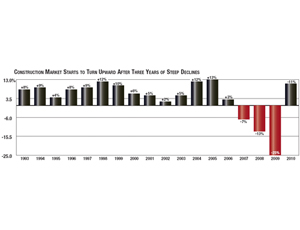

The decline in construction activity this year was broader, steeper and faster than many economists anticipated as private non-residential building markets succumbed to the credit crunch and many public markets waited for stimulus funding to be delivered. The consensus of this year’s batch of forecasts for construction in 2010 says the worst is over, but most gains will be the result of percentage comparisons with dismal 2009 numbers, while market fundamentals will be unable to sustain much forward momentum. Wall Street analyst sometimes call this activity a “dead-cat bounce.”

McGraw-Hill Construction is forecasting the dollar value of total U.S. construction starts in 2010 will climb 11% to $466.2 billion, following an estimated 25% decline in 2009. “This is not a booming market; it is just inching upward,” says Robert Murray, chief economist for McGraw-Hill Construction (MHC), of which ENR is part. “At the very least, we are stabilizing after years of steep declines,” he says.

Single- and multifamily housing will help buoy total construction spending. Single-family housing is expected to hit bottom in 2009 with an estimated 430,000 units started. Murray predicts housing will bounce back from this low with a 30% increase next year to 560,000 starts, which would return the market to 2008’s level. But even with that seemingly robust rebound, housing will remain 65% below its mid-decade peak. In addition, the MHC forecast for housing hinges on continued low mortgage rates and an extension of first-time home-buyer tax credits, Murray adds.

The MHC forecast also expects public works, including institutional building, to give next year’s overall market a boost. “We have seen an uptick in stimulus-related public-works projects last summer, but it has yet to take place in terms of construction starts for buildings,” Murray says. “The hope is that the stimulus bill will provide a lift to institutional buildings and speed up the timing of what would have been a more delayed upturn,” says Murray. He predicts this market will increase 3% next year to $43.6 billion.

Health-care projects took a big hit in 2009 due to the tight credit market. The sector dropped 31% in 2009 to $21 billion. Murray expects the health-care market to bounce back 5% next year to nearly $22 billion. “Aside from money supplied to bolster Medicaid funds, the federal stimulus act carries direct support for health-care construction,” he adds.

The educational building market has been vulnerable to state and municipal budget woes, and Murray expects that market to decline another 3% next year, following an 18% drop in 2009. In terms of square footage, the school market in 2009 dropped 23% to 172 million sq ft as state and local governments pulled back projects and private institutions saw big drops in endowments. The sector is expected to continue its downward path in 2010 with 158 million sq ft of new starts.

Private non-residential building markets have yet to bottom out, according to MHC forecasts. “The commercial market is facing the dual problem of very tight credit and deteriorating market fundamentals,” says Murray. Rents, occupancy and employment trends will continue to depress these markets. Murray predicts both office building and commercial work will fall another 3% next year after tumbling more than 30% in 2009. Hotel and motel work will be hit even harder, with 2010’s expected 9% decline following this year’s 61% decrease.

