A Solid 2017 Fuels Stronger Growth for Region’s Contractors

E.E. Reed Construction completed work on this 1.11-million-sq-ft mixed-use project in December 2017.

PHOTO COURTESY OF E.E. REED CONSTRUCTION

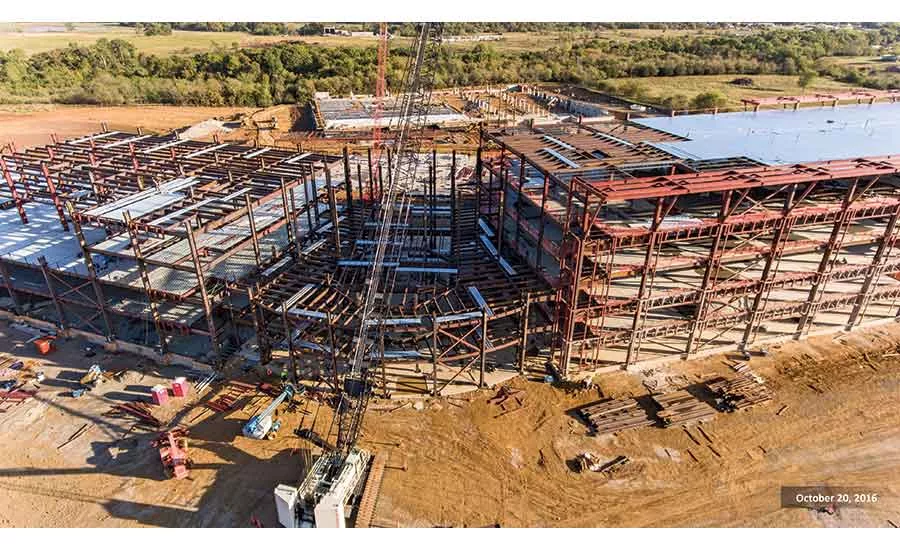

Manhattan Construction completed the new Tribal Headquarters Complex for the Choctaw Nation in Durant, Okla., earlier this year. Shown left is an Oct. 2016 progress photo.

PHOTO COURTESY OF MANHATTAN CONSTRUCTION GROUP

During 2017, Manhattan Construction completed the final phases of the Star Omni Hotel and Retail complex in Frisco, Texas.

PHOTO COURTESY OF MANHATTAN CONSTRUCTION GROUP

In May, McCarthy Building Cos. completed work on the $260-million phase I of a two-part expansion at The Museum of Fine Arts, Houston, which encompassed construction of the Glassell School of Art.

PHOTO COURTESY OF MCCARTHY BUILDING COS.

Construction markets across the Texas-Louisiana region continued to show strength over the last year and a half, according to some of the region’s leading contractors.

Reported 2017 regional revenue among the top 100 firms on ENR Texas & Louisiana’s 2018 Top Contractors ranking totaled $42.38 billion across the five-state region of Arkansas, Louisiana, Mississippi, Oklahoma and Texas, compared to $40.95 billion in 2016.

A state-by-state analysis shows that three out of five states in the region experienced construction growth during 2017. The top 10 contractors in Arkansas saw revenues of $740 million in 2017, compared to $480 million in 2016. In Louisiana, revenues for the top 10 contractors were somewhat lower, at $4.23 billion, compared to $4.49 billion in 2016.

Meanwhile, Oklahoma’s top 10 firms reported regional revenue of $1.9 billion in 2017, up from $1.69 billion the previous year. Regional revenue for the top 10 contractors in Texas also grew, reaching $11.46 billion in 2017, up from $10.68 billion in 2016.

Mississippi was the only state in the region where the top firms saw significantly less revenue last year, with $632 million reported by the state’s top 10 contractors, compared to $1.8 billion in 2016. Local construction associations have noted that state budget issues continue to limit investment in infrastructure across Mississippi, as has the loss of incentives such as historic-preservation tax credits.

“The markets where we build are booming, with projects across nearly every industry sector,” notes Joe Jouvenal, senior vice president operations and Dallas business unit leader at Dallas-based McCarthy Building Cos.

The firm experienced significant year-on-year growth from 2016 to 2017 of 23% in Texas alone, Jouvenal adds, with McCarthy reporting regional revenue of $799 million for 2017.

“In Dallas-Fort Worth, the construction pipeline topped $23.4 billion in 2017. Real estate executives forecast even more projects launching this year despite labor shortages impacting the construction cycle and cost of development,” he says.

Additionally, McCarthy is seeing an increase in owners hiring the firm in a CMAR capacity through a negotiated process rather than through hard bid.

