After several years of unprecedented demand and annual double-digit increases, costs for basic construction materials in the Middle East hit a major market barrier this fall. Whether the correction is short-lived or continues through 2009 or even 2010 is an open question, according to analysts.

(Click to Enlarge Image)

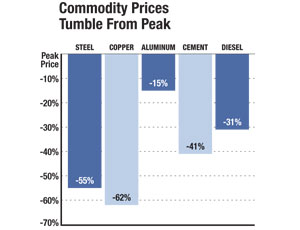

Sources: Rider Levett Bucknall. Percent Change Is From Peak 2008 Price To November 2008. Prices Are For The U.A.E.

Developments underpinning price declines have come fast and hard in recent weeks. Several major developers have announced delays in their megaprojects, including Dubai developer Nakheel slowing its ongoing Palm Island development and Trump International Tower and Hotel. Meraas Development, a company controlled by the Dubai government, says it will delay its $95-billion Jumeirah Gardens City project in Dubai. Dozens of other lesser projects have been put on hold, as the global financial crisis sinks in and developer liquidity problems curtail future speculative projects.

As a result, most materials costs have dropped significantly from record highs in mid July, in some instances dramatically. In the United Arab Emirates, rebar dropped from $1,540 per ton in July to $450 per ton in November. Cement, steel, diesel fuel, aluminum and copper also have fallen from record highs last summer.

Despite these short-term corrections, some analysts expect building costs in the Gulf States to continue an upward march in 2009, although at slower rates than in recent years. Others expect costs to continue to decline in the first half of 2009 and stabilize by year’s end.

U.K.-based construction consultant Rider Level Bucknall projects a 7% increase in building costs in 2009. That follows 20% and 15% cost hikes in 2007 and 2008, respectively, the firm notes.

Despite the impact of the global financial crisis on future projects, the backlog of ongoing work in the Gulf is so large that prices will rebound quickly from the recent downturn. Industry estimates peg the volume of ongoing construction in the U.A.E at $330 billion. “We do not expect major reductions in materials prices” in 2009, Rider Level Bucknall says in its November report.

Another view is that materials costs will continue to fall next year but will stabilize by 2010. E.C. Harris LLP, a U.K construction consultancy, projects a 10% drop in 2009. “With liquidity emerging as a key threat in the region, current levels of growth will be restricted in the short-to-medium term, but we anticipate the supply and demand of the market to be in balance at the start of 2010,” says Mark Prior, E.C. Harris partner.

One area that is likely to remain strong, despite the downturn, is materials for interior fit-outs on current projects.

An estimated $51 billon of interiors work is projected in 2009 in U.A.E., according to a Dubai-based trade publication, DMG-World Media.

Expanding regional steel-production capacity is another trend that will extend beyond the current downturn. A November study by Kuwait-based Global Investment House estimates that countries that are members of the Gulf Cooperation Council (GCC) will invest up to $9 billion over the next three to five years to more than double steel-production capacity. Saudi Arabia, Kuwait, Bahrain, Qatar, U.A.E and Oman comprise the group’s membership. Currently, more than 50% of steel products are imported from outside GCC borders.

“The new capacities that are coming on line are unlikely to pull down prices significantly as additional output will be absorbed by strong steel demand,” the study contends. “Despite the financial turmoil affecting world economic growth, we believe that the demand for steel will remain strong in the GCC,” it notes, adding that, in the shorter term, “steel prices are likely to come down on the back of falling crude-oil and raw material prices and lower world economic growth.”

To that point, the Global Investment House study estimates that GCC countries will invest more than $850 billion over the next three to five years to develop infrastructure, petrochemical industries, tourism and other projects.

Post a comment to this article

Report Abusive Comment