| Actual | Estimate | Forecast | Percent | Change | |

|---|---|---|---|---|---|

| TYPE OF CONSTRUCTION | 2008 | 2009 | 2010 | 08-09 | 09-10 |

| TOTAL CONSTRUCTION | 554,882 | 418,925 | 466,175 | -24.5 | +11.0 |

| RESIDENTIAL | 162,052 | 113,525 | 147,275 | -30.0 | +30.0 |

| Single-Family Housing | 122,402 | 95,300 | 126,225 | -22.1 | +32.0 |

| Multifamily Housing | 39,650 | 18,225 | 21,050 | -54.0 | +16.0 |

| NON-RESIDENTIAL | 242,614 | 169,200 | 166,600 | -30.3 | -2.0 |

| Office Buildings | 30,621 | 20,350 | 19,675 | -33.5 | -3.0 |

| Hotels and Motels | 12,775 | 4,950 | 4,500 | -61.3 | -9.0 |

| Stores and Shopping Centers | 21,787 | 13,325 | 12,625 | -38.8 | -5.0 |

| Other Commercial | 19,300 | 9,550 | 9,300 | -50.5 | -3.0 |

| Manufacturing | 28,854 | 10,850 | 9,375 | -62.4 | -14.0 |

| Educational Buildings | 57,860 | 47,200 | 45,800 | -18.4 | -3.0 |

| Health-Care Facilities | 30,086 | 20,775 | 21,750 | -31.0 | +5.0 |

| Other Institutional Buildings | 41,331 | 42,200 | 43,575 | +2.1 | +3.0 |

| NON-BUILDING CONSTRUCTION | 150,216 | 136,200 | 152,300 | -9.3 | +12.0 |

| Highways and Bridges | 52,915 | 57,300 | 64,700 | +8.3 | +13.0 |

| Environmental Public Works | 38,230 | 34,000 | 40,200 | -11.1 | +18.0 |

| Other Public Works | 28,836 | 28,400 | 31,400 | -1.5 | +11.0 |

| Electric Utilities | 30,235 | 16.500 | 16,000 | -45.4 | -3.0 |

| Source: McGraw-Hill Construction. Figures for 2010 are estimated. | |||||

| Actual | Estimate | Forecast | Percent | Change | |

|---|---|---|---|---|---|

| TYPE OF CONSTRUCTION | 2008 | 2009 | 2010 | 08-09 | 09-10 |

| TOTAL CONSTRUCTION | 1,072.1 | 962.0 | 944.6 | -10.0 | -2.0 |

| Residential | 357.4 | 268.3 | 287.1 | -25.0 | +7.0 |

| Lodging | 35.8 | 25.8 | 19.1 | -28.0 | -26.0 |

| Office | 70.3 | 56.2 | 43.9 | -20.0 | -22.0 |

| Commercial | 84.9 | 57.7 | 43.3 | -32.0 | -25.0 |

| Health Care | 47.7 | 49.1 | 50.6 | +3.0 | +3.0 |

| Educational | 104.1 | 106.2 | 106.2 | +2.0 | 0.0 |

| Religious | 7.1 | 6.5 | 6.2 | -8.0 | -5.0 |

| Public Safety | 12.9 | 15.0 | 14.7 | +16.0 | -2.0 |

| Amusement and Recreation | 21.5 | 18.7 | 17.2 | -13.0 | -8.0 |

| Transportation | 34.0 | 35.0 | 32.6 | +3.0 | -7.0 |

| Communication | 25.6 | 18.9 | 18.0 | -26.0 | -5.0 |

| Power | 80.2 | 90.6 | 95.2 | +13.0 | +5.0 |

| Highway and Street | 81.8 | 84.3 | 84.3 | +3.0 | 0.0 |

| Sewerage and Waste Disposal | 25.1 | 24.8 | 25.3 | -1.0 | +2.0 |

| Water Supply | 17.0 | 16.2 | 16.5 | -5.0 | +2.0 |

| Conservation and Development | 5.4 | 5.8 | 6.0 | +7.0 | +4.0 |

| Manufacturing | 61.3 | 82.8 | 78.6 | +35.0 | -5.0 |

| Source: U.S. Dept. of Commerce. Figures for 2009 are estimated. | |||||

Manufacturing is expected to have an even tougher time, dropping 14% to $9.4 billion in 2010, after plunging 62% this year as refinery and ethanol plant work dried up. Those two sectors drove the market in 2008. Economists say there is not much hope of the manufacturing market picking up while capacity utilization in the sector remains below 70%.

Pessimist’s Club

The MHC forecast is based on project starts, which tend to be a leading indicator of where construction markets are going. Other industry forecasts focus on construction put-in-place, and these forecasts are calling for further overall declines in 2010, as this year’s 25% collapse in project starts spills over into next year’s put-in-place numbers.

The U.S. Dept. of Commerce in its forecast, released on Nov. 6, is predicting overall construction will decline...

Post a comment to this article

Report Abusive Comment