2016 2Q Cost Report

Construction Costs Absorb Two Big Hits This Quarter

Two big events hit construction this quarter: Brexit—that is, the British vote to leave the European Union— and the U.S government’s decision to increase tariff duties on Chinese cold-rolled flat steel by 522%. However, neither will have much of an impact on domestic construction costs, according to ENR’s sources.

Two big events hit construction this quarter: Brexit—that is, the British vote to leave the European Union— and the U.S government’s decision to increase tariff duties on Chinese cold-rolled flat steel by 522%. However, neither will have much of an impact on domestic construction costs, according to ENR’s sources.

Julian Anderson, president of Rider Levett Bucknall’s (RLB) North American operations, has spent the past week in London talking with politicians, contractors, owners and economists about the potential effects of Brexit. Their initial conclusion is that the U.K. should brace for a recession that could spread to Europe. “Some large building projects are already being recalled for reconsideration,” he says.

However, the impact of that recession rippling across the pond will be small, Anderson says. In the short term, the U.S. Fed probably will hold off on raising interest rates until the initial furor over the Brexit vote settles down; such a move by the Fed would be good for construction, Anderson says. However, U.S. contractors working abroad likely will face more aggressive bids from U.K. contractors, which will be helped by a weaker U.K. pound.

Earlier in the second quarter, the U.S. raised import duties on Chinese cold-rolled flat steel by a staggering 522%. Despite this, there is no reason for contractors to panic.

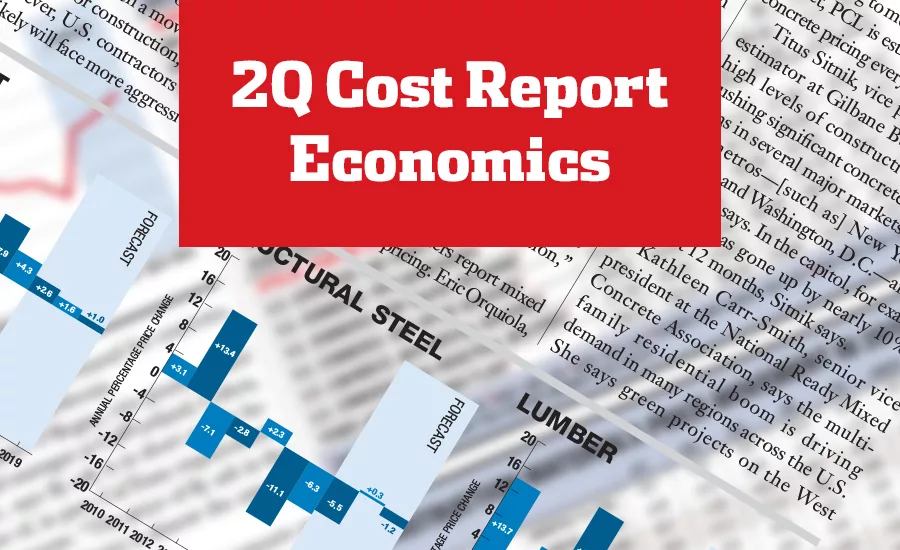

However, looking at the big picture, imported Chinese steel products in 2015 accounted for only 6.15% of all steel products imported into the U.S., according to the U.S. Census Bureau; in March 2016, it accounted for only 2.7% of the total. Drilling down a little further, of the 70,040 tons of steel imported from China in March 2016, only 807 tons was for structural steel and only 29 tons was for reinforcing bar.

|

Click Here to Read the Cost Report (subscription required) |

“While it is possible that the tariff may have an effect on steel plate, pipe and tubing, RLB does not expect the tariff on Chinese steel to lead to an increase in the price of steel members or rebar used in building construction,” says Anderson.

Contractors and suppliers report mixed outlooks on concrete pricing. Eric Orquiola, director of preconstruction at PCL Construction, says concrete pricing typically has followed escalations of 3% to 4% nationally, with some regional exceptions. However, PCL sees higher escalations toward the end of the year, he says. “We’re hearing of shortages of fly ash, but the biggest one may be a shortage of rock,” he says. “That’s a big issue we’re trying to monitor.” On one three-year project, PCL is estimating a $3 increase in concrete pricing every six months.

Looking for quick answers on construction and engineering topics?

Try Ask ENR, our new smart AI search tool.

Ask ENR →

Titus Sitnik, vice president and chief estimator at Gilbane Building Co., says high levels of construction activity are pushing significant concrete price escalations in several major markets. “The major metros—[such as] New York City, Boston and Washington, D.C.—are going nuts,” he says. In the capitol, for example, concrete has gone up by nearly 10% in the past 12 months, Sitnik says.

Kathleen Carr-Smith, senior vice president at the National Ready Mixed Concrete Association, says the multi-family residential boom is driving demand in many regions across the U.S. She says green projects on the West Coast are raising demand for concrete, especially in California.

Melanie O’Regan, vice president and general manager at CalPortland, Colton, Calif., says fly ash is in short supply because of, in part, CalTrans requirements for concrete. “The price of fly ash in the batch-plant [mix] is almost the same as cement now,” she says.

Aggregate costs are also a concern on the West Coast. “Some aggregate suppliers don’t have extra to sell to people that they aren’t already supplying to,” she said. “You can get it, but you’ll pay top dollar because suppliers can command it.”

However, O’Regan said the top driver of cost increases has been a shortage of commercial drivers. “Cement is available—drivers are not,” she added.

This quarter, ENR is introducing two new building cost indexes, compiled by the U.S. Commerce Dept., to its table of 16 major industry indexes. The two new indexes show annual cost increases of 1.7% for medical buildings and 1.9% for industrial buildings. These percentages are slightly lower than the 2.1% average increase for nine other general building cost indexes.

In addition, Commerce’s cost index for residential building work is up 3.0% for the year. Selling price indexes by Sierra West, Turner Construction and RLB show larger increases—between 4% to 8%—due to higher subcontractor and vendor prices. The big negative is a 5.6% drop in construction costs for power plants, tracked by Power Advocate.