at 10 in. of rain over a rolling, 20-day period. If the rain total of any 20-day period rose above the 10-in. mark, the pipeline contractor would have stood to collect $250,000.

Several weather stations were used to track rainfall along the 250-mile length of the pipeline, including one weather station that was 11.9 miles away from a section of pipeline that was going to get drenched.

By the contractor’s own measurement, the storm had dumped more than 10 in. of rain. But the weather station miles away from the pipeline put the amount of rainfall at 8.8 in.

Many pipeline contractors carry their own rain gauges and will push to “use their own data set,” said Aon’s DeLio. However, he cautions, “You don’t want someone standing out there with a garden hose triggering the policy.”

But once all sides agree to a data source, barring some dramatic problem, there should be no “wiggle room,” he added. Aon’s Ramiz says there can be issues if the weather stations have been installed or monitored incorrectly. But he added that improved sensors and more satellite data will limit such problems in the future.

As in traditional insurance, parametric insurance comes with a level of basis risk. 'This is the big problem.'

– David Eckles, a professor in the University of Georgia’s risk management and insurance program

As in traditional insurance, parametric insurance comes with a level of basis risk. “This is the big problem,” says David Eckles, a professor in the University of Georgia’s risk management and insurance program. “It is whether or not the event, the trigger, will cover your loss. … You have damage, but you get nothing.”

The interest in parametric weather insurance from other specialized construction sectors still seems limited, however. Few U.S. construction contractors have purchased such policies so far.

Parametric weather insurance has a limited legal track record in U.S. construction, too. At a recent conference in a session on the subject, no one could think of a disputed claim involving parametric weather insurance.

Foundation contractors contacted by ENR directly or through informal surveys mostly stated that they either had never heard of weather insurance for their industry or that they relied on traditional builders risk policies.

James Baty, executive director of the Concrete Foundations Association and the manager for regulatory and technical affairs for the Tilt-Up Concrete Association, said it would be “hard to find weather scenarios that would impact this culture of contractors.”

And contractors polled at another association, for deep foundations, said they were aware of parametric weather policies. “We have heard pitches for this type of coverage” to be used on a job-by-job basis, said one, but “we have not ever used it.”