Texas, Louisiana Builders Optimistic As 2018 Approaches

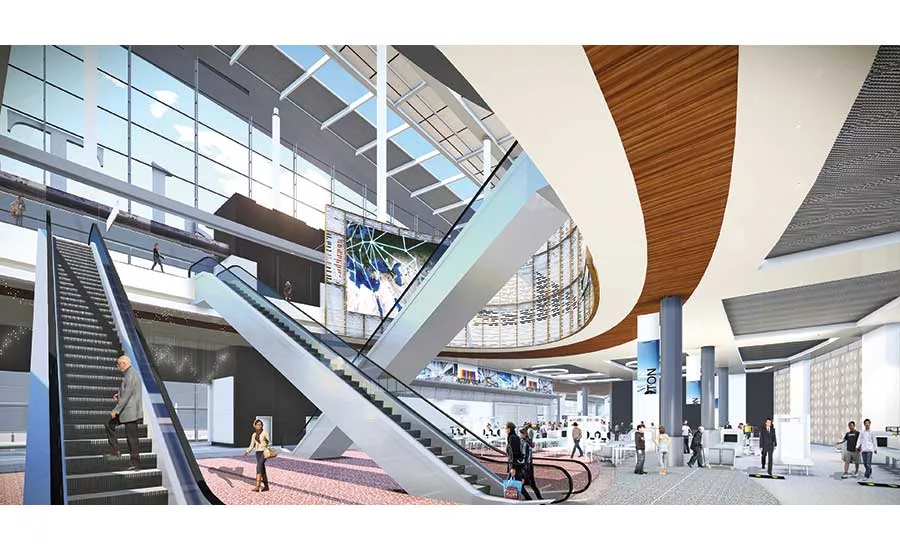

The city of Houston recently selected a joint venture of Austin Commercial and Gilbane Building Co. as construction manager for the new Mickey Leland International Terminal at George Bush International Airport.

RENDERING COURTESY OF AUSTIN COMMERCIAL/GILBANE BUILDING CO.

McCarthy Building Cos. is leading construction efforts on the $80-million Kinder High School for the Performing and Visual Arts in Houston.

PHOTO COURTESY OF MCCARTHY BUILDING COS.

This 12-story Class A office building in Dallas is located across from Kylde Warren Park. Contractor McCarthy Buildling Cos. completed the job in 2016.

PHOTO COURTESY OF MCCARTHY BUILDING COS.

Gilbane Building Co. recently completed work on the new Phillips 66 Campus in West Houston.

PHOTO COURTESY OF GILBANE BUILDING CO.

Gilbane built the eighth high school for Katy, Texas, the Patricia E. Paetow High School, which will open this fall.

PHOTO COURTESY OF GILBANE BUILDING CO.

Many of the region’s top contractors report a slower start to 2017 across Texas and Louisiana. While industry leaders remain optimistic and firms are completing plenty of projects, some market sectors lag their performance of past years, especially oil and gas. Shifts in the marketplace mean that contractors must remain nimble, diverse and adaptive to stay competitive.

Three Texas cities are among the top 20 metropolitan areas in the U.S. for building and multifamily construction starts in 2016, according to Dodge Data & Analytics. Dallas-Fort Worth is fifth largest with $8 billion in new projects, up 16% from 2015, Houston-Baytown-Sugar Land is 12th on the list at $3.2 billion, down 28%, and Austin-Round Rock is 13th, at $3 billion, up 13%. Texas is the only state in the region to make Dodge’s top 20 list of starts.

With the expanded regional coverage for ENR Texas & Louisiana—which now includes Arkansas, Oklahoma and Mississippi—many contracting firms reported additional revenue from the past year. The top 100 firms on the ENR regional list reported a combined $40.95 billion in revenue for 2016 across all five states, compared with nearly $35.6 billion reported by the top 100 firms in Texas and Louisiana in 2015.

Kiewit Corp., for example, reported regional revenue of $1.4 billion in 2016, up $263 million from the previous year, with $225.5 million of that total coming from work in Arkansas and Oklahoma. Among Kiewit’s key projects in those states are the Grand River Energy Center, in Chouteau, Okla., and Hawg Wild Highway in Little Rock.