“Over the past 12 months, we’ve seen these CMAR contracts more closely resemble an integrated project-delivery method, with close collaboration between design and construction as we’re hired earlier in the process,” Jouvenal says. “We welcome this trend, as we feel it facilitates the owner getting the most building for her/his dollar.”

With more people moving south, contractors are seeing more projects in K-12 education, health care, municipal and other support services, adds Eric Krueger, executive vice president at Balfour Beatty, Dallas. “We continue to see more emphasis on social service needs to support all the families moving to the state. We see this trend continuing for the foreseeable future,” Krueger says.

Balfour Beatty reported $1.3 billion in regional revenue during 2017, just slightly under its 2016 figures, thanks to a solid backlog of diverse projects.

“We also we made a strategic decision to exit the wood-frame multifamily market to allow us to really focus more on our core business in commercial office, K-12 education, health care, municipal, high-rise residential, hospitality and interiors and special projects,” Krueger says.

The firm is finding that more owners are turning to design-assist and design-build, he adds. “Innovation and advances in technology, especially in regard to offsite manufacturing, prefab and pre-assembly, continue to be important, especially given the tight labor conditions,” he adds.

Sugar Land, Texas-based E.E. Reed Construction has started a number of new projects ranging from health care to hospitality, says Patti Miller, vice president of business development. “The office market is still very stagnant,” she says. “However, the industrial build-to-suit market is booming and making up for it,” Miller adds.

Over the last year, E.E. Reed has expanded into Savannah, Ga., where the business climate is similar to Texas, Miller says. “We’ve already seen a positive impact from expanding into that market,” she adds.

While CMAR continues to be a standard delivery method for Tulsa, Okla.-based Manhattan Construction Group in the vertical construction space, the firm is seeing growth in design-build delivery, says President Larry Rooney.

“The increased number of pursuits for design-build is intriguing to us and continues to show great efficiency for clients who want a single source to work with,” he says. “This region continues to be one of the largest and best-performing for our business.”

Contracting strategies are evolving across the industry, points out Stephen Toups, executive vice president at Turner Industries, Baton Rouge.

“It may actually be a regular cycle, but with additional work on the horizon, we are noticing a marked difference in the way that some of our customer are handling what the future may bring,” he says. “Some are business-as-usual, while others are preparing and researching now to find the next contracting strategy which, in some instances, is to identify the best partner and then create an alliance to get the work completed as safely and cost effectively as possible.”

While 2017 was a good year for Turner, it wasn’t a great one, Toups says. The firm posted $2.34 billion in regional revenue in 2017, slightly down from 2016’s $2.32 billion.

“But we saw the addition of some great people, a safe work record, and innovations in training. We were able to use the pace of 2017 to prepare for where we are now—a little more growth than expected and looking at an accelerating 2019 through 2020,” Toups says.

Turner’s equipment division will relocate its New Orleans offices out of the busier areas of town to a safer location to help the team serve a larger portion of the market, while the firm’s Houston offices are preparing to expand.

And while 2018 won’t be a record-setting year for Turner, it is looking to be a nice increase over 2017, Toups adds.

“We are watching many more decisions in our business come from HQ. While that is not a bad thing, input from the personnel actually performing the work must be taken into account,” he says. “At the end of the day, we are seeing a driving force toward TCO—Total Cost of Ownership. Many contractors may not be the lowest price but could deliver the best value and in turn, the lowest TCO.”

Ultimately, the construction cycle in the Texas-Louisiana region is robust, Jouvenal says. Population growth will continue to spur the need to upgrade dated facilities and build new ones, he adds.

“We anticipate the remainder of 2018 to be characterized by continued intense construction activity,” Jouvenal says.

Areas of concern moving forward include inflation in the cost of materials and labor, which continue to strain the financial outcomes of some projects, adds Rooney.

Skilled workers are aging out of the workforce, and an insufficient number of replacements are entering it, Jouvenal notes. “In fact, for every four-and-a-half-to-five people who age out, only one person enters,” he says. “Perception of what a career in construction entails contributes to the problem—the recruitment, retention and development of the construction industry is a priority,” he says.

The industry will need thousands of new employees to stay competitive, Jouvenal adds.

“We’ve been blessed to be well established in Texas the last several years, given the great business climate that’s resulted in growth with so many companies moving to the state,” Krueger says. “That and the increase in oil prices has really caused almost all sectors in Texas to rise in the last 12 to 18 months. Moving forward, we don’t see the pace of private development continuing at the same rate, although we also don’t see a major downturn like we’ve seen in past cycles.”