“As we look at last year and into this year, you’re still seeing a lot of construction starts, both from the horizontal and vertical markets,” says Ray Sedey, Texas region president for McCarthy Building Cos. “On the horizontal—the transportation side and the marine work—we’re seeing a lot of great opportunities.

TxDOT is embarking on a 10-year capital improvement program that will introduce billions of dollars a year into transportation work throughout the state of Texas. That’ll be going on for about 10 years.”

Oil prices will affect construction starts moving forward. As prices rise, more opportunities will surface, he adds.

“There’s also a lot of work on the marine side. We’re seeing more opportunities on the public side—Port of Houston, Port of Shreveport—but we’re also seeing a lot of private clients we work along with in the Houston Ship Channel embarking on some expansions,” Sedey says.

ENR Texas & Louisiana 2017 Top Contractors

Vertical Building

Many segments of the vertical markets are still thriving. Although the first half of the year was soft for McCarthy, Sedey says the firm has landed more opportunities in Dallas, Houston and the civil market.

“In the past, whenever you see a little bit of slowing coming into the middle of the year, a lot of times it’s because projects didn’t ultimately materialize, but one of the things we’re seeing is the projects aren’t going away. We just had a lot of them push out to the back end of 2017 and early 2018,” Sedey says. “That’s not unique to Texas—it’s something we’re experiencing in a lot of parts of the country right now, and it’s more of a kind of wait and see mentality. “

McCarthy’s regional revenue reached $700 million in 2016, $120 million above 2015 totals, and the firm expects another $200 million increase in 2017, Sedey says.

Diversity has been a key for the firm. Recent projects include the Southwest Airlines Wings project in Dallas, an expansion to Christus Spohn Health System’s Corpus Christi campus, the new High School for the Performing and Visual Arts in Houston and the Glassel School of Arts for the Museum of Fine Arts Houston, along with work for the Port of Houston and TxDOT.

“It’s a very diverse work program, but I think that’s what’s going to ultimately help us to grow in a reasonable manner in the years to come,” Sedey says.

A pursuit of market flexibility is helping keep Gilbane Building Co. busy as well, explains senior vice president Dan Gilbane. “What we’ve tried to do is the Wayne Gretzky—go where the puck is going to be, not where the puck is,” he says.

While the firm’s regional revenue declined by about $150 million year over year, to $604 million, “the reality is that we are probably overall about flat,” he says. “We had a good change in the mix of our business, but we have several large projects that aren’t in this geographic region, particularly in Mexico.”

The firm also is working on the $1.5-billion renovation and expansion of a Constellation Brands’ Nava brewery in Mexicali, Mexico.

Houston’s market has been considerably slower than the rest of the state, and Gilbane has adapted to accommodate those changes. In 2007, Gilbane’s project mix was 60% in K-12 schools, then in 2012, it was 85% in office buildings and in 2016-17, it’s about 40% industrial, 30% K-12 schools and minimal office work.

“At the start of the year, there was 11 million sq ft of sublease space on the market in Houston, so the supply-and-demand equation is a little out of whack, and that’s somewhat similar on multifamily overall,” Gilbane says. “There are a lot of deliveries coming into the market, and job growth and population growth, while still positive, are not where they were at $120 per barrel for oil. That’s the silver bullet in all this—commodity prices have dropped considerably, a lot of people have much less disposable income on the multifamily side and companies have downsized considerably on the corporate commercial side.”

Gilbane is currently at work on several major K-12 projects in Houston, including Lamar High School, Katy High School No. 8 and Cy-Fair High School and Elementary School No. 12. Gilbane also recently won the $472-million Mickey Leland International Terminal project from the city of Houston.

Other Markets

Uncertainty is affecting the regional health care sector.

“One thing we’re really keeping an eye on is there have been a lot of leadership changes in the health care arena,” Gilbane says. “When you look at the Houston Medical Center; St. Luke’s, their CEO left; Memorial Hermann, their CEO left; MD Anderson, their CEO left—I think a lot of that relates back to the uncertainty from a legislative perspective from the federal government with Obamacare and what Trump may or may not do here.

“Our crystal ball says that we should see a steady rise in activity as we approach 2019.”

– Stephen M. Toups, Executive Vice President, Turner Industries Group LLC

“Given so much change across the client side, we’re waiting to see what the impact there is,” he adds.

Federal work also has declined since the November election, Gilbane adds. “We’re keeping a close eye on the legislative environment.”

More P3 projects have emerged in Texas, particularly in the north and central markets, which remain incredibly strong, notes David B. Walls, president and CEO of Austin Industries. The firm reported $1.08 billion in 2016 regional revenue, a $259-million increase from 2015 due to increased activity in both the public and private sectors.

“Higher education and municipal and county work is attributed to the growth in the public sector, while private development work continued to see rapid and extensive growth from three key areas: corporate relocations, existing Texas-based companies expanding their footprint within the state and shell office buildings in the Class A and AA space,” Walls says. “Specific to Austin Commercial, the regional impacts of shell office buildings, corporate build-to-suit developments, hospitality, sports, health care and aviation have allowed Austin to realize marked growth in revenue.”

A subsidiary, Austin Bridge & Road, recently teamed with Kiewit on a joint venture to build the $814-million Midtown Express Project, a reconstruction of about 28 miles of highway through Euless, Irving and Dallas, including the rebuild of the interchange at Loop 12-SH 114-SH 183 at the old Dallas Cowboys Stadium.

“The passage of propositions 1 and 7 have provided predictable and increased funding for transportation in Texas. The impact of these will be felt more in late 2017 and then in 2018,” Walls adds.

Work continues in the petroleum sector, despite a drop in the number of major projects starts. Turner Industries Group LLC dipped $283 million in regional revenue to $2.32 billion in 2016 over 2015, but much of that decrease can be attributed to the fact that a lot of its major work didn’t take place in 2016.

“The industry continues to find ways to operate more efficiently,” says Stephen M. Toups, executive vice president at Turner. “Consequently, those large events don’t take place as often as they did in the past. We know there is future turnaround work in the planning stages, and we’re looking forward to being awarded our share of that work when it occurs.”

Turner Industries was recently selected as general contractor on the $717-million, 425,000-ton addition to Shell’s Geismar facility, scheduled to be complete and begin operations in early 2018. At its peak, it will provide nearly 1,600 construction jobs, Toups adds.

The Sasol North America Mega Project continues in Westlake, La., where Turner is self-performing a large portion of the piping and mechanical work on the project. Work began in October 2014 and will finish in June 2019 at an installation cost of $11 billion.

Even though 2017 has started off on the slower side, the market is improving, Sedey says.

Dodge noted that the manufacturing sector in June increased 35% nationally, lifted by the start of a $1.8-billion methane plant in Louisiana. Also, large electric utility projects starts in June included a $296-million wind farm in Texas and several large natural gas pipeline projects that began in May, including the $690-million Gulf South Coastal Bend Header Pipeline in Texas.

Texas was also one of the top five states in terms of the dollar amount of new highway and bridge construction starts, according to Dodge.

“This business has always been cyclical,” Toups says. “You can look back and see six- to seven-year cycles, depending on the services offered. Construction markets in the Gulf Coast area have fared well in the last cycle, and we are optimistic about seeing another upturn in the coming months.”

While much of that depends on many national and international variables, Toups says, “Our crystal ball says that we should see a steady rise in activity as we approach 2019.”

In the meantime, workforce continues to be a problem for contractors throughout the region. “That’s going to continue to be a challenge for us, especially as oil prices rise, which eventually they will, and as oil prices rise, you’re going to have more demand on craft labor and on the managerial labor force,” Sedey says.

AGC of America reported on Aug. 2 that the largest year-over-year construction job loss between June 2016 and June 2017 was seen in Houston-The Woodlands-Sugar Land, which posted a drop of 5,200, or 2% of construction-related jobs.

While contractors continue to reach out to high schools and colleges for help through the ACE (Architecture, Construction, Engineering) Mentoring Program and other workforce initiatives, shortages persist. A greater percentage of talented women are coming into the business, and firms like Gilbane are taking steps such as amending family leave policies to further entice skilled workers, Gilbane says.

“We’re trying to do what we can to ensure the future of the construction business,” he says. “There are mitigating factors to that: There is a lot of prefabrication, and I know there was a big buzz last week or two weeks ago where pundits were saying that by 2050 there won’t be humans on construction sites. I don’t know if I believe that. In the near term, we need human beings on construction sites, and there aren’t enough of them